Special Home Sale Exclusion Rules For Married Taxpayers

When a married couple divorces or one spouse dies, special home sale gain exclusion rules apply. Learn more about how the IRS requires taxpayers to deal with these situations below:

Transfers Between Spouses or Transfers Related To Divorce

For an individual holding property transferred between spouses or transfers incident to divorce, the period the individual owns the property includes the period the transferor owned the property. However, the period that the transferor spouse or former spouse used the property is not included in the period that the individual used the property. So, it seems that the transferee spouse would still have to satisfy the use requirement in order to qualify for the exclusion. (Reg. §1.121-4(b)(1))

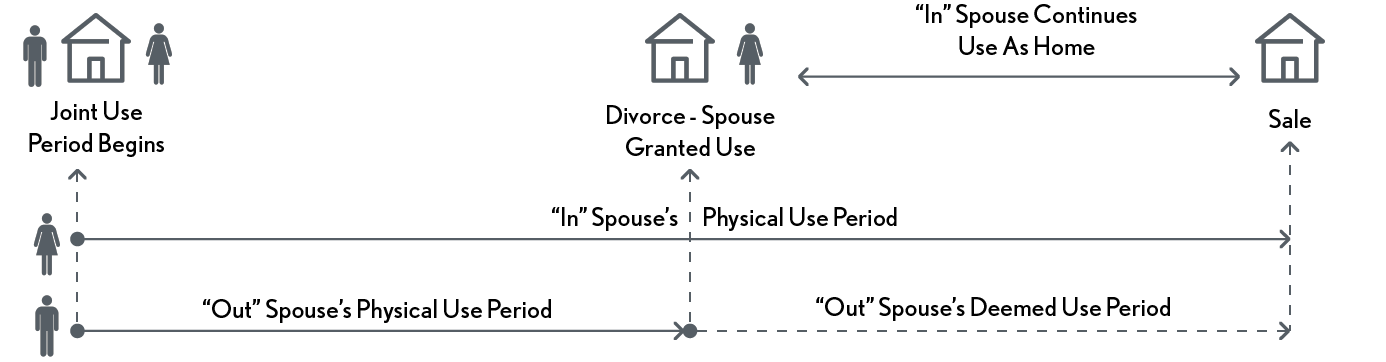

Sale After Ex-Spouse Retains Property For Some Period of Time

Only for purposes of this exclusion is an individual treated as using property as the individual’s principal residence during any period of ownership while the individual’s spouse or former spouse is granted use of the property under a divorce or separation instrument. This means that if a husband (or wife) continues to own the home after a divorce, and his/her former wife (husband) is granted use of the property under a divorce instrument, the exclusion could be available when the husband (wife) sells the house if he (she) meets the ownership requirement and his wife (her husband) meets the use requirements. (Reg. §1.121-4(b)(2))

Deceased Spouse’s Property

A surviving ppouse is treated as owning and using property as the taxpayer's principal residence during any period that the taxpayer's deceased spouse owned and used the property as a principal residence before death if (Reg. §1.121-4(a):

1) The taxpayer's spouse is deceased on the date of the sale or exchange of the property; and

2) The taxpayer has not remarried at the time of the sale or exchange of the property.

Special Note: Remember, a surviving spouse will have a step-up (or step-down) in basis for half or all of the property (depending on how title is held and state law). In addition, the capital gains holding period for inherited property is always long-term. (This note is not applicable for property acquired from a decedent dying in 2010 if the executor chose the “no estate tax” and carryover basis method.)