Miscellaneous Home Sale Gain Exclusion Rules

There are a number of miscellaneous circumstances that can impact taxpayers' eligibility for the home sale gain exclusion. These include an unmarried couple jointly owning a home, the sale of partial interest in a home, and more.

Learn more about how the IRS requires taxpayers to deal with some of these home sale issues below:

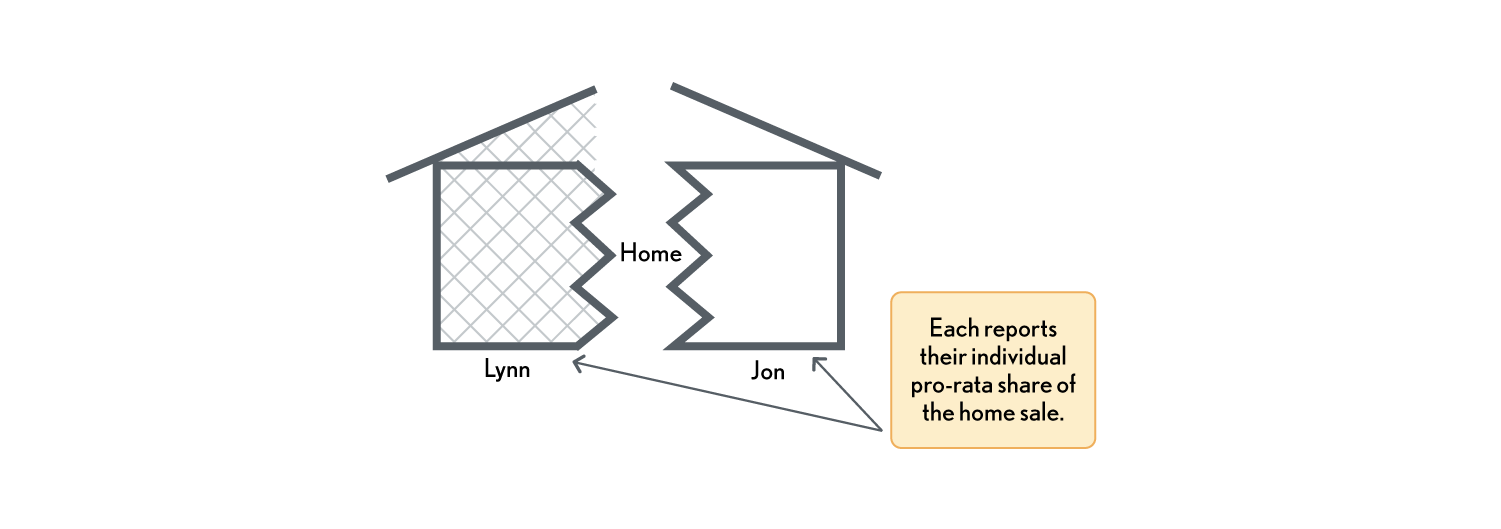

Jointly Owning a Home – Unmarried Individuals

(Reg. §1.121-2(a)(4), Ex. 1) - If two unmarried individuals jointly own and use one principal residence, the $250,000 exclusion provisions apply independently to each upon a sale of the residence. Everyone must report their separate gain (or loss) on their personal tax return and, therefore, may be eligible to exclude from gross income up to $250,000 of gain that is attributable to each taxpayer’s interest in the property.

Example – Unmarried Taxpayers - Lynn and Jon, who are unmarried, own a house as joint owners, each owning a 50-percent interest in the house. They sell the house after owning and using it as their principal residence for 2 full years. The gain realized from the sale is $256,000. Lynn and Jon are each eligible to exclude $128,000 of gain because the amount of realized gain allocable to each of them from the sale does not exceed the available limitation amount of $250,000 available to each separately.

-

Sales of Partial Interests and Remaining Interests

(Reg §1.121-4(e)(1)(ii)) - Only one maximum limitation amount of $250,000 ($500,000 for certain joint returns) applies to the combined sales or exchanges of the partial interests. In applying the maximum limitation amount to sales or exchanges that occur in different taxable years, a taxpayer may exclude gain from the first sale or exchange of a partial interest up to the taxpayer's full maximum limitation amount and may exclude gain from the sale or exchange of any other partial interest in the same principal residence to the extent of any remaining maximum limitation amount, and each spouse is treated as excluding one-half of the gain from a sale or exchange relating to the limitation for certain joint returns apply.

