Rollover of Gain on Qualified Small Business Stock (IRC § 1045)

Per (IRC § 1045), stockholders are subject to specific rules in regard to the rollover of gain on qualified small business stock.

The gain from the sale of qualified small business stock held by a taxpayer (not a corporation) for more than six months can be rolled over tax-free to other qualified small business stock. This means that the benefit of a tax-free rollover on sale of qualified small business stock by a partnership will flow through to a partner who is not a corporation, if the partner held its partnership interest at all times that the partnership held the small business stock. A similar rule applies to S corporations. There is no provision limiting the types of partners or shareholders that a partnership or S corporation may have for the benefits of the rollover rules to apply to a noncorporate partner or shareholder. Thus, even if a corporation is the majority partner in a partnership, it won’t prevent any noncorporate partner from being able to exclude from income his share of the gain on the sale of qualified small business stock that is rolled over into other qualified small business stock.

How The Rollover Works

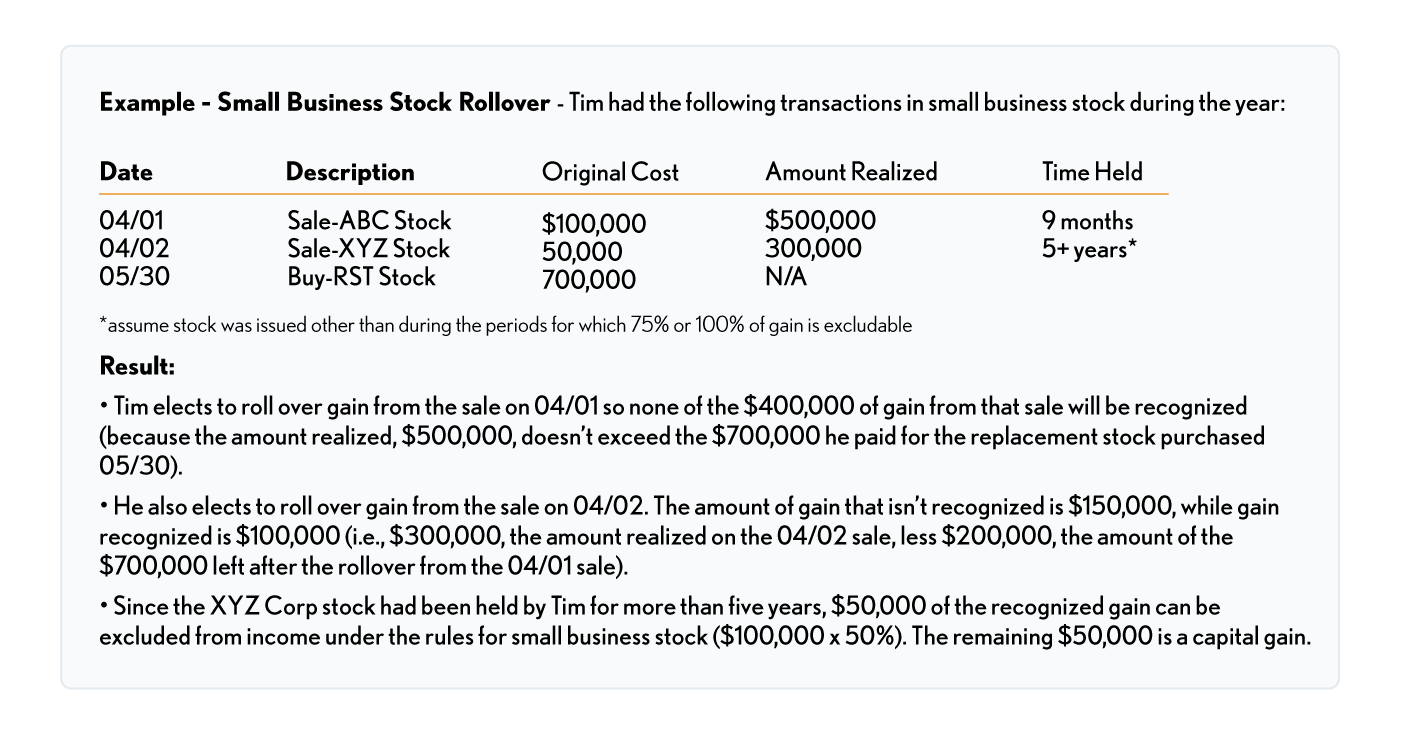

The rollover rules let taxpayers electively roll over capital gain from the sale of qualified small business stock held for more than 6 months by buying other qualified small business stock within 60 days of the sale of the original stock. If the rollover option is chosen, no tax is due currently on the transaction. In addition, the QSBS gain exclusion can be used later when the replacement stock is sold.

If rollover is elected, capital gain from the sale is recognized only to the extent that the amount realized from the sale exceeds:

• The cost of any replacement QSBS purchased within the 60-day period, reduced by

• Any portion of the cost previously taken into account under this rollover rule.

Gain from any sale not recognized due to the rollover election reduces the basis for determining gain or loss of any qualified business stock purchased by the taxpayer during the 60-day period beginning on the date of the sale.

“ Example - Basis Reduction Rule - On 04/01, Ted sold small business stock in DEF Corp; he had owned the stock for 2 years. He realized $500,000 from the sale and his basis was $100,000. On 05/29, he purchased more small business stock in GH Corp for $150,000. On 05/30, he purchased small business stock in LM Corp for $600,000.Ted’s basis in the GH Corp stock is zero and his basis in the LM Corp is $350,000 ($600,000 minus $250,000 (the amount left after $400,000 of unrecognized gain on the DEF Corp stock is reduced by the $150,000 of unrecognized gain applied against the basis of the GH Corp stock)). ”

-

Partners May Opt Out Of Partnership's Sec. 1045 Election

(Reg. Sec.

1.1045-(b)(4) and (5)) - An eligible

partner may opt out of the partnership's Sec. 1045 election with respect to QSB

stock either by recognizing the partner's distributive share of the partnership

Sec. 1045 gain, or by making a partner Sec. 1045 election with respect to the

partner's distributive share of the partnership section 1045 gain. Opting out

of a partnership's election does not constitute a revocation of the

partnership's election, and such election continues to apply to other partners

of the partnership. An eligible partner that opts out of a partnership's Sec.

1045 election must notify the partnership, in writing, that the partner is

opting out. Effective for sales 8/14/2007 and after.