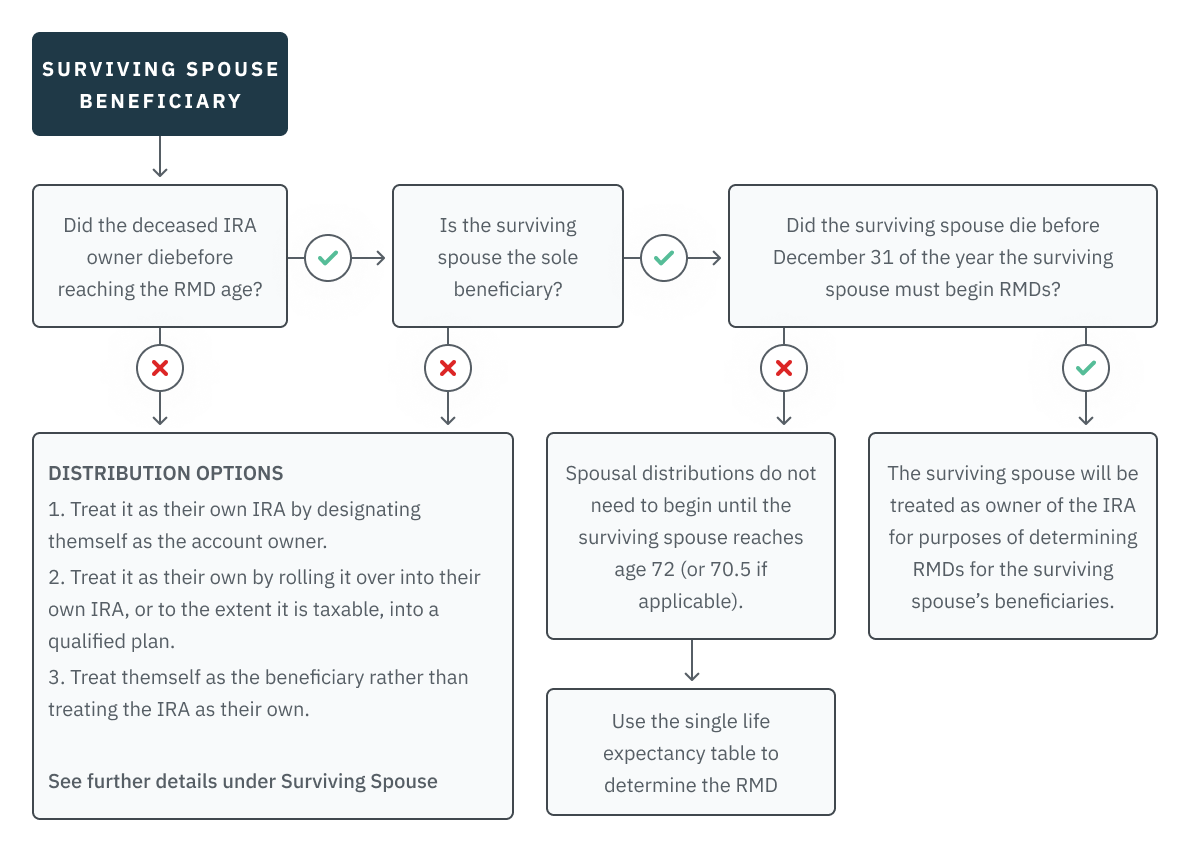

Surviving Spouse Beneficiary

The SECURE Act did not alter the options available to spouse beneficiaries that include:

-

Treat it as their own IRA by designating themself as the account owner.

-

Treat it as their own by rolling it over into their own IRA, or to the extent it is taxable, into a: a. Qualified employer plan

-

Qualified employee annuity plan (section 403(a) plan)

-

Tax-sheltered annuity plan (section 403(b) plan)

-

Deferred compensation plan of a state or local government (section 457 plan); or

-

-

Treat themself as the beneficiary rather than treating the IRA as their own.

Treating IRA as their own - The surviving spouse will be considered to have chosen to treat the IRA as their own if:

-

Contributions (including rollover contributions) are made to the inherited IRA, or

-

The surviving spouse does not take the required minimum distribution for a year as a beneficiary of the IRA.

The surviving spouse will only be considered to have chosen to treat the IRA as their own if:

-

The surviving spouse is the sole beneficiary of the IRA, and

-

The surviving spouse has the unlimited right to withdraw amounts from it.

However, if the surviving spouse receives a distribution from the deceased spouse's IRA, the surviving spouse can roll that distribution over into their own IRA within the usual 60-day time limit for rollovers, provided the distribution isn’t an RMD. This is true even if the surviving spouse is not the sole beneficiary of the deceased spouse's IRA.

Surviving spouse is sole designated beneficiary - If the IRA owner died on or after the RMD required beginning date and the surviving spouse is the sole designated beneficiary, the life expectancy the spouse must use to figure the RMD may change in a future distribution year. This applies where the spouse is older than the deceased owner or the spouse treats the IRA as his or her own.

Special Rules for Sole Surviving Spouse

-

Deceased IRA owner died before reaching the RMD starting date

-

Spousal distributions do not need to begin until the surviving spouse reaches age 73 (years 2023 through 2032).

-

If the surviving spouse dies before December 31 of the year the surviving spouse must begin RMDs, the surviving spouse will be treated as the owner of the IRA for purposes of determining RMDs for the surviving spouse’s beneficiaries.

-

Use the Single Life Expectancy table to determine the surviving spouse’s RMD.

-

Example #1: An IRA owner, Alex, died in 2019 at the age of 65. Alex’s sole surviving beneficiary is his spouse, Betty, who will not be required to take an RMD until December 31, 2027, the year Alex would have reached age 73. If Betty dies prior to that date, she will be treated as the owner of the IRA for purposes of determining the required distributions to her beneficiaries. So if Betty dies in 2024, which is before reaching the RMD date (12/31/27), her beneficiaries must start taking distributions under the general rules for an owner who died prior to the required beginning date.

-

Example #2: Let’s say that Betty from Example #1 marries Chad in 2021 and Betty dies in 2024. Chad is the sole beneficiary of the IRA. Chad cannot delay beginning distributions until Betty would have reached age 73, and as result will have to start taking distributions in 2025 based on his life expectancy (or Chad can elect to fully distribute the account under the 10-year rule by the end of 2034).

-