Age-Related Tax Issues

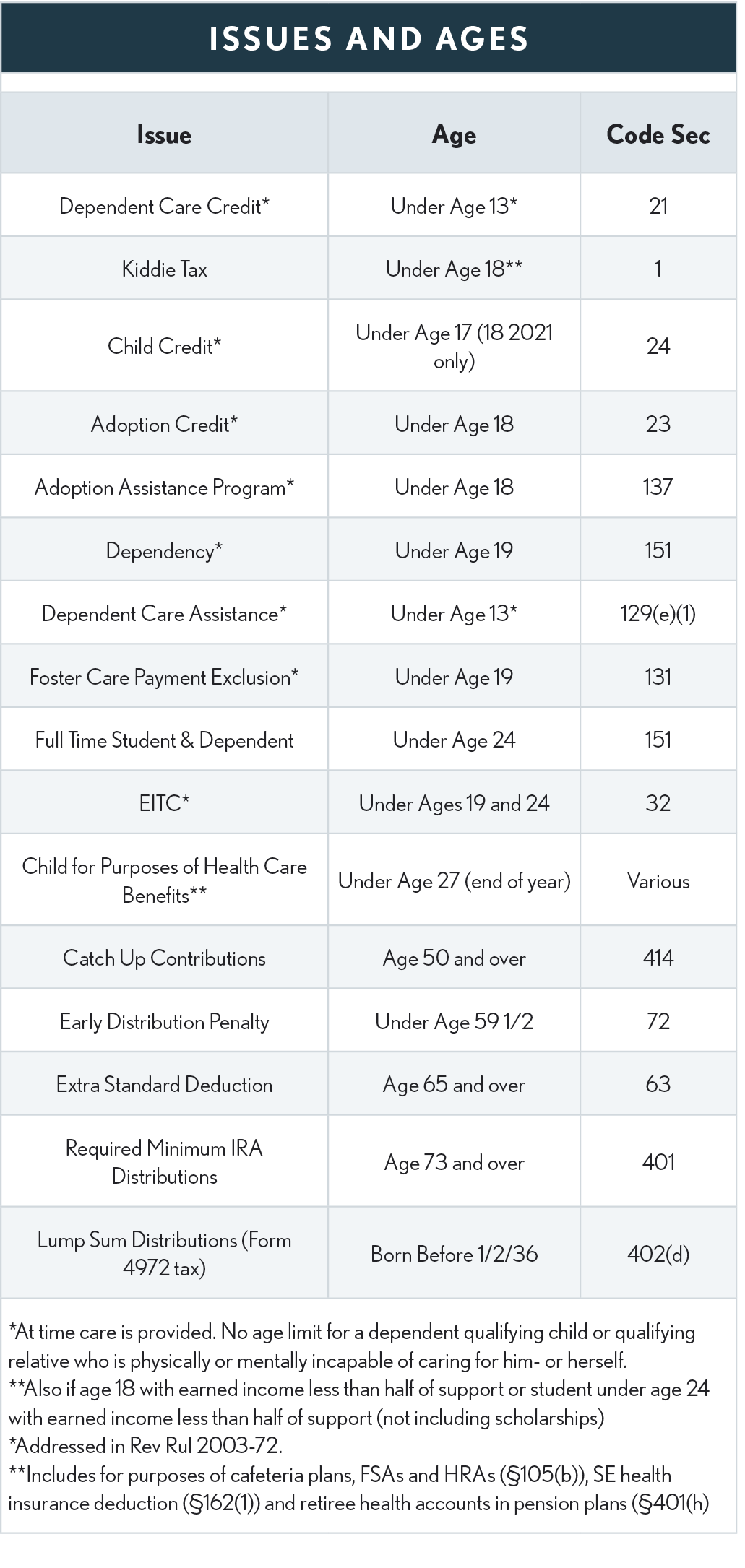

Since age plays a major role in filing taxes, it is important to understand precisely how the IRS defines a taxpayer's age. This can be especially important in regard to the child tax credit (CTC) and other tax breaks.

