AMT Strategies

Strategy #1 - Defer Regular Tax-Deductible Tax Payments

No itemized tax deduction including state income, sales tax, property tax, etc., is ever deductible for AMT purposes. Conventional wisdom would dictate deferring, where possible, tax payments to the subsequent year if taxed by the alternative method. When deferring, care should be exercised in regard to late payment penalties and interest on underpayments for certain taxes. For example, if a taxpayer puts off paying their state tax liability until the subsequent year, will the benefit exceed the underpayment penalty?

Strategy #2 - Prepay Regular Tax-Deductible Tax Payments

Another way to avoid losing the benefit of a tax deduction to the AMT would be to prepay already assessed taxes being paid in instalments or estimated tax payments in the prior year if not subject to the AMT. Sometimes planning in advance for a specific event will bring attention to the possibility of the AMT in the subsequent year. If that is the case, then paying as many taxes as legally possible (up to the TCJA limit of $10,000) in advance of the AMT-taxed year without throwing that year into the AMT should be considered.

Caution - In Rev Ruling 82-208, the IRS ruled that when a taxpayer makes an estimated state tax payment with no reasonable basis for belief that he owes any additional state income taxes, a deduction will be denied for the year of the payment.

Strategy #3 - Capitalize Property Taxes for Unimproved & Unproductive Real Estate

A taxpayer can annually elect to capitalize property taxes with respect to unimproved and unproductive real estate. (Reg § 1.266-1(b)(1))

Strategy #4 - Don’t Deduct Investment Property Taxes

Investment interest is deductible for AMT purposes. Investment interest expense is limited to net investment income. Net investment income is equal to investment income less investment expenses. Thus, deducting investment expenses for regular tax purposes will only limit the available investment interest expense deduction. The result may be a negative benefit from deducting taxes and investment expenses. Note: For years 2018 through 2025, the TCJA suspends the miscellaneous deductions that are subject to the 2% of AGI reduction (Tier 2 expenses), so in these years Tier 2 investment expenses won’t be deductible anyway. Property taxes aren’t part of Tier 2 expenses but are included in the taxes for which a deduction is capped at $10,000 per year by the TCJA.

However, the taxpayer may only be marginally in the AMT and it may be appropriate to only limit part of the deductions. The best way to determine the optimal amount is by trying various scenarios using your tax software. Some of the more sophisticated programs may do this analysis automatically. When limiting deductions, you should also consider what the effect will be on the taxpayer’s state return. Does state law allow deductions only if they have been claimed on the federal return? You may need to look at the combined federal and state tax liabilities before deciding not to deduct investment taxes and other expenses as a strategy to minimize federal AMT.

Another element to consider is the 3.8% net investment income tax (NIIT) on higher-income individuals. To be able to offset gross investment income by investment expenses for purposes of this tax, the expense must be claimed when figuring regular tax. So, when trying various scenarios to determine whether to limit the investment expense as a way to reduce AMT, be sure to also take the 3.8% NII tax into account. But the investment expenses not allowed as a miscellaneous deduction due to the TCJA suspension won’t be deductible for the 3.8% NIIT calculation either.

Strategy #5 - Tax Benefit Rule – State Income Tax

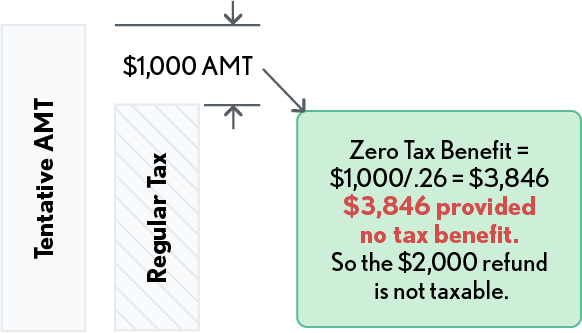

When taxed by the AMT, part or none of the state income tax paid is allowed as a deduction. Therefore, to the extent the tentative AMT income exceeds the regular taxable income, the taxpayer receives no benefit for the state tax deduction. To the extent the taxpayer receives no benefit, the state income tax refund is not taxable for regular tax purposes in the subsequent year. Some tax software makes this computation, some don’t.

