Principal Residence Acquisition Debt Forgiveness Exclusion

The IRS principal debt forgiveness exclusion allows taxpayers to exclude home debt forgiveness income from their income. The following is an overview of the provision:

-

Effective: For tax years 2007 through 2025 (extended to 2025 by the Taxpayer Certainty and Disaster Tax Relief Act of 2020)

-

Exclusion: For discharges of indebtedness after 2020, the maximum exclusion is $750,000 ($375,000 MS); for discharges 2007 through 2020, up to $2 million ($1 million MFS)

-

Home: Principal Residence Only (same definition as for Sec 121 gain exclusion rules)

-

Debt: Acquisition Debt Only

-

Basis of Home: Reduced by the amount of the exclusion if retained after relief

Application

This exclusion applies where a taxpayer:

-

Restructures the acquisition debt on a principal residence,

-

Loses a principal residence in a foreclosure, or

-

Sells a principal residence in a short sale.

Limitations

-

The exclusion does not apply to a taxpayer’s designated 2nd (vacation) residence.,

-

The exclusion doesn't apply to the discharge of a loan if the discharge is on account of services performed for the lender or any other factor not directly related to a decline in the value of the residence or to the taxpayer's financial condition.,

-

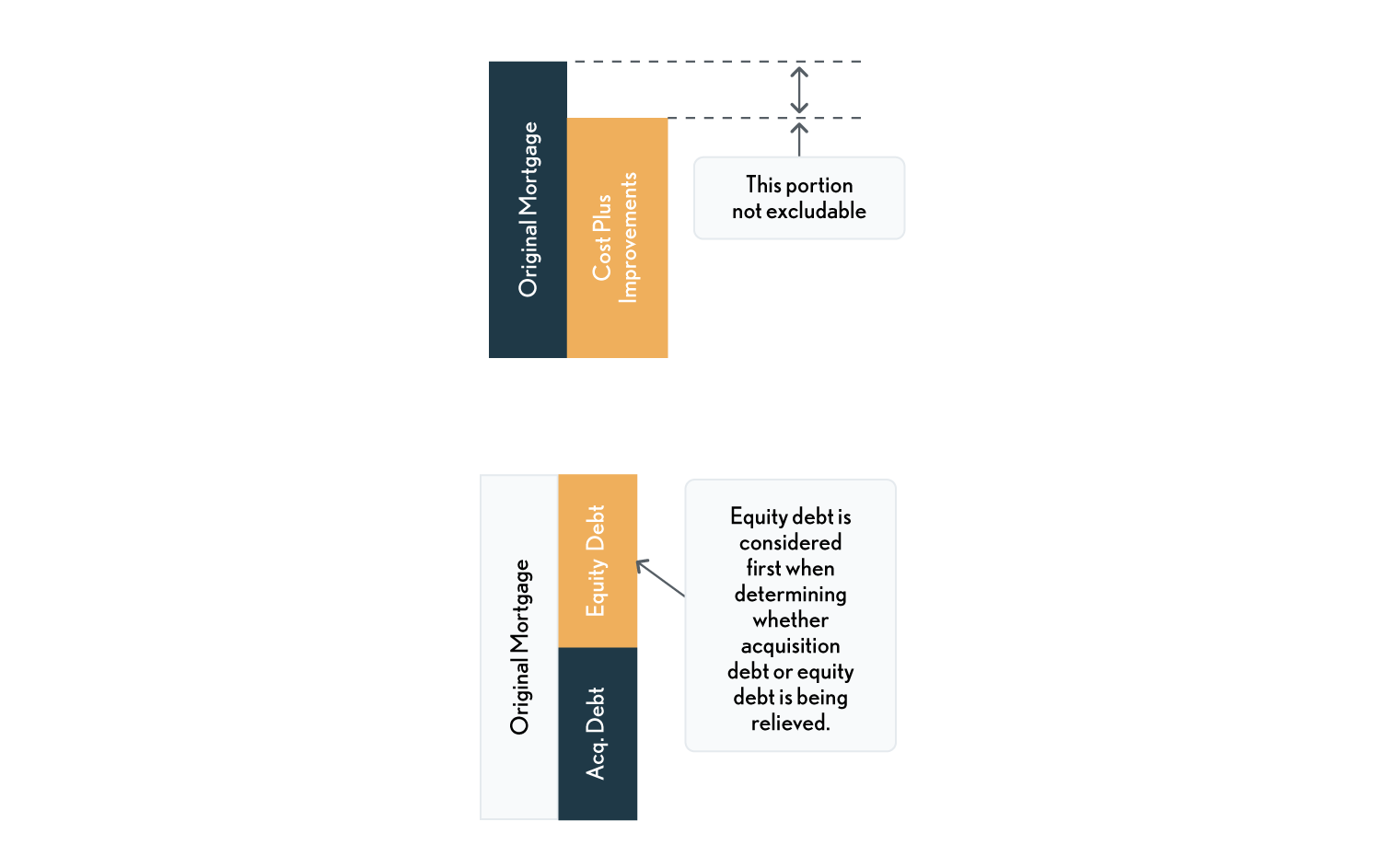

The exclusion only applies to the discharge of qualified principal residence acquisition debt., Thus equity debt is not included as part of the exclusion. Acquisition indebtedness of a principal residence is indebtedness incurred in the acquisition, construction, or substantial improvement of an individual's principal residence that is secured by the residence. It includes refinancing of debt to the extent the amount of the refinancing doesn't exceed the amount of the refinanced indebtedness. (Joint Committee on Taxation, JCX-86-07)

o Debt used to refinance qualified principal residence indebtedness is eligible for the exclusion up to the amount of the old mortgage principal just before the refinancing. (H Rept No. 110-356 (PL 110-142) p. 5)

