Principal Residence Defined For the Home Sale Gain Exclusion

The definition of a homeowner's principal residence, as defined by the IRS, helps to determine eligibility for the home sale gain exclusion.

The home sale exclusion only applies to the taxpayer’s principal residence. Final regulations address the definition of principal residence. In the case of a taxpayer using more than one property as a residence, which one qualifies depends upon all the facts and circumstances. If a taxpayer alternates between two properties, using each as a residence for successive periods of time, the property that the taxpayer uses most of the time during the year will ordinarily be considered the taxpayer's principal residence. (Reg. §1.121-1(b))

Relevant Factors – In addition to the taxpayer’s use of the property, relevant factors in determining a taxpayer's principal residence include, but are not limited to (Reg. §1.121-1(b)):

-

The taxpayer's place of employment;

-

The principal place of abode of the taxpayer's family members;

-

The address listed on the taxpayer's Federal and state tax returns, driver's license, automobile registration, and voter registration card;

-

The taxpayer's mailing address for bills and correspondence;

-

The location of the taxpayer's banks; and,

The location of religious organizations and recreational clubs with which the taxpayer is affiliated.

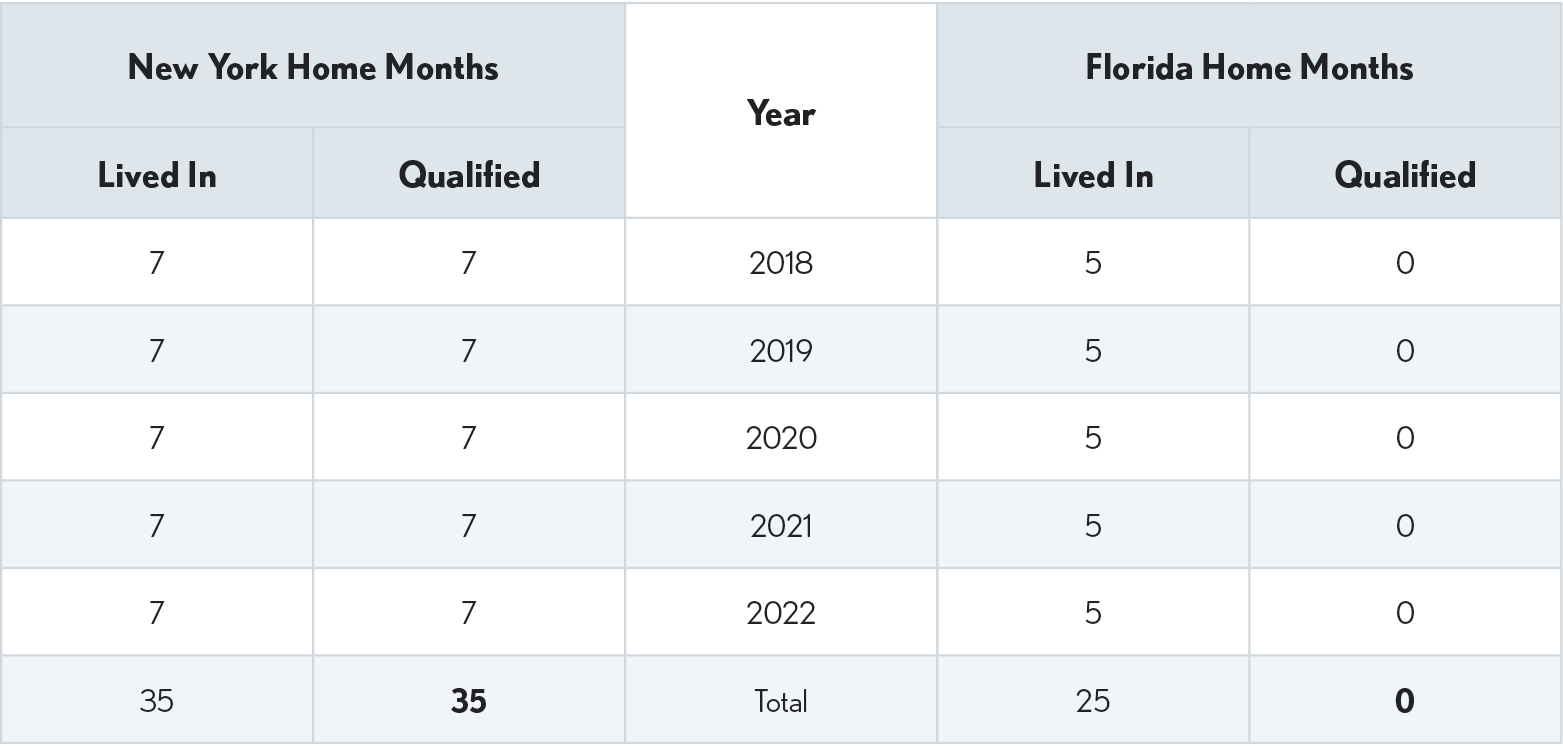

“ Example #1 – Taxpayer owns two residences - Taxpayer K owns two residences, one in New York and one in Florida. From 2018 through 2022, K lives in the New York residence for 7 months and the Florida residence for 5 months in each year. Thus, K used the New York residence a majority of the time in each year from 2018 through 2022. Therefore, in the absence of facts and circumstances indicating otherwise, the New York residence is K's principal residence, and only the New York residence would be eligible for the §121 exclusion if it were sold at the end of 2022. ”

-

Note

Example #1 is interesting in the fact that even though both properties meet the 24-month use and ownership tests, only the New York property qualified as the primary residence during any of the five-year period. Therefore, only the New York home will qualify for the exclusion. In example #2 that follows, both properties qualified as a primary residence during the 60-month qualification period.

“ Example #2 – Taxpayer owns two residences - Taxpayer L owns two residences, one in Virginia and one in New England. During 2018 and 2019, L lives in the Virginia residence. During 2020 and 2021, L lives in the New England residence. During 2022, L lives in the Virginia residence. L's principal residence during 2018, 2019 and 2022 is the Virginia residence. L's principal residence during 2020 and 2021 is the New England residence. Either residence would be eligible for the 121 exclusion if it were sold during 2022. ”

-

“ Example #3 – Taxpayer owns two residences – This uses the same homes as example #2 except the lived-in and qualifying months have been changed to demonstrate that it is possible to have two homes with neither clearly qualifying as principal residence. When a situation like this occurs, you will have to rely on “facts and circumstances” to determine if the home being sold qualifies as the taxpayer’s principal residence. ”

-