For sure they do not for a new client that had AMT in the prior year. A state’s refund statement (Form 1099-G) absolutely does not take the AMT into consideration. Therefore, if there is a state refund from the prior year and the taxpayer had some amount of alternative minimum tax in the prior year, then part or all the refund may not be taxable. (IRC §111(a)) The no tax benefit amount can generally be determined from the AMT amount; see example:

Example – Extrapolating the No Benefit Amount - In the prior tax year, the taxpayer itemized, and his state income tax deduction was $5,000, his state tax refund was $2,000 and the AMT (add-on tax) was $1,000. Assuming he was in the 26% AMT bracket and his AMT tax was $1,000, he did not receive benefit from $3,846 ($1,000/.26) of the state income tax deduction. Therefore, any state tax refund up to that amount would not be taxable in the subsequent year. In this example, none of the $2,000 refund needs to be included in income the following year.

-

Be Sure to Look Back – To see if the taxpayer was subject to the AMT on the prior year’s return. If they were, apply the tax benefit rule and treat as taxable the amount of refund that reduced the regular tax taxable income below the alternative minimum taxable income (AMTI).

Strategy #6 - Schedule A Taxes Can Reduce AMT LTCG Tax

The LTCG rates for AMT purposes are determined from the taxpayer’s regular taxable income for the year. Therefore, to the extent a taxpayer’s regular taxable income for 2025 is no more than $48,350 single, $64,750 head of household, $96,700 married joint, or $48,350 married separate, their LTCG will be taxed at 0% for both AMT and regular tax purposes. This makes the planning choices more difficult. The question being: is there more tax benefit maximizing the tax deduction or minimizing it through other strategies for taxes?

Home Mortgage Interest

Below is a review of the home mortgage interest limitations:

-

Acquisition Debt - Code Sec. 163(h)(3)(B)) Is debt incurred to purchase, construct, or substantially improve a taxpayer’s principal home or second home and must be secured by the home. Acquisition debt interest is deductible for AMT purposes. Combined acquisition debt on the two homes can’t be more than:

-

$1,000,000 ($500,000 for married separate) for acquisition debts incurred on or before December 15, 2017.

-

$750,000 for acquisition debts incurred after 12/15/2017

-

Refinanced debt can also qualify as acquisition debt, if it doesn’t exceed the amount of the acquisition debt just before the refinancing.

-

-

Home Equity Debt - (Code Sec. 163(h)(3)(C)) Is debt that is not acquisition debt and is secured by a taxpayer’s principal or second home., For years other than 2018-2025, for regular tax purposes, the equity debt on the two homes can’t be more than $100,000 ($50,000 for married separate), or the difference between the acquisition debt on the home and the FMV of the home, if smaller., Equity debt interest is NOT deductible for AMT purposes. Note: For years 2018 through 2025 TCJA suspended the deduction of equity debt interest for regular tax purposes, so for those years there is no AMT adjustment for equity interest.

-

Nonconventional Home Debt – IRC Sec 56(e)(2) Says that a “qualified dwelling unit” for purposes of the “qualified housing interest” deductible for AMT purposes is a house, apartment, condominium, or mobile home not used on a transient basis. Thus, for AMT purposes nonconventional home interest is not allowed as qualified home mortgage interest. The term nonconventional home refers to homes that are used on a transient basis, such as a motor home and boat. Starting with 2018 returns, nonconventional home debt interest does not appear as one of the Form 6251, line 2 items. However, the 6251 instructions for line 3, other adjustments, directs that an adjustment for nonconventional home interest be included on that line.

Charitable Contributions

The same charitable contributions that are allowed for regular tax purposes are allowed for AMT (with a rare exception – see 6251 instructions page 8)., Thus, generally there is no adjustment for charitable contributions on Form 6251.

Miscellaneous Deductions

Miscellaneous deductions are segregated into two categories, Tier 1 or Tier 2 expenses., Prior to 2018, Tier 1 miscellaneous deductions were allowed for AMT purposes but not Tier 2. With the advent of TCJA, Tier 2 deductions are suspended for years 2018 through 2025. Thus, there is no longer an AMT adjustment for miscellaneous deductions.

