Railroad Retirement

Find details about the pension and annuity reporting process for retired railroad workers in this section of TaxBuzz Guides.

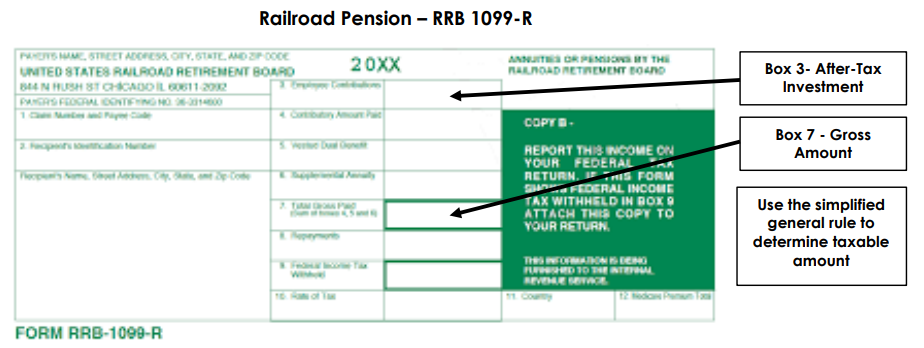

Pensions and annuities paid by the Railroad Retirement Board (RRB) are reported on Form RRB-1099-R, which is a green form, as opposed to the blue RRB-1099, which reports RR equivalent Social Security benefits. Box 7 of the RRB-1099-R shows the gross amount paid, without any reduction for taxpayer contributions. Box 3 shows the employee’s after-tax investment in the contract – use the simplified general rule to determine the amount that reduces the taxable amount reported in Box 7. Box 8 shows any repayments. See chapter 9.05, Claim of Right, for how to deduct or take a tax credit for the repayment. For additional information on Railroad Retirement benefits, see IRS Pub 575, page 6 (2021).

Residents of the U.S. and beneficiaries of one of the following Canadian plans:

-

A registered retirement savings plan (RRSP)

-

A registered retirement income fund (RRIF)

-

A registered pension plan, or

-

A deferred profit-sharing plan

Have been taxed on the accrued earnings from these plans unless they made the election under the US-Canada Tax Treaty Article XVIII(7).

IRS Rev. Proc. 2014-55

Simplified the reporting requirements. Previously Form 8891 was used to report contributions to, undistributed earnings of and distributions from the Canadian plans and to make the election under the US-Canada Tax Treaty Article XVIII(7) to defer taxation on undistributed earnings.

An eligible individual can make that election under the provisions of Rev Proc 2014-55. An “eligible individual” is a beneficiary of a Canadian retirement plan who:

-

Is or at any time was a U.S. citizen or resident while a beneficiary of the plan;

-

Has met his or her U.S filing requirements for all years during which the individual was a U.S. citizen or resident;

-

Has not previously reported undistributed accrued earnings from a plan during any taxable year in which the individual was a U.S. citizen or resident; and

-

Has reported any and all distributions received from the plan as if the individual had made an election under Article XVIII(7) for all years during which the individual was a U.S. citizen or resident.

Election Procedure for an Eligible Individual

An eligible individual (defined above) who did not previously make an election under Article XVIII(7) will be treated as having made the election in the first year in which the individual would have been entitled to elect the benefits under Article XVIII(7). No forms need to be filed for any year. Once an election is made pursuant to section 4.02 of Rev Proc 2014-55 with respect to a Canadian retirement plan, that election is in effect for all subsequent taxable years through the year in which a final distribution is made from the plan, unless the election is revoked with the consent of the Commissioner.

Effect on Prior Elections

A beneficiary who previously made an Article XVIII(7) election with respect to a Canadian plan on Form 8891 or under the procedures set forth in Revenue Procedure 2002-23 (or an eligible individual who is treated as having made the election per Rev Proc 2014-55) is not required to file Form 8891 or a similar statement for taxable years ending after December 31, 2012.

Effect on Other Than an Eligible Individual

Beneficiaries who have reported on their U.S. Federal income tax return undistributed income that has accrued in a Canadian retirement plan during a taxable year are not “eligible individuals” and consequently are not eligible to make an election under Article XVIII(7). Undistributed income will remain currently taxable. If such a beneficiary desires to make an Article XVIII(7) election with respect to a Canadian retirement plan, the beneficiary must seek the consent of the Commissioner.

Note: Annuitants and beneficiaries of these Canadian plans are not required to file Form 3520 or 3520-A. However, beneficiaries may be required to file FinCEN Form 114 (FBAR) related to foreign financial accounts and trusts valued at over $10,000.

Other Issues: Exchange – Inherited Annuities

According to PLR 201330016, a taxpayer who had elected to annuitize her inherited non-qualified annuities (elected to receive the pay-out over her lifetime) was allowed to exchange those annuities for annuities with higher pay-outs as provided by IRC Sec. 1035(a)(3). A PLR is non-binding and only applies to the taxpayer who made the request, but it also shows how the IRS regards a certain issue.