Home Qualifying For Sec. 121 Exclusion and Sec. 1031 Deferral

Find details about what taxpayers should do if their home qualifies for the Internal Revenue Code (IRC) Sec. 121 exclusion and the Sec. 1031 deferral.

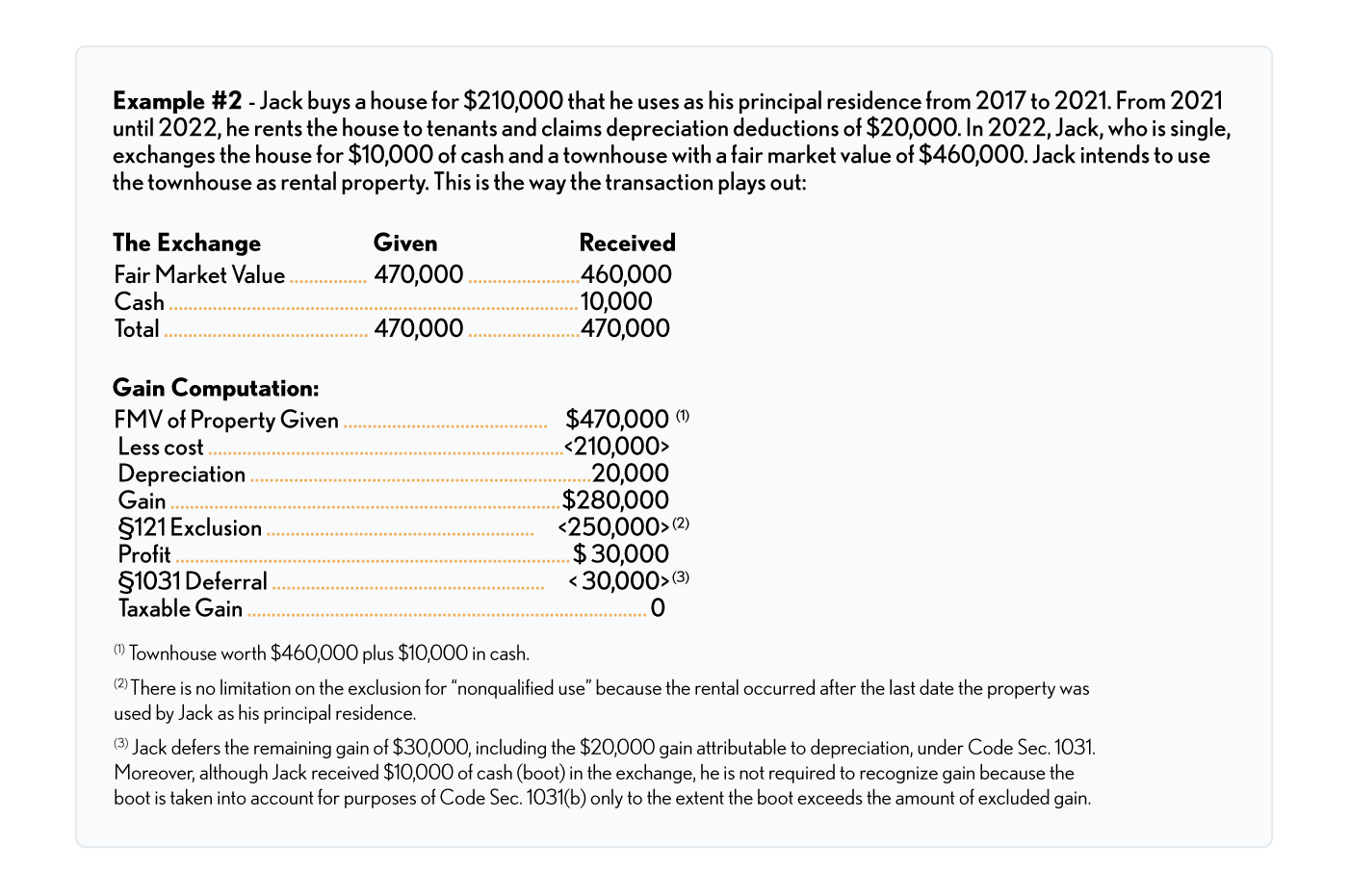

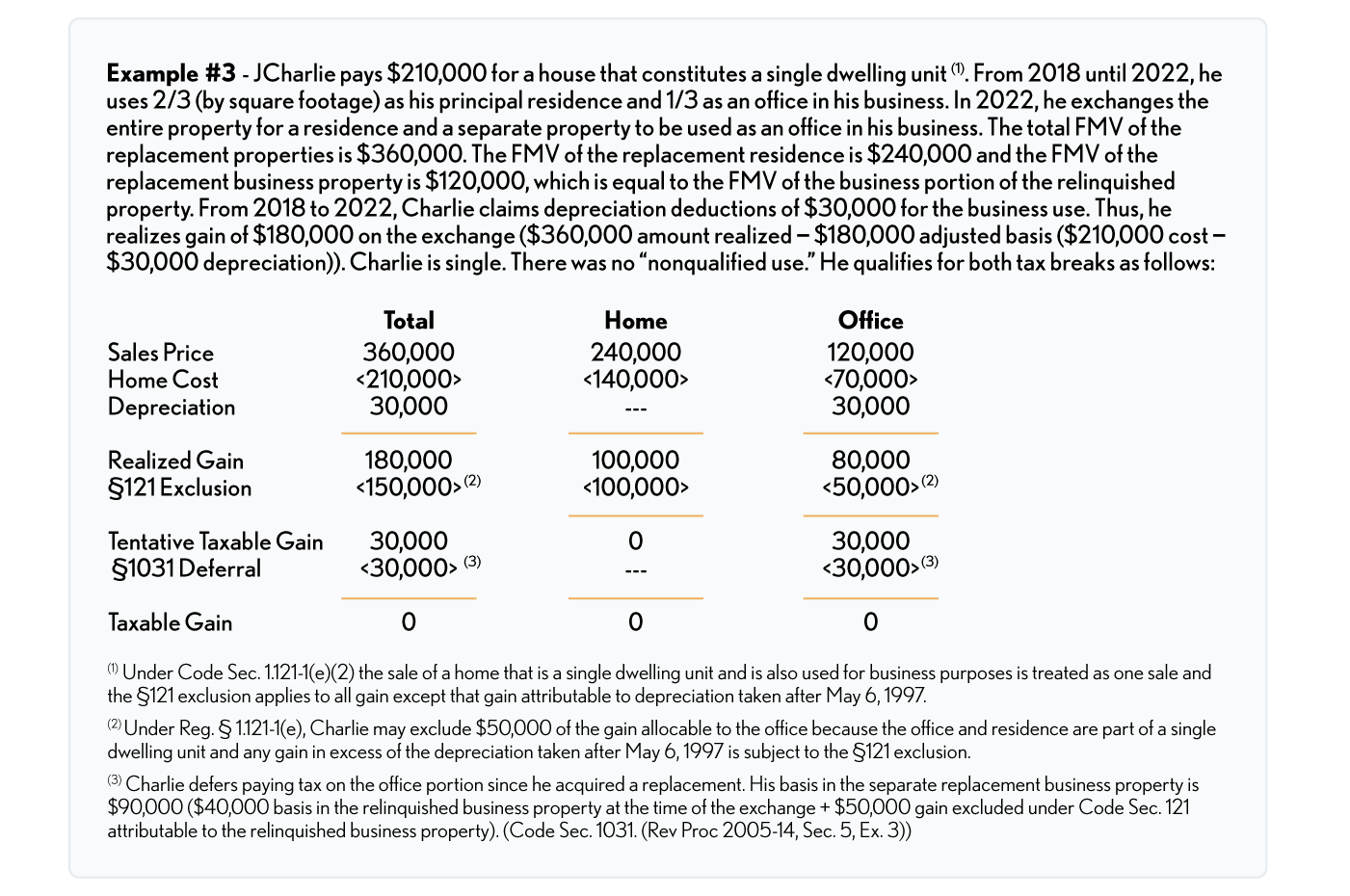

Rev. Proc. 2005-14 has made it quite clear that the exchange of a home can qualify for both the §121 home sale exclusion and §1031 like-kind exchange deferral treatment. This can occur where the property was used as a principal residence and a business consecutively (e.g., used as a principal residence followed by rental of the property) or concurrently (a portion of the home used as a principal residence and a portion used as a home office). (Rev. Proc. 2005-14) Caution: in real life, how many people selling their principal residence would structure the deal as an exchange? Merely selling a home where part has been used as an office and buying a new one where part is going to be used as an office won’t qualify as an exchange.

Consecutive Use – This would occur when a taxpayer’s home is converted to a rental property and is still being used as a rental property at the time of the exchange AND still meets the two-out-of-five ownership and use qualifications. Thus, the §121 home sale exclusion would apply and since the property is in business use, it also would qualify for §1031 like-kind exchange deferral treatment.

Concurrent Use – This would occur when a taxpayer’s home is used as a primary residence and for business purposes at the same time. A frequently encountered example would be a taxpayer with a home office.