Phase-Out of Itemized Deductions

Subtract the regular tax overall itemized deduction phase out amount for high-income taxpayers, if any, since it does not apply to AMT tax., Thus, itemized deductions allowed in computing alternative minimum taxable income aren’t reduced for high-income taxpayers in computing the AMT. However, for 2018 through 2025, this is not an issue since TCJA suspended the PEASE phase-out.

Tax Refund

(Form 6251 – Line 2b) – For AMT purposes, the taxable refunds of state and local taxes are not included in the AMT computation., A state income tax refund should be an automatic adjustment by your software for prior year clients, but make sure the refund is not taxed for AMT for new clients. Include any refund from Form 1040 Schedule 1, line 1 or 8z (2021), that is attributable to state or local income taxes. Although rare, this exclusion also applies to refunds of local taxes, real property taxes, personal property tax, foreign income tax and foreign real property tax that are treated as income because they were included as an itemized deduction on a prior year return, and the income cannot be excluded for regular tax purposes on the current return under the tax benefit rules.

Investment Interest Expense

(Form 6251 – Line 2c) – Investment interest is deductible for both regular and AMT purposes to the extent of net investment income (Note: investment expenses are part of the Tier 2 miscellaneous itemized deductions and therefore not used in the computation of net investment income for years 2018 through 2025). However, investment taxes if allowed as part of the $10,000 cap on taxes would be since that is an investment expense. Because the interest from most private activity municipal bonds is taxable for AMT purposes, taxpayers with private activity bond income will have a higher net investment income and, therefore for AMT purposes, will be allowed to deduct more investment interest expense., This also creates two investment interest carryovers, one for regular tax and one for the AMT. Generally, most preparation software will make both carryover computations. Line 2c on the 6251 compensates for the differences between the regular investment interest deduction and the AMT investment interest deduction.

-

Strategy - Utilize the Capital Gains Election - Income that is subject to the long-term capital gains rates is not investment income for purposes of computing the net investment interest limitation. However, the election to tax LTCG at ordinary rates and include that LTCG income as investment income applies to both the regular tax and the AMT. This will allow a larger deduction for investment interest for both the regular tax and the AMT. This adjustment is generally automatic in most tax preparation software. Therefore, if there is a planning reason not to utilize this election, the software will need to be overridden.

Depletion Adjustments

(Form 6251 – Line 2d) – The depletion deduction has limits based upon income from an activity and asset basis limitations., This adjustment is the excess of percentage depletion over cost basis. Except with respect to depletion taken by independent oil and gas producers and royalty owners, the excess of the allowable depletion on each depletable asset over the adjusted basis (before considering the current year's depletion) of the property at the end of the year is a preference item., This adjustment is rarely encountered for individual purposes except via pass-through entities.

Net Operating Loss Adjustments

(Form 6251 – Lines 2e and 2f) – The NOL deduction for regular tax purposes is replaced in the AMT tax computation with the NOL computed based upon AMT income and deductions.

Watch out! Frequently when carrying back an NOL to a prior year the AMT NOL is overlooked and not also carried back. When the carry back year is subject to the AMT, failure to include the AMT NOL will reduce or eliminate the benefit of the NOL carry back. It will also generate correspondence from the IRS if filed without the AMT NOL.

Note: The CARES Act, enacted March 27, 2020, modified the NOL changes that were put in place by the TCJA. Thus, for any net operating loss arising in a taxable year beginning after December 31, 2017, and before January 1, 2021 (i.e., 2018, 2019 and 2020 returns), the loss is carried back to each of the 5 taxable years preceding the loss year starting with the earliest year in the carry back period. The loss deducted in the carry back year is not subject to the 80% of taxable income limitation that was added by the TCJA. These carry back provisions are retroactive to 2018, so a taxpayer that incurred an NOL in 2018 would carry the loss back to 2013 to recover tax paid in that year, and then carry any excess loss forward to 2014. If there’s still loss remaining, then carry the remaining loss forward to 2015, and so on. See chapter 3.16 for details.