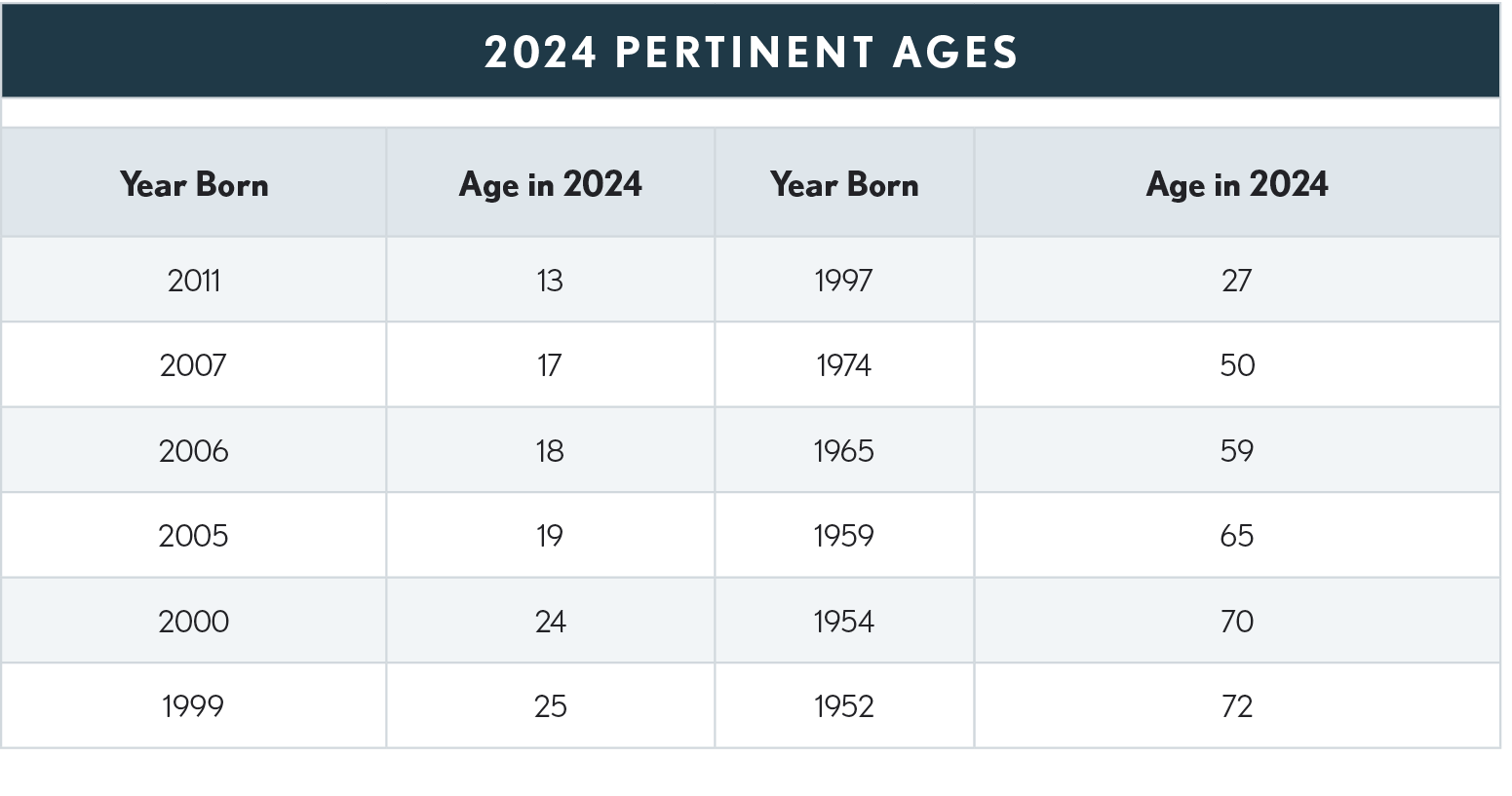

Age - Birthday or Day Before? Since tax law includes a number of age-related issues, the date on which a taxpayer attains a specified age can have an impact on his or her income tax and the income tax of others. Per common law,a person attains a given age on the day before his/her birthday. This common law rule is why the IRS has held a person whose 65th birthday is Jan. 1 gets the additional standard deduction for the prior year.

However, in other circumstances, the common law rule has a negative impact on the taxpayer. So, the IRS in Rev Ruling 2003-72 (IRB 2003-33, 8/18/2003) has ruled for purpose of various provisions included in the list below that a child attains a given age on the anniversary of the date that the child was born. For example, a child born on January 1, 2007, attains the age of 17 on January 1, 2024. The IRS reiterated this provision in Notice 2010-38 with respect to the items on the list related to changes enacted as part of the 2010 health care reform legislation.

Many of these provisions allow a credit, exclusion, or deduction to the taxpayer, provided, among other requirements, an individual has not attained a specific age. For example, under § 24(c), one of the requirements for a qualifying child for the child tax credit (CTC) is that the child “has not attained the age of 17 as of the close of the calendar year in which the taxable year of the taxpayer begins.” So, for example, a child born on January 1, 2008, attains the age of 17 on January 1, 2025, and would qualify for the credit for 2024 but not 2025.

The ARPA changed the CTC eligibility age for 2024 by allowing the credit for qualifying children who haven’t reached age 18 by the end of 2024.