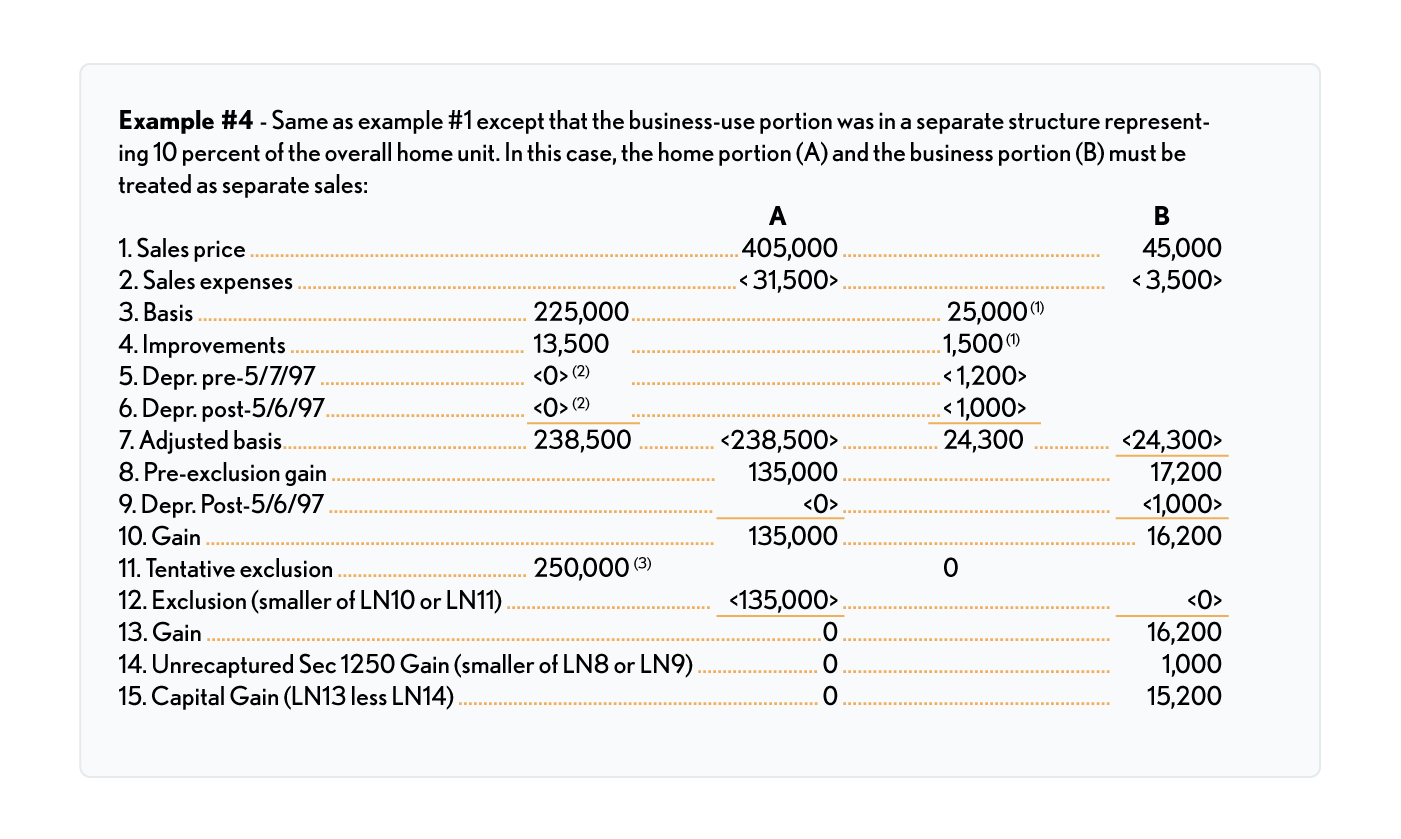

Treatment where business use is in a separate structure (Reg. § 1.121-1(e)(1)):

If the residence was mixed-use property and the business portion was in a separate structure, only that part of the gain allocable to the residential portion is excludable under §121. Therefore, the 2-out-of-5 years rule must be applied separately to the separate structure used for nonresidential (business) purposes.

EXCLUSION TEST: Does the separate structure meet the 2-out-of-5 years qualification rules?

Yes – Then the separate structure qualifies for the home sale exclusion right along with the rest of the home and the gain computation will be the same as if it were included in the same structure as illustrated previously.

No – Then the two structures are treated as separate sales. No part of the gain on the separate structure used for nonresidential purposes will qualify for the §121 exclusion. The same rules will apply to depreciation recapture with depreciation after May 5, 1997 treated as unrecaptured §1250 gain. Depreciation before May 6, 1997 adjusts the basis of the separate structure.

-

In the example, the improvements have been allocated 90% to the home structure and 10% to the business structure., In actual application, the improvements are allocated to the structure where the improvements were made., If the separate business structure was built or required substantial improvements after the home structure was acquired, the specific allocation of improvements can provide a substantial benefit to a client.

-

The depreciation may not always be allocated all to the separate structure., There could be situations where the business use was originally in the home structure and later moved to the separate structure.

-

The tentative exclusion would be $250,000 for an individual or $500,000 for a qualifying couple., The amount could also be a partial exclusion based on either of those two amounts.