Private Activity Bond Interest

(Form 6251 – Line 2g) – Tax-exempt interest and tax-exempt interest dividends on certain private activity bonds issued after 8/07/86 is a tax preference item (after 9/01/86, for bonds considered governmental bonds by pre-TRA ’86 definition)., Private activity bonds include those that finance mass-transit facilities, sewage and solid waste disposal facilities and certain multi-family dwellings. Taxpayers may invest in these bonds individually or through holdings in mutual funds that invest in government obligations (“muni bonds”). Tax-exempt interest and the portion of it that is private activity interest is required to be reported by the payer on Form 1099-INT, boxes 8 and 9, respectively. On Form 1099-DIV, the exempt-interest dividends amount is shown in box 12 and private activity bond interest dividends appear in box 13. The tax preference amount is the private activity interest and dividend income reduced by the related expenses not allowed for regular tax purposes because the income is nontaxable.

NOTE: The interest on the following bonds that are otherwise considered private activity bonds is not a tax preference: (1) certain mortgage bonds, qualified Veterans’ mortgage bonds, and bonds related to residential rental projects issued after July 30, 2008, and (2) bonds issued in 2009 and 2010.

-

Strategy - Eliminate Investments in Private Activity Bonds - Taxpayers invest in lower yielding muni bonds because they provide tax-free income. However, when a taxpayer is subject to the AMT the tax-free benefit for private activity muni bonds is lost. Therefore, taxpayers who are regularly subject to the AMT should avoid investing in Private Activity Bonds or mutual funds that invest in such bonds (but see “Note” just above). Taxpayers who already have these bonds in their portfolio should consider divesting themselves of these investment vehicles if it makes financial sense.

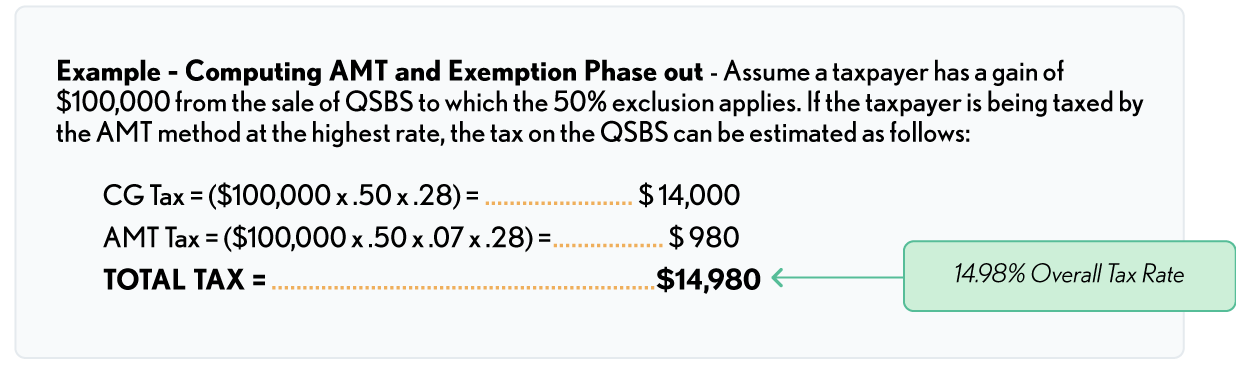

Excluded Qualified Small Business Stock Gain

(Form 6251 – Line 2h) – Current tax law dictates that non-corporate taxpayers exclude 50%, 75% or 100% of any gain realized on the sale or exchange of “qualified small business stock” held more than 5 years. The exclusion percentage depends on when the stock was issued:

-

50% gain exclusion for stocks issued after 8/10/1993 and before 2/18/2009.

-

75% gain exclusion for stocks issued after 2/17/2009 and through 9/27/2010.

-

100% gain exclusion for stocks issued after September 27, 2010.

Gain from the sale of Sec 1202 stock does not benefit from the special 0%, 15% and 20% capital gains rates. But the gain that isn’t excluded will be taxed at a maximum of 28% for regular tax. For AMT, 7% of the excluded Sec 1202 gain is treated as a tax preference, unless the 100% exclusion applies, in which case, none of the gain is considered a tax preference item.

When the entire preference is subject to the highest AMT rate (28%), the effective rate on the Sec.

