Methods For Taxing Pensions

There are two main methods for taxing pensions. Learn about fully taxable pensions and partially taxable pensions below.

Schedule a consultation with a qualified local tax expert if you have questions about the taxation of your personal pension plan.

Fully Taxable Pensions

Payments are 100% taxable if there is no investment in the contract. Most often these pensions consist of distributions from cash or deferred arrangements (401(k) plans), simplified employee pensions (SEPs), or tax-sheltered annuities.

Partially Taxable Pensions

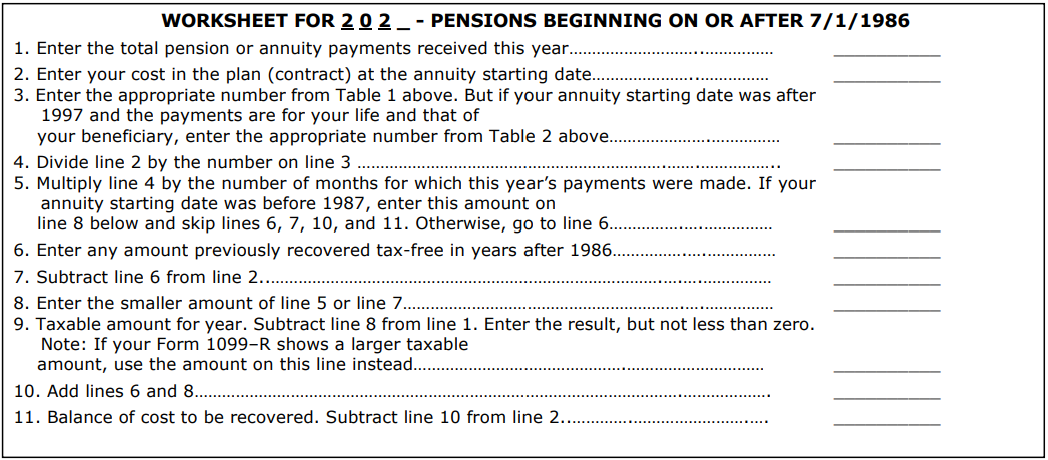

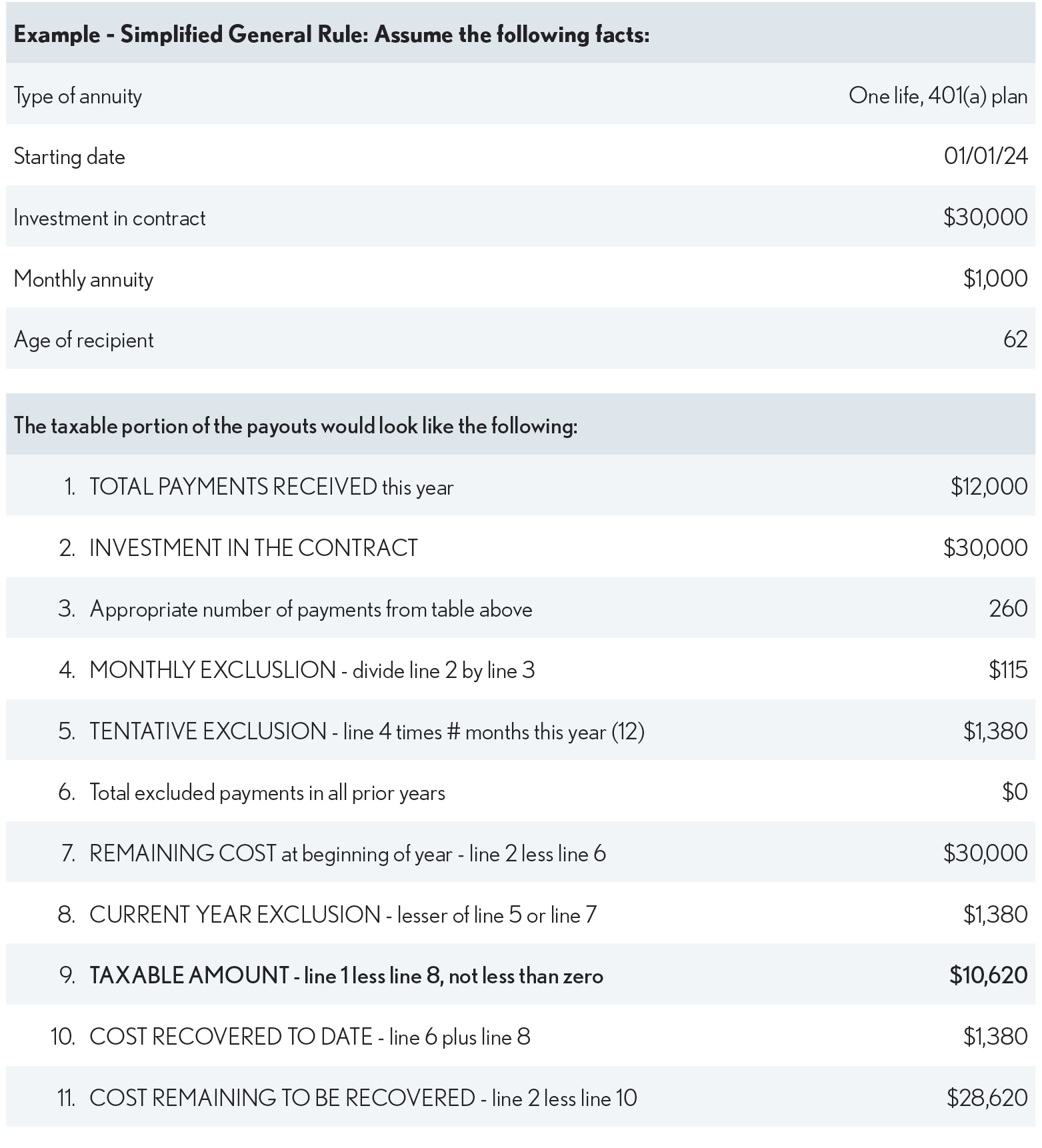

