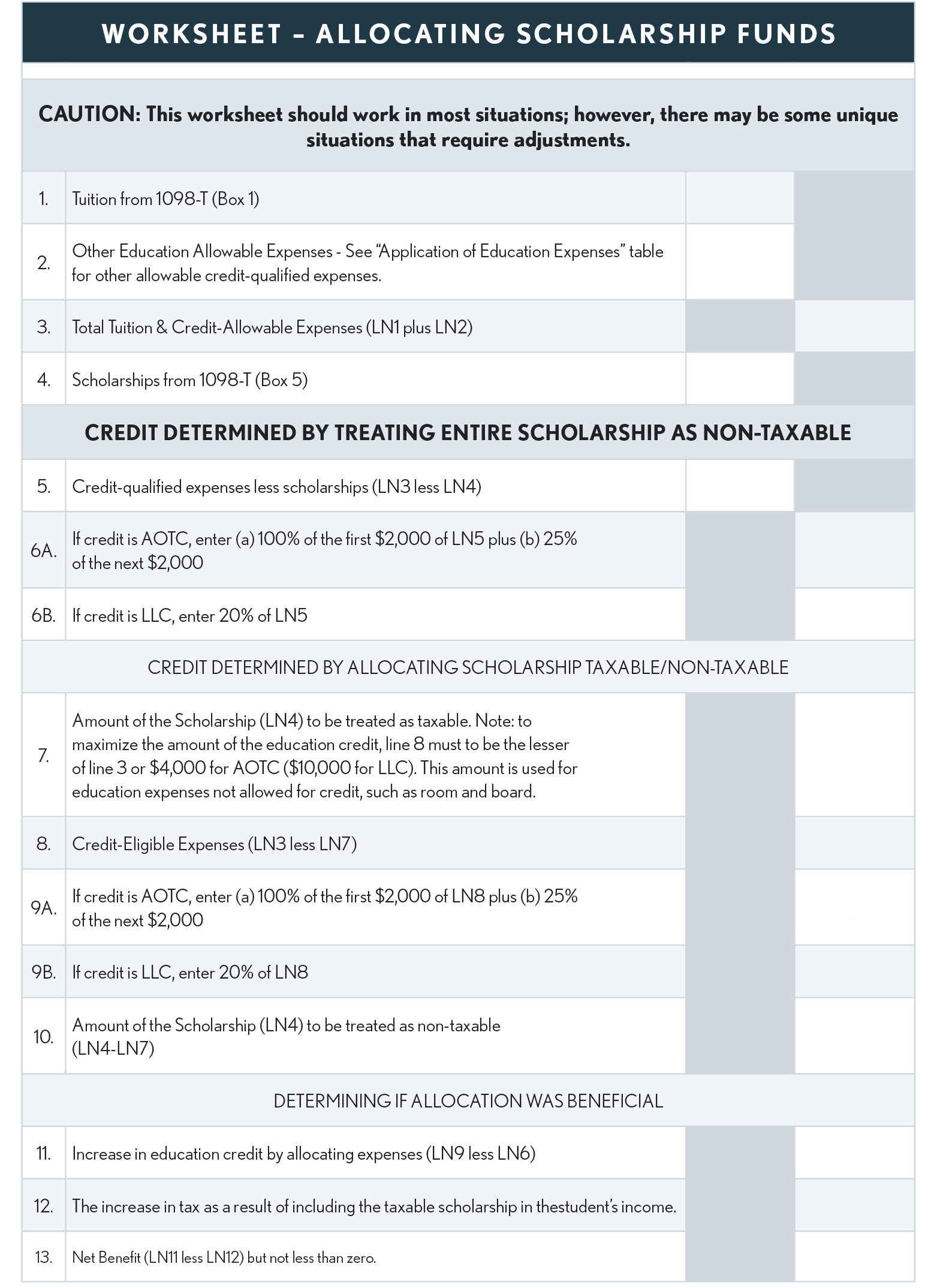

Interaction of Scholarships and Education Tax Credits

For education credit purposes, qualified tuition must be reduced by tax-free scholarship amounts (including fellowships) excluded from income under Code Sec. 117 except to the extent, by the terms of the scholarship, it may (or must) be applied to room and board, in which case it is reported as taxable income if the student is required to file a tax return. (Reg. § 1.25A-5(c)(3))

Scholarship Terms

The use of scholarship funds depends upon the terms of the scholarship.

-

If the scholarship specifies it must be used towards tuition and expenses, then the scholarship is non-taxable and must reduce expenses that qualify for the education credits.

-

If the scholarship specifies it is for room and board, then it must be used for room and board and is therefore taxable income. Where the funds can be used for any education purpose (discretionary), the use of the funds can be allocated among the educational expenses that provides the best overall tax benefits.

Federal Student Aid

Federal student aid, including Pell Grants, can be used to cover a variety of costs, generally including tuition and fees normally assessed; books, supplies, transportation, and miscellaneous personal expenses; and living expenses such as room and board.

GI Bill

Payments to vets under the GI Bill for tuition and allowances is treated as support provided by the government when determining who pays over half of a student’s support. (2021 Pub 17 page 35)

Scholarship Strategy

Being able to allocate scholarships where the terms permit provides a significant strategy for maximizing the education credits. Consider the following:

-

If the terms of a scholarship permit, a student may choose to allocate (in any portions) the use of scholarship funds to either credit-qualified expenses or other education expenses that are not qualified for the credits such as room and board. (Reg § 1.25A-5(c)(3))

-

Any amount allocated to credit-qualified expenses is non-taxable and reduces the expenses that are qualified for an education credit.

-

Any amount allocated to other than credit-qualified expenses (such as room and board) becomes taxable income on the student’s tax return if the student is required to file a tax return.

Observation

If the parent(s) claim the student as a dependent, the parent(s) get the education credit, but the taxable scholarship amount is included in the student’s income, and since it is considered earned income, it is taxed at the student’s tax rate.

Making this allocation can become complicated since one must take into consideration the benefit of the education credit versus any tax to the student as a result of treating some portion of the scholarship amount as taxable.

Example: Student receives a scholarship (Pell Grant) in the amount of $5,000. Her tuition for the year was $5,000. So, her 1098-T will show $5,000 in box 1 (payment received for qualified tuition and related expenses) and $5,000 in box 5 (scholarships or grants). She also had other credit qualifying expenses of $1,500, bringing the total expenses to $6,500. Without allocating her scholarship funds, the scholarship would be nontaxable and reduce her expenses qualifying for the credit to $1,500 and a resulting AOTC of $1,500 (100% of $1,500). The student is in the 12% tax bracket.

-

By using the worksheet and allocating the scholarship between taxable and non-taxable income, the credit can be increased by $1,000 to $2,500 ((100% x $2000) + (25% x $2000)). However, the portion of the scholarship treated as taxable is taxable to the student, and in our example increases the student’s tax by $300, resulting in a net tax benefit of $700.