Incentive Stock Option Preference Income

(Form 6251 – Line 2i) – If an option is a qualified option (also known as an incentive stock option), then for regular tax purposes, no amount of income is included in income either at the time the option is granted or at the time it is exercised., Income or loss is recognized when the stock is sold., However, to qualify for this treatment, the stock acquired under the option must be held for:

-

More than 1 year after the stock option was exercised, AND

-

More than 2 years after the option was granted.

The gain or loss from the sale of ISO stock is generally a capital gain or loss. The gain for regular tax purposes will be the difference between the exercise price and the sales price. If the stock is sold prior to the required holding period, the income to the extent of the bargain element will be treated as ordinary income (wages).

For AMT purposes, taxpayers recognize alternative minimum taxable income (AMT preference income) equal to the excess of the fair market value of the stock on the exercise date over the exercise price. This creates three effects for AMT purposes:

-

Preference income in the exercise year, and

-

A different stock basis for AMT gain or loss (AMT basis = Exercise price and REG tax basis equals grant price), and

-

Since the ISO preference is a deferral item of preference, an Alternative Minimum Tax Credit carryover may also be generated (see AMT credit later).

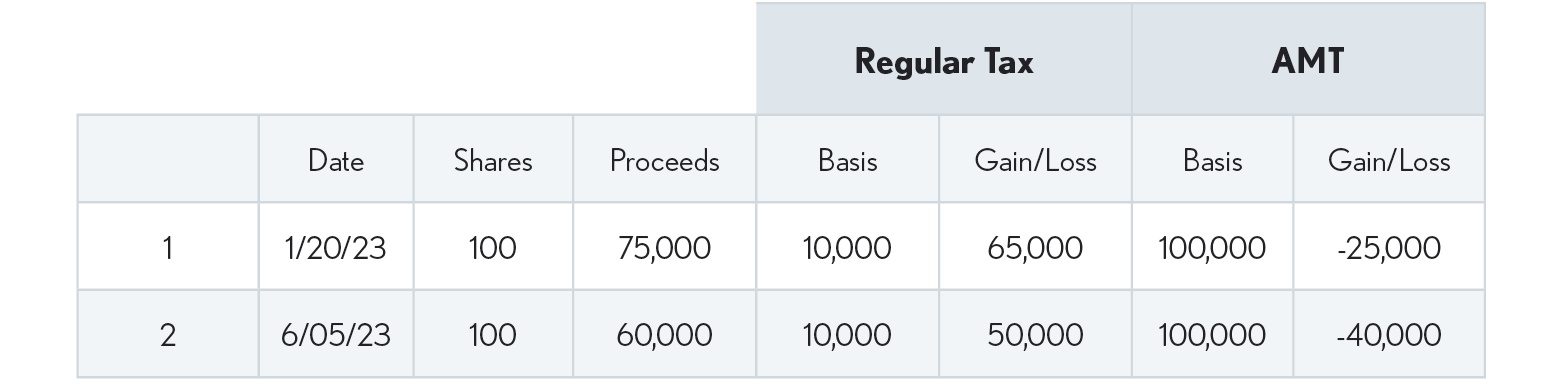

Example – Exercising an ISO – In January 2016, Victor is granted an option to purchase up to 20,000 shares of XYZ, Inc. On March 30, 2022, Victor exercises the option and pays $20,000 to acquire 20,000 shares of stock with a FMV of $200,000. The results for 2022 are:

-

Regular tax: No taxable income, Stock Basis of $20,000

AMT: $180,000 Preference Income ($200,000 - $20,000) and a stock basis of $200,000.

Transaction#1 – Disqualified disposition, since he sold the stock before meeting the one-year ISO holding requirement. It results in the following tax treatment:

-

Regular Tax: Ordinary Income of $65,000 (NOT a Form 8949/Schedule D transaction) AMT: Short-Term Capital Loss of $25,000

Transaction #2 – Since he met the ISO holding period requirements, this transaction results in a qualified disposition with the following tax treatment:

Regular Tax: Long-term capital gain of $50,000

AMT: Long-term capital loss of $40,000

Since the Schedule D is computed separately for the regular and AMT tax, the result of the two transactions is a $65,000 AMT Schedule D loss. However, the loss is limited to $3,000 (this produces a separate AMT capital loss carryover). For regular tax purposes, we have $65,000 ordinary income and $50,000 long-term capital gain. Therefore, the difference between regular tax income and AMTI for this example is $118,000 ($65,000 + $50,000 - <3,000>).

