Home Sale Transactions Get Break on IRS Information Reporting Requirements

Certain home sale transactions are subject to a break from standard IRS information reporting requirements. Learn more about Internal Revenue Code rules below.

For sales relating to the IRC Section 121 exclusion, the law creates an exception from the real estate transaction reporting requirements for any sale or exchange of a residence for $250,000 or less ($500,000 or less for a married taxpayer). To take advantage of the exception, however, the reporting person must receive written assurance, in a form the IRS approves, from the seller that:

-

The residence is the seller’s principal home,

-

If the real estate sale information return requires disclosure about whether there is federally subsidized mortgage financing assistance for the mortgage on the residence (whether old mortgage or new mortgage is unspecified in the law), that there is no such assistance,,

-

The full amount of the gain on the sale is excludable from gross income, and

-

There has been no period of nonqualified use after December 31, 2008.

Avoid CP-2000 Notice – Home Sale Gross Proceeds

The instructions for 1099-S, “Proceeds from Real Estate Transactions”, generally require the gross proceeds of sale to be reported for real estate transactions. However, it provides for an exception for the sale or exchange of a principal residence as noted above.

Problem – The instructions say the escrow company may issue a 1099-S even if the transaction meets the principal residence exclusion. Just because the selling price of a client’s home is under the exclusion limits, don’t assume a 1099-S has not been issued. Many times they are and the client may not be aware that one was issued.

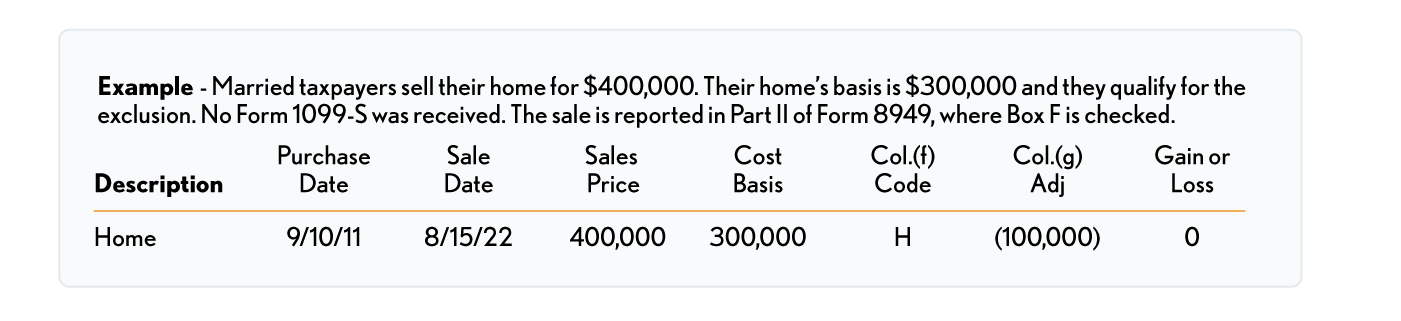

Solution – Always report the sale on Form 8949 even if the sales price is under the $250,000/$500,000 gain exclusion limits.