Options For Holding Title to California Property

California is a community property state, and married couples in the Golden State have three options for holding title to property:

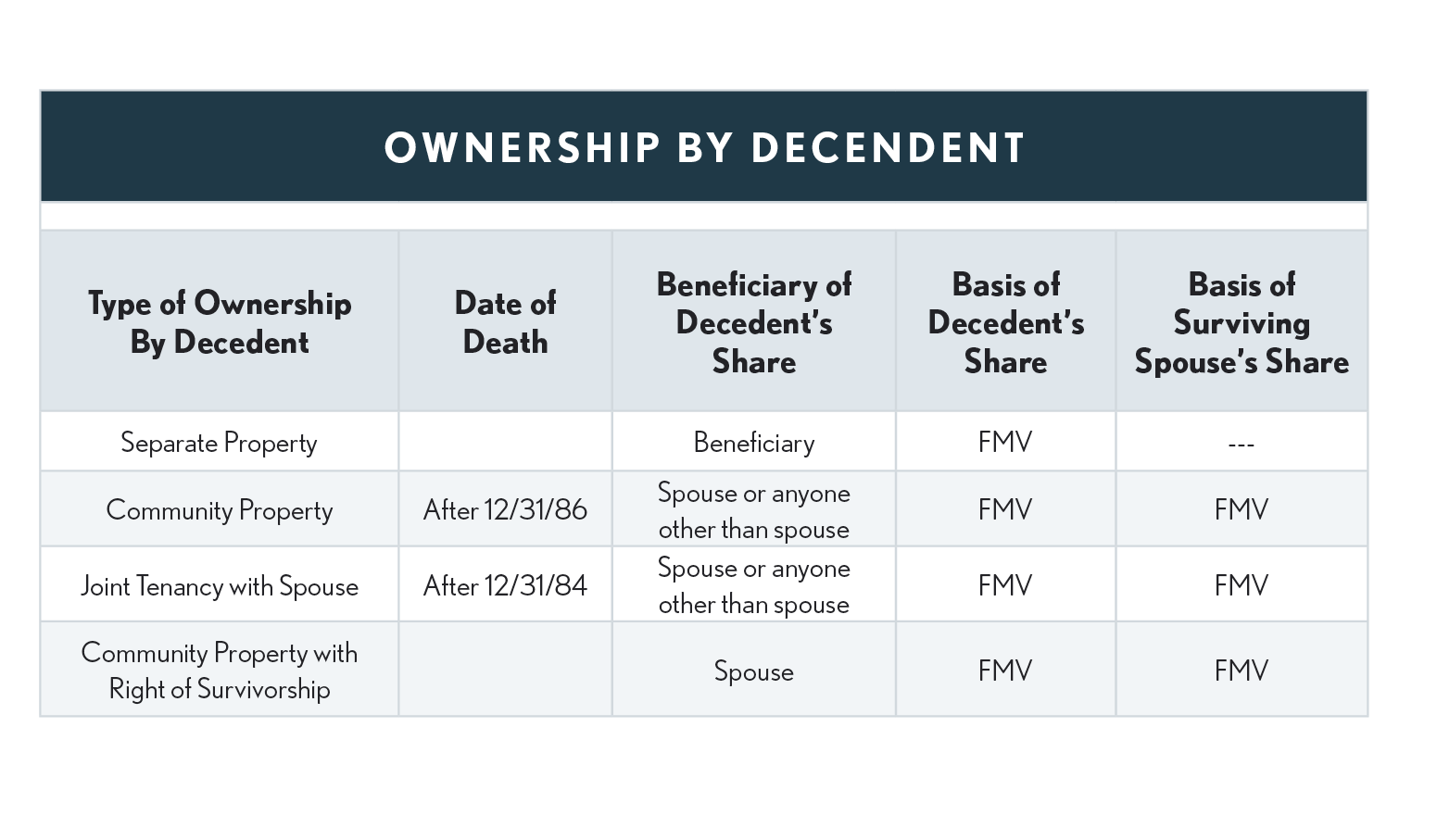

Joint Tenancy - Guarantees that the surviving spouse will inherit the property with little or no transfer cost. The survivor is also assured of inheriting the decedent's share since a secret will cannot divest a joint tenancy interest. However, the surviving spouse receives a step-up (or step-down) in basis of only 50% of the FMV at the time of the decedent's death. The remaining 50% retains the surviving spouse's original basis.

Community Property - Provides a 100% step-up (or step-down) of the property's basis when one of the spouse’s dies. Both the decedent's and the survivor's halves get a new basis of the FMV upon the death of the first spouse. Unlike joint tenancy, each spouse can will his or her share of the community property to anyone at all. Changing title requires filing a "spousal property petition" and generally will cause the surviving spouse to incur legal costs and can take up to 6 to 8 weeks.

Community Property with Right of Survivorship - Combines the tax benefits of holding title as community property with the ease of property transfer available to the survivor of joint tenancy property. Holding title this way results in a double step-up (or step-down) in basis; requires that the surviving spouse inherit the property; and allows the property to pass to the surviving spouse without court action.

General Presumption of Community Property – There is a general presumption that all real property in California and all personal property wherever situated, that is acquired by a spouse during marriage, is community property (Family Code Sec 760). The presumption may be overcome (rebutted) by certain types of evidence to prove that the property is actually separate. Some property acquired during marriage is specifically excluded from the community property presumption (Family Code Sec. 802 and 803). The general community property assumption specifically applies to:

-

All real property (including leased) that is located in California and acquired during marriage by a spouse while domiciled in California (Family Code Sec 760).

-

All personal property, wherever located that is acquired during marriage by a person while domiciled in California (Family Code Sec 760).

-

All community property transferred by husband and wife to a trust pursuant to Family Code Sec 761.