California Differences - Filing Status

Filing status for California must generally be the same as the filing status used on the federal income tax return.

Exceptions - Married taxpayers who file a joint federal income tax return may file either a joint return or separate returns if either spouse was:

-

An active member of the United States armed forces or any auxiliary military branch during the tax year; or

-

A nonresident for the entire year and had no income from California sources during the tax year. However, if the taxpayers file a joint return and if either spouse was a nonresident during the tax year, the taxpayer must file Form 540NR, California Nonresident or Part-Year Resident Income Tax Return.

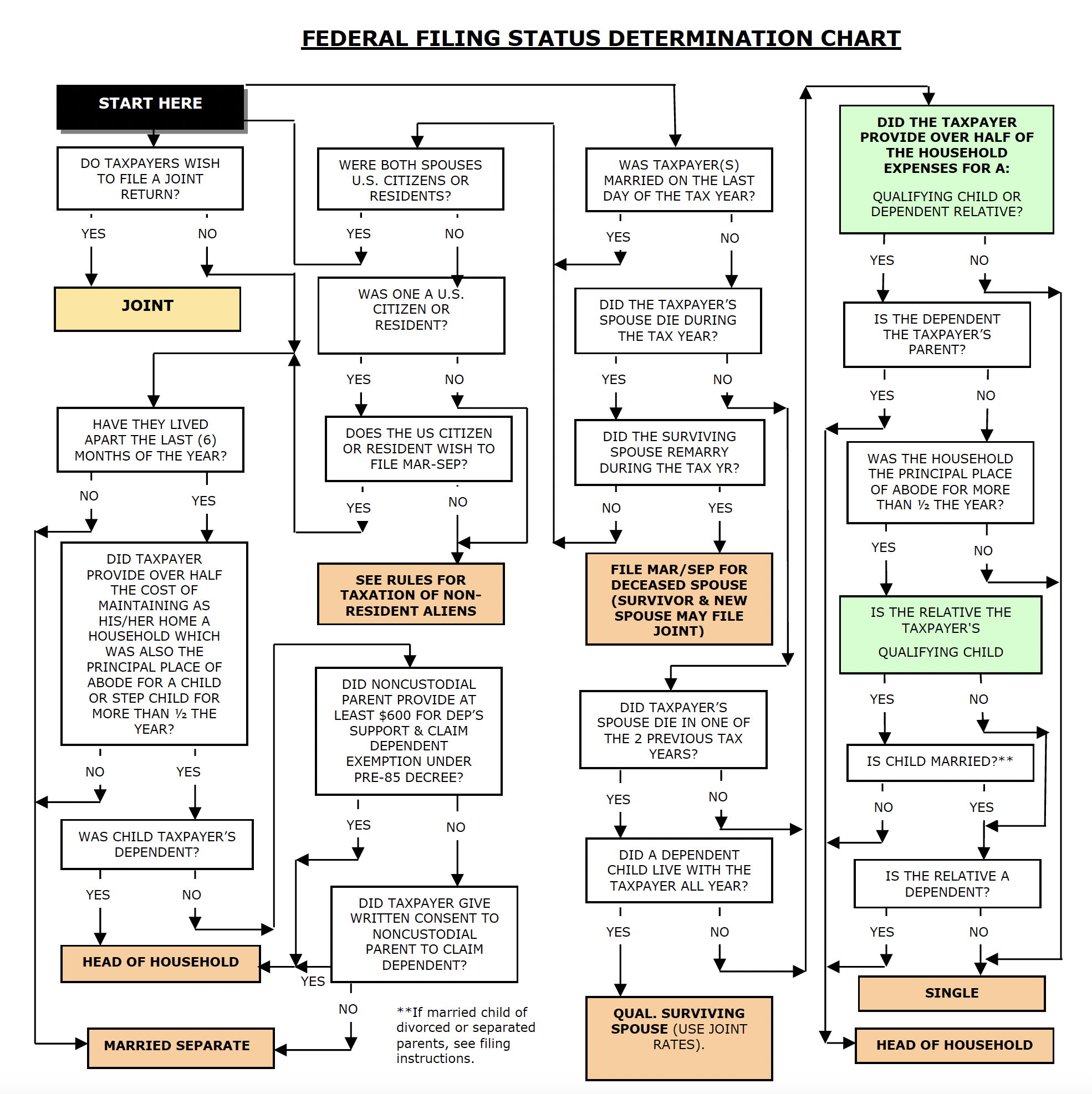

Qualifying for Head of Household While Still Married - California follows the federal rule that allows a married individual to use the head of household status if he or she (a) lived apart from their spouse at least the last six months of the year, and (b) paid more than one-half of the cost of maintaining as his or her home a household which is the principal place of abode for more than one-half the year of a child, stepchild or eligible foster child for whom the taxpayer may claim a dependency exemption. The “lived apart” requirement is unchanged by an amendment to the California Family Code (SB 1255, Stats. 2016, chapter. 114, 7/25/16) regarding the definition of “date of separation.” Under that revision, date of separation is the date that a complete and final break in the marital relationship has occurred as evidenced by the spouse’s expression of his or her intent to end the marriage and conduct that is consistent with that intent. In other words, for purposes of the Family Code, the spouses don’t have to live in separate residences to establish a date of separation, but for Head of Household qualification purposes, they must still meet requirement (a) above. (FTB News, Sept. 2017). The HoH status could not be used in this situation for federal, even if the RDP met the “lived apart” rule because RDPs are not considered married for federal purposes.

FTB Form 3532 - For taxable years beginning on or after January 1, 2015, California requires taxpayers who use the head of household filing status to file form FTB 3532, Head of Household Filing Status Schedule, with their Form 540, 540NR or 540 2EZ to report how the head of household filing status was determined.

Common Law Marriages - California abolished common law marriages by statute in 1895. However, CA has recognized common law marriages originating in states that recognize common law marriages. Reference: Appeal of Estate of Lawrence Foley, Deceased,77-SBE-100, 7-26-77