Caution: The provisions for sales of partial interests do not apply to sales or exchanges of remainder interests to related parties described in Sections 267(b) or 707(b). (Reg §1.121-4(e)(1)(ii)(B)). A remainder interest is where beneficiaries (remainderman) of an estate or trust get future ownership of a property after the tenant in a life estate passes.

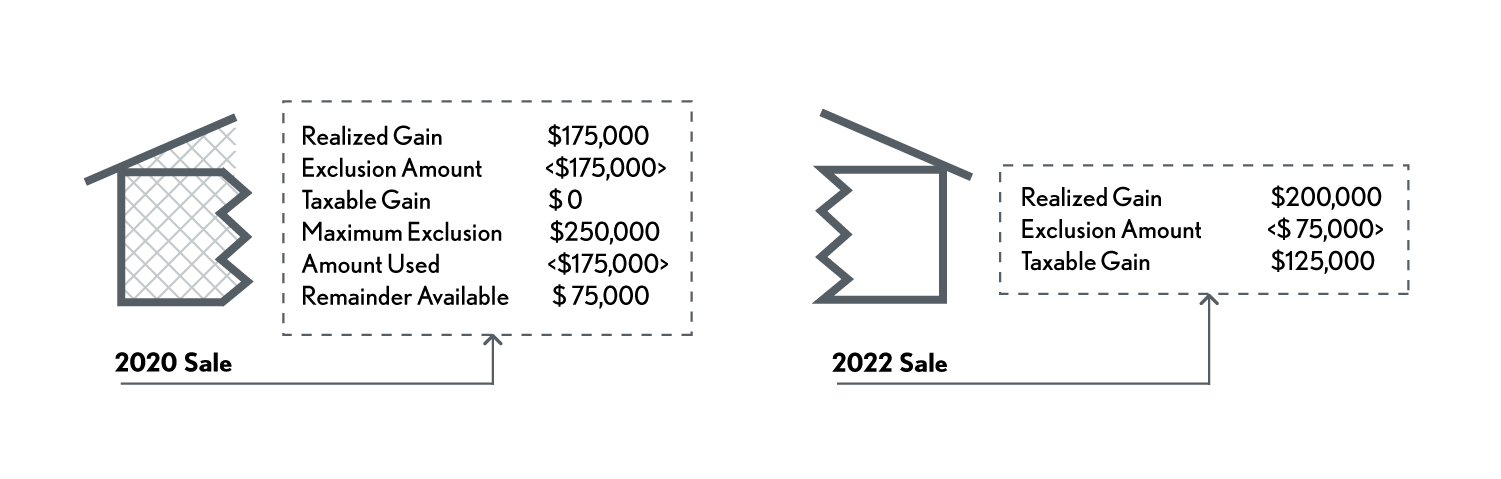

Example – Sale of a Partial and Remaining Interest - In 2013, Gil buys a house that he uses as his principal residence. In 2020, Gil’s friend Dave moves into Gil’s house and Gil sells Dave a 50-percent interest in the home. Gil realized a gain of $175,000 in the transaction. Gil may exclude the $175,000 of gain. In 2022, Gil gets married and Gil’s new wife Connie owns a home. Gil and Connie decide to live in Connie’s home, so Gil sells his remaining 50-percent interest in the home to Dave, realizing an additional gain of $200,000. Gil may exclude $75,000 ($250,000 - $175,000) of gain from sale of his remaining interest and the balance of $125,000 will be taxable.

-

The one-sale-every-two-year rule is disregarded for sales of partial interests in the same home. However, in the example above, the taxpayer could not have had another sale two years prior to the 2020 sale nor can he have one for two years after the 2022 sale. Should he, for some reason, wish to elect not to take the exclusion on the 2022 sale, he can do so by reporting the gain on his 2022 return in which case the one-sale-every-two-year rule would be based solely on the 2020 sale date.

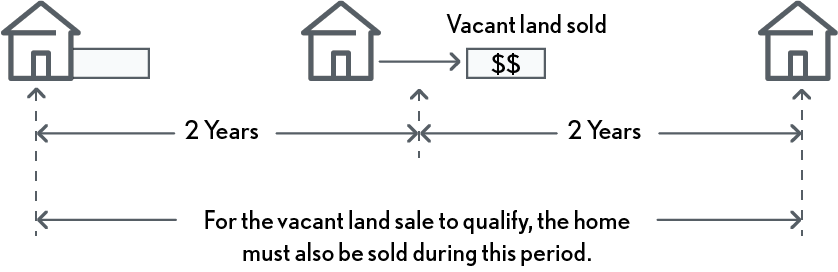

Sale of Vacant Land Adjacent to a Home

(Reg. §1.121-1(b)(3)) - In general, the sale or exchange of vacant land is not a sale or exchange of the taxpayer's principal residence unless:

-

The vacant land is adjacent to land containing the dwelling unit of the taxpayer's principal residence;

-

The taxpayer owned and used the vacant land as part of the taxpayer's principal residence;

-

The vacant land was not used for non-residential purposes (Reg § 1.121-1(e)(1));

-

The taxpayer sells or exchanges the dwelling unit in a sale or exchange that meets the requirements of Section 121 within 2 years before or 2 years after the date of the sale or exchange of the vacant land; and

-

The requirements of Section 121 have otherwise been met with respect to the vacant land.

