Planning for Zero Tax on Long-Term Capital Gains

Lower-income taxpayers and those whose income is abnormally low for the year can enjoy a long-term capital gain tax rate of zero, which provides an interesting strategy for these individuals.

Even if the taxpayer wishes to hold on to a stock because it is performing well, they can sell it and immediately buy it back, allowing them to include the current accumulated gain in the sale-year’s return with no tax while also reducing the amount of taxable gain in the future. If they are concerned about the so-called wash sale rules that require a taxpayer to not buy back the same stock within the 30 days before or after the sale of the stock, that is not a problem because the wash sale rules only apply to stocks sold at a loss.

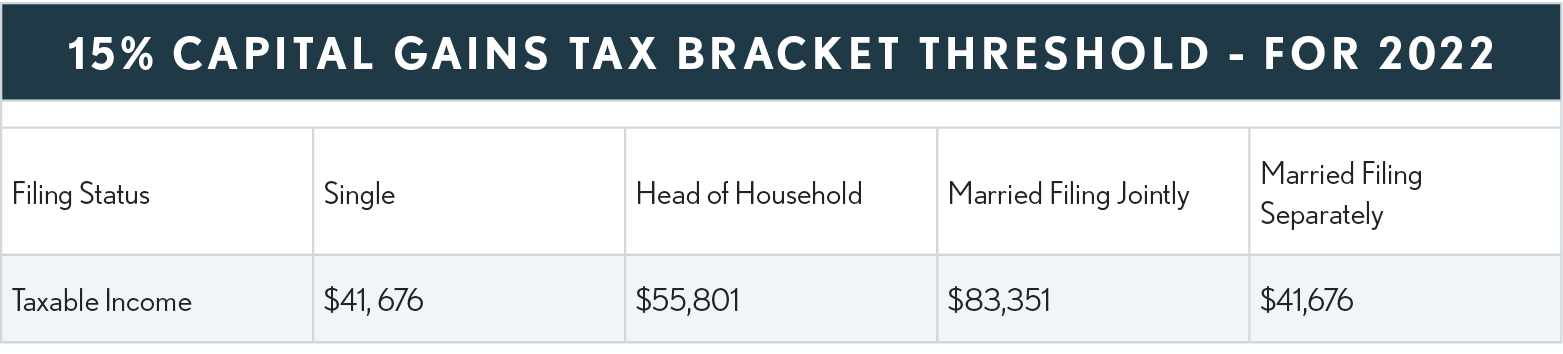

To determine if a taxpayer can take advantage of this tax-saving opportunity, you must determine if their taxable income will be below the point where the 15% capital gains tax rate begins. The following table shows the incomes at which the gain becomes taxable at 15% for different filing statuses in 2022.

Example: Suppose a married couple is filing jointly and has projected taxable income for the year of $50,000. From the table above we find that the 15% capital gains tax bracket threshold for married joint filers is $83,351. That means they could add $33,350 ($83,350- $50,000) of long-term capital gains to their income and pay zero tax on the capital gains.

-

Of course, this strategy must be worked out based upon the taxpayer’s projected taxable income for the year, which could be more or less than the estimated amount.

In addition, if the taxpayer has any loser stocks, he or she can sell them for a loss, and thereby allow additional long-term capital gains to take advantage of the zero-tax rate.

There are also some situations where the increase in adjusted gross income as a result of the added long-term capital gains could have other unanticipated adverse effects on a taxpayer that could reduce the overall benefit of this strategy. They include reducing the taxpayer’s ACA premium tax credit, and for seniors, causing an increase in the Medicare premium withheld from their Social Security benefits.