Step #1 – Determine If There Is COD Income

Step #1 in a debt relief plan is to determine if there is cancelation of indebtedness (COD) income and, if so, the total sum.

Determining the amount of the COD income and the year in which it is taxable is not always readily apparent for the following reasons:

-

Personal Liability – There is no COD income where the debtor is not personally liable for the debt., That is where the lender’s only recourse is against the property secured by the debt.

-

Date of Debt Discharge – Debt discharge generally does not occur until the lender no longer has any legal opportunity for collection from the debtor, which is defined by IRS Regulations as an identifiable event., See list of identifiable events in the “Date of Debt Discharge” paragraph below.

Determining if a Loan is Recourse or Non-Recourse

Determining whether a loan is recourse or non-recourse has a huge bearing on how the COD is treated on the borrower’s tax return. If a loan is non-recourse then the borrower is not personally liable for a deficiency and the lender’s only recourse is against the secured property.

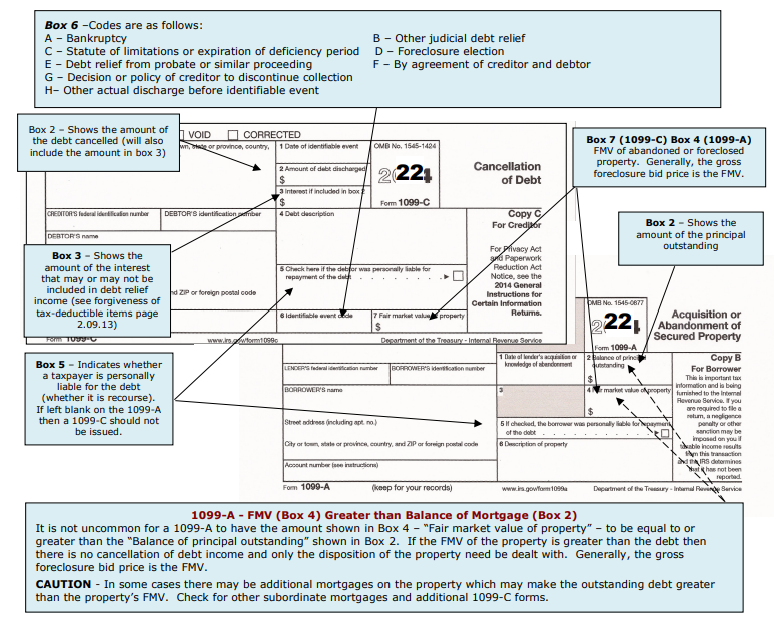

Where the borrower is not personally liable there is no COD income - Therefore it is extremely important to determine if the borrower is personally liable. Generally it is necessary to read the actual loan documents to determine whether a loan is recourse or non-recourse. Both the 1099-A and 1099-C include an entry (Box 5) for the lender to indicate whether the taxpayer is personally liable or not, but the box is frequently left blank or in some cases answered incorrectly.

Several states have statutes that prohibit lenders from seeking deficiencies from borrowers and are referred to as non-recourse states. Each non-recourse state has its own anti-deficiency statutes that prohibit lenders from seeking judgments. Not all non-recourse statutes are the same, so it is important to understand the law as it applies to your state. For example in California the statutes only apply to purchase money loans (acquisition debt) and then only if the loan is for 4 residential units or less and at least one unit is owner occupied. Almost all home equity line of credit loans – abbreviated HELOCs – and home equity loans are considered recourse loans, and lenders for these loans may sue borrowers to recoup loss, although most do not go to that expense.

The following is a list of anti-deficiency/non-recourse states.The list is from the IRS’ Real Estate Property Foreclosure and Cancellation of Debt Audit Technique Guide (8/10/21). Each of these states has its own rules and the antideficiency rules are not applied in the same manner.