CAUTION: Victor’s Schedule D will also need to be refigured for AMT purposes.

Strategy #1 - Exercise ISO in Amounts to Avoid AMT - Taxpayers who are under the AMT threshold might consider developing a multi-year plan to exercise the options in smaller amounts to avoid or minimize AMT.

Strategy #2 - Sell Early and Treat as Nonqualified Option - Taxpayers who will be subject to the AMT in the exercise year should consider exercising and selling in the same year, thus creating a disqualifying disposition and thereby eliminating the preference income.

Strategy #3 - Utilize the AMT Tax Credit - Where a taxpayer will not be subject to the AMT in a subsequent year and has an AMT credit carryover, the taxpayer might consider subjecting themselves to the ISO AMT preference and then recover part or all of the AMT add-on tax in a subsequent year when the AMT credit can be utilized. AMT tax credit is discussed later in this material.

Disposition of Property

(Form 6251 – Line 2k) - Difference between Regular and AMT gain or loss. This adjustment is made if property is sold during the year., The gain or loss must be refigured for AMT purposes using the AMT basis for the property., The difference between the gain or loss reported for regular tax and the recomputed AMT gain or loss is the adjustment. This can be a negative amount for property where depreciation, circulation expenses, research and experimental expenses, mining exploration expenses, or pollution control expenses have been different for AMT purposes than for regular tax purposes.

-

Real Property Differences – Prior to 1999 real property had a preference adjustment equal to the difference between the 27.5-, 31.5- or 39-year life and the 40-year straight-line depreciation. After 1998 there is no preference adjustment for real property. Thus, if a property is sold that was in service before 1999 there will be a favorable difference between the AMT and regular tax gain or loss.

-

Personal Property Differences – After 1998, personal property depreciated at the 200% MACRS rates had a preference adjustment in the amount of the difference between the 200% and the 150% MACRS rate. Thus, for personal property not fully depreciated there will be a favorable difference between the AMT and regular tax gain or loss.

These differences will result in a favorable AMT adjustment when the asset is ultimately sold. This is true whether or not the taxpayer was subject to AMT in any of the prior years.

However, the first-year bonus depreciation allowance applies for both regular tax and AMT and for property on which the bonus allowance is claimed, there is no preference adjustment. If the election was made not to claim bonus depreciation on eligible property put in service before 2016, the property may be subject to a preference adjustment. A provision of the PATH Act of 2015 eliminates the preference adjustment for all property placed into service after 2015 and eligible for bonus depreciation, whether or not the special allowance was elected. (2016 Form 6252 instructions, page 6)

Strategy #1- Differences between Regular and AMT Depreciation Rates

Don’t overlook Form 4797 gain or loss differences for the AMT as a result of AMT depreciation, even if the client was not taxed by the AMT in the year the depreciation was taken. The AMT depreciation rate is lower than the regular rate, which could result in a smaller AMT gain and thus reduce the AMTI.

Depreciation of Property after 1986

(Form 6251 – Line 2L) – Adjustment for the difference between regular and AMT depreciation., Generally, the taxpayer must refigure depreciation for the AMT, including depreciation allocable to inventory costs, for property that is depreciated for the regular tax using the 200% declining balance method (generally 3-, 5-, 7-, or 10-year property under the modified accelerated cost recovery system (MACRS))., The preference is the difference between the 200% and the 150% MACRS rate. But see “bonus depreciation” in box just above.

Strategy #1 - Use AMT Depreciation Rates - Taxpayers who are regularly subject to the AMT should consider using the 150% declining balance method of depreciation for regular tax and thus avoid the AMT adjustment between the 200% and 150% declining balance methods.

Strategy #2 - Use the Section 179 Deduction - The Section 179 expense deduction is NOT a preference adjustment for AMT. Therefore, the 179 deductions can be used in place of the MACRS depreciation to avoid an AMT adjustment. If there is a limit on the 179 deduction or the taxpayer’s circumstances dictate a slower write-off, a partial 179 deduction can be combined with the 150% declining balance method to avoid AMT.