The gain exclusion for the two transactions would be in accordance with the provisions of selling partial or remaining interests discussed previously. Caution: The Sec. 121 provisions do not apply for partial interest and remaining interest sales to related parties.

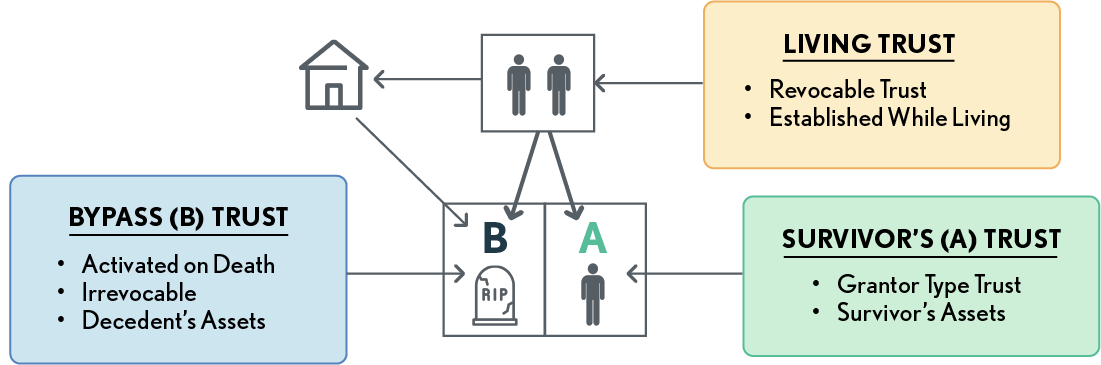

Home Sale - Revocable Trust

If a residence is owned by a trust, for the period that a taxpayer is treated as the owner of the trust or the portion of the trust that includes the residence, the taxpayer will be treated as owning the residence for purposes of satisfying the 2-year ownership requirement of Section 121, and the sale or exchange by the trust will be treated as if made by the taxpayer. (Reg. § 1.121-1(c)(3)(i))

Home Sale Exclusion – Irrevocable Trusts

Some individuals use revocable trusts as an alternative to having their property transferred by will. While there is no income or estate tax advantage to a revocable trust, there is a benefit in having the property pass to beneficiaries on the death of the owner without having to go through the probate process. A private ruling reveals a potential pitfall where a married couple transfers their residence to a revocable trust that becomes irrevocable after the first spouse dies – the $250,000 home sale exclusion may be completely lost or available only to a limited extent even though the surviving spouse has the continued right to occupy the residence.

In the ruling (PLR 200104005), the exclusion was available only to the extent the survivor was considered to own trust property. The couple, living in a community property state, established a revocable trust while both were living. Upon the death of the spouse, the trust was split into two trusts, the irrevocable bypass trust and the survivor’s revocable trust. The home was assigned to the irrevocable bypass trust and the survivor was only allowed to withdraw from the principal of the trust in each calendar year an amount not to exceed the greater of $5,000 or 5% (5 or 5 power) of the then aggregate market value of all property included in the trust.

In the letter ruling, the IRS concluded that gain on the trust's sale of the residence is taxable to the trust except for the portion of the gain that is taxable to the surviving spouse, by virtue of his 5 or 5 power. Thus, the surviving spouse may only use the Code Sec. 121 exclusion to shelter gain on the portion of the residence attributable to his 5 or 5 power.

Example – Assume the taxpayers have a revocable living trust. Upon the first spouse’s death, the irrevocable bypass (B) trust is created. If some portion of the taxpayers’ home is assigned to the bypass trust, that portion of the home does not qualify for future § 121 gain exclusion. This initially creates no problem, because the home’s basis is stepped up when it goes into the trust (and it won’t be stepped up again when the surviving spouse passes). However, if the surviving spouse continues to use the home for a number of years and the home appreciates in value and is then sold, the resulting gain for the portion of the home in the irrevocable trust would not be excludable under § 121.

-