-

Alaska

-

California

-

North Carolina

-

Minnesota

-

Utah

-

Arizona

-

Connecticut

-

Idaho

-

North Dakota

-

Texas

-

Washington

Date of Debt Discharge

The debt discharge generally does not occur until the lender no longer has any legal opportunity for collection from the debtor. IRS regulations (§ 1.6050P-1(a)(1)) set forth identifiable events that trigger cancellation of debt income whether an actual discharge of indebtedness has occurred on or before the date on which the identifiable event has occurred. Although the list is long, the following are the more commonly encountered identifiable events:

-

Discharge of indebtedness under title 11 of the United States Code (bankruptcy);

-

Cancellation or extinguishment of an indebtedness that renders a debt unenforceable in a receivership, foreclosure, or similar proceeding in a federal or State court;

-

A cancellation or extinguishment of an indebtedness upon the expiration of the statute of limitations for collection of an indebtedness;

-

A cancellation or extinguishment of an indebtedness pursuant to an election of foreclosure remedies by a creditor that statutorily extinguishes or bars the creditor's right to pursue collection of the indebtedness;

-

A cancellation or extinguishment of an indebtedness that renders a debt unenforceable pursuant to a probate or similar proceeding;

-

A discharge of indebtedness pursuant to an agreement between an applicable entity and a debtor to discharge indebtedness at less than full consideration; or

-

A discharge of indebtedness pursuant to a decision by the creditor, or the application of a defined policy of the creditor, to discontinue collection activity and discharge debt.

In the past, an identifiable event included the expiration of a non-payment testing period, generally a 36-month period ending on December 31. If a bank, savings and loan, credit union, or certain government agencies hadn’t received a payment on the debt of a taxpayer during that period, the lender was required to issue an information return (1099-C) reporting the debt as being canceled. However, this rule created confusion for taxpayers and, according to the IRS, did not increase tax compliance by debtors or provide the IRS with valuable third-party information that could be used to ensure taxpayer compliance. In regulations finalized in November 2016, the IRS dropped this testing period rule, applicable to information returns required to be filed, and payee statement required to be furnished, after December 31, 2016. (T.D. 9793)

No 1099-C or a 1099-C Issued in a Subsequent Year

Because of the identifiable event rules the 1099-C may show up in a year other than the year when a 1099-A is issued. The IRS provides no special guidance in situations such as this even though the regulations acknowledge that the debt relief may have occurred prior to the issuance of the 1099-C. To deal with this problem, a practitioner needs to carefully review the facts and circumstances to determine when and if debt relief actually took place. It may not necessarily be in the year when the 1099-C was issued and may have not occurred at all. Financial institutions frequently do not actually relieve the debt in the year of the foreclosure. Others may not relieve the debt at all in hopes of collecting on the liability in a future year before the state statute for the collection of a debt expires. When no 1099-C is issued there is generally no debt relief, and a practitioner should exercise caution in arbitrarily adding COD income to a client’s tax return.Where no 1099-C is issued and the practitioner has determined debt relief has occurred, the amount of the debt relieved is generally the amount in 1099-A Box 2 minus the amount in Box 4. Practitioners may wish to utilize the Form 8275 Disclosure Statement to provide an explanation of why the COD income was reported in a year when a 1099-C was not issued or why the COD income is not included in the year the 1099-C was issued. A 1099-C issued many years after a taxpayer default on a debt may be incorrect, as the debt relief may have taken place long before the year of issuance. The taxpayer and practitioner need to examine all the events surrounding the COD to determine whether the 1099-C was issued for the correct year, as the following case demonstrates. In a Tax Court summary opinion (which cannot be treated as precedent), the court ruled against the IRS, which contended debt was discharged in 2008 when the 1099-C was issued, and agreed with the taxpayer that, while it is often impossible to find just one event that clearly establishes the moment at which a debt is discharged, there was no cancellation of debt in 2008 because the debt was discharged at the end of the 36-month nonpayment testing period, which was in 1999. (TC Summary Opinion 2012-46)

Paycheck Protection Program (PPP) Loan Forgiveness – Under certain conditions, the PPP Loans were forgiven. The forgiveness, by statute, is not treated as COD income for federal purposes.