o If the amount of the taxpayer's original mortgage is more than the cost of the principal residence plus the cost of any substantial improvements, only the debt that doesn't exceed the cost of the principal residence plus improvements is qualified principal residence indebtedness. (Form 982 Instructions, 3/2018, p. 3)

-

Forgiveness ordering rule -If only a part of a loan is qualified principal residence indebtedness, the exclusion applies only to the extent the amount discharged exceeds the amount of the loan (immediately before the discharge) that is not qualified principal residence indebtedness.

Example - Assume a principal residence is secured by a debt of $750,000, of which $600,000 is qualified principal residence indebtedness. If the residence is sold in 2022 for $550,000 and $200,000 of debt is discharged, only $50,000 of the debt discharged can be excluded (the $200,000 that was discharged minus the $150,000 of nonqualified debt). The remaining $150,000 of nonqualified debt may qualify in whole or in part for one of the other exclusions, such as the insolvency exclusion.

-

Definitions:

-

Qualified principal residence indebtedness - Qualified principal residence indebtedness means acquisition indebtedness on the taxpayer's principal residence, up to $750,000 ($375,000 for married individuals filing separately) for 2021 through 2025 discharges or up to $2 million ($1 million MFS) for 2007 – 2020 discharges.

-

Acquisition indebtedness - Acquisition indebtedness is defined as in Code Sec. 163(h)(3)(B) for purposes of the interest deduction rules. (IRC Sec. 108(h)(2))

Ordering Rule

The principal residence exclusion takes precedence over the insolvency exclusion unless elected otherwise (IRC Sec 108(a)(2)(C)). If only a part of a loan is qualified principal residence indebtedness, the exclusion from income for canceled qualified principal residence indebtedness applies only to the extent the amount canceled exceeds the amount of the loan (immediately before the cancellation) that is not qualified principal residence indebtedness. The remaining part of the loan may qualify for another Sec 108 exclusion.

Basis Adjustment

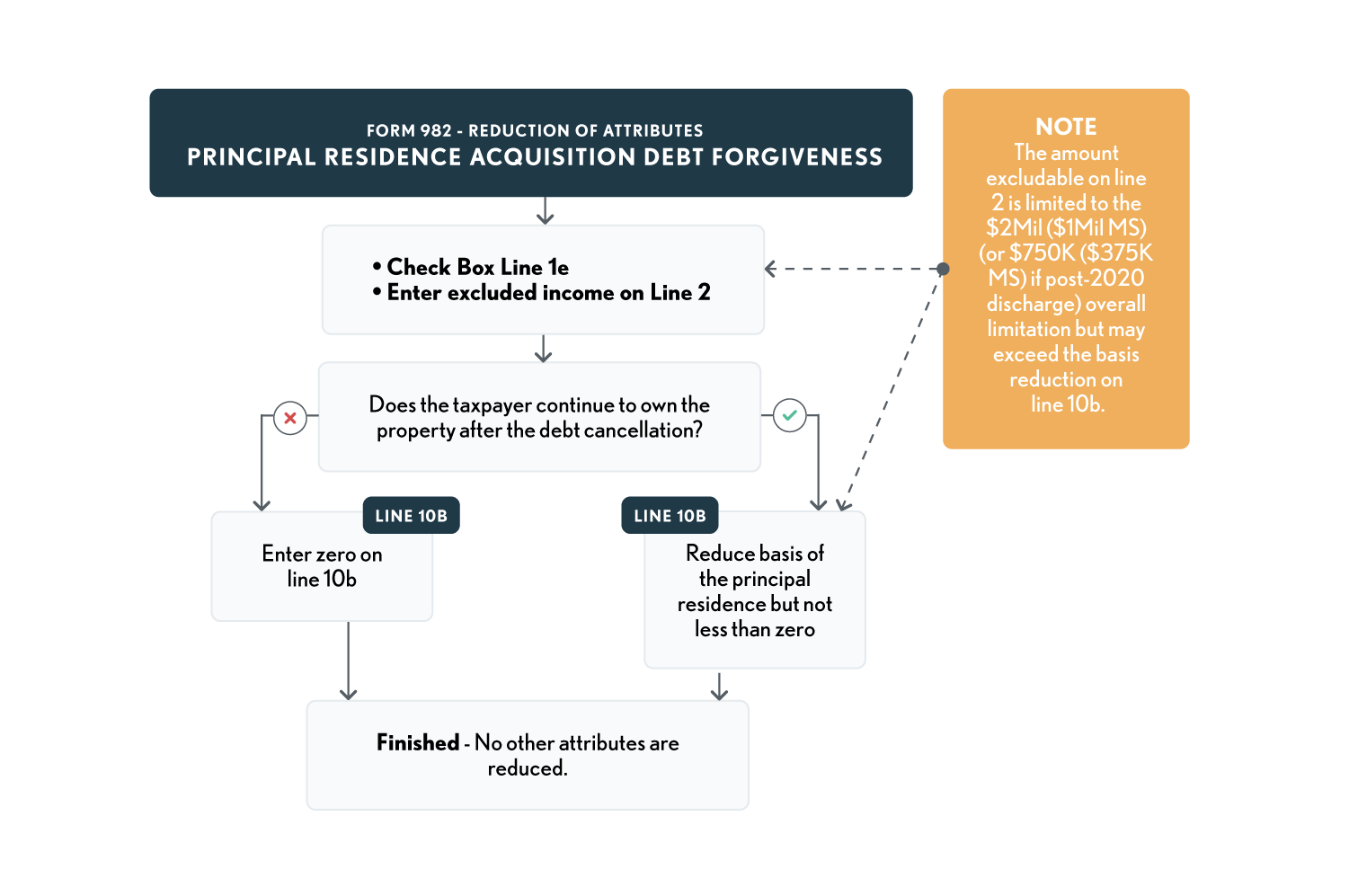

If the taxpayer excludes canceled qualified principal residence indebtedness from income and continues to own the residence after the cancellation, the taxpayer must reduce the basis of the residence (but not below zero) by the amount of the canceled qualified principal residence indebtedness excluded from income. Enter the amount of the basis reduction on line 10b of Form 982. Thus basis adjustment would be required in a loan modification where the taxpayer retains the home. However, no basis adjustment is required in a foreclosure, short sale or abandonment because the taxpayer no longer owns the residence.

This may or may not create a problem in the future since any gain will be subject to the Sec 121 home sale gain exclusion. But keep in mind: any basis adjustment as a result of COD exclusion recaptures as ordinary income and cannot be excluded using the Sec 121 exclusion (same treatment as depreciation recapture).

Electing Out of Mortgage Relief Exclusion

An insolvent taxpayer (other than one in a Title 11 bankruptcy) can elect to have the mortgage forgiveness exclusion not apply and can instead rely on the Code Sec. 108(a)(1)(B) exclusion for insolvent taxpayers. (IRC Sec. 108(a)(2)(C)) Thus, where a taxpayer has significantly tapped the equity in the home, and has a significant amount of debt discharge that does not qualify for the exclusion, it may be to their advantage to forgo the mortgage relief exclusion and instead use the insolvent taxpayer exclusion.

Things To Consider

-

The home mortgage debt forgiveness only applies to “Acquisition Indebtedness” while the insolvency rule applies to all debt.

-

The home mortgage forgiveness rule allows up to $750K of debt relief ($2 million for pre-2021 discharges) while the insolvency exclusion only allows exclusion to the extent of insolvency.

-

Some states do not conform to the home mortgage forgiveness rule and only allow the insolvent taxpayer exclusion.