1099-C - A financial institution, credit union, federal government agency or others in the business of lending money must issue a 1099-C if the debt relief is $600 or more. Individual lenders such as the seller of the property are not required to file the 1099-C. This form will generally provide the information needed to determine the amount of debt relief. The 1099-C can be issued for a variety of circumstances related to debt forgiveness including credit card debt, vehicle repossessions, home foreclosures, etc.

1099-A - A lender who acquires an interest in a property in a foreclosure or repossession should issue Form 1099-A showing the information needed to figure the taxpayer’s gain or loss. However, if the lender also cancels part of the debt and must file Form 1099-C, the lender can include the information about the foreclosure or repossession on that form instead of on Form 1099-A. The 1099-A includes the amount of the debt relieved and the FMV of the property which should be the auction price.

Multiple Debtors - For debts for more than $10,000 that involve debtors who are jointly and severally liable for the debt, the 1099-C instructions tell the creditor (lender) to report the entire amount of the canceled debt on each debtor’s Form 1099-C. Multiple debtors are jointly and severally liable for a debt if there is no clear and convincing evidence to the contrary. However, the amount, if any, of the canceled debt income that each debtor must report depends on all the facts and circumstances, including:

-

State law,

-

The amount of debt proceeds each person received,

-

How much of any interest deduction from the debt was claimed by each person,

-

How much of the basis of any co-owned property bought with the debt proceeds were allocated to each coowner, and

-

Whether any of the COD income qualifies for any of the COD exclusions or exceptions.

If joint and several liability does not exist, a 1099-C is required for each debtor for whom canceled debt is $600 or more. The lender is only required to issue Form 1099-C for the primary or first-named debtor for debts of less than $10,000.

If the lender knows that the multiple debtors were husband and wife who were living at the same address when the debt was incurred, and the lender has no information that these circumstances have changed, then only one 1099-C need be filed. Where there are co-signers, the COD income can be allocated according to the facts and circumstances of the situation. (Chief Counsel Advice 200023001) For example where parents co-sign for a child and the child made all the payments, it would be appropriate to allocate the entire COD income to the child.

Pass-Through Entities

If a partnership’s liability is discharged, the partnership allocates the income from discharge of debt to the partners as a separately stated item. The debt relief is thus reported on Form 1040 by the partners. Any available exclusion is also applied at the partner level.

Special Rules For Partnerships

Under the final regs, partnerships don't have to inform their partners of COD income before the date the partnership return is filed.

Instead of reducing tax attributes according to the usual order specified by Code Sec. 108(b)(2), a taxpayer may elect under Code Sec. 108(b)(5) first to reduce the adjusted bases of depreciable property to the extent of excluded COD income. Excluded COD income from cancelled qualified real property business debt must, under Code Sec. 108(c), be applied against depreciable real property. A partnership interest is treated as depreciable property when applying Code Sec. 108(b)(5), and as depreciable real property when applying Code Sec. 108(c), to the extent the partnership correspondingly reduces the partner's proportionate interest in the adjusted bases of depreciable property (or depreciable real property) held by the entity (inside basis). (Code Sec. 1017(b)(3)(C))

Partnership Consent

A partnership must consent to reduce its partners' shares of the partnership's depreciable basis in property only if consent is requested by:

-

partners owning (directly or indirectly) an aggregate of more than 80% of the partnership's capital and profits interests, or,

-

five or fewer partners directly or indirectly owning more than 50% of those interests.,

If partners meeting either of these tests elect to exclude COD income from the partnership, the partnership must consent to reduce the basis of its depreciable property (or depreciable real property). (Reg. § 1.1017-1(g)(2)(ii)) In other situations, partners may request the partnership to reduce basis and the partnership may or may not consent to do so.

The partner must request and receive the consent of the partnership before the due date (including extensions) of the partner's return for the year the COD income is received. However, the partnership does not have to attach its consent statement to its return until the filing date for the tax year following the year that the partner excludes the COD income. (Reg. § 1.1017-1(g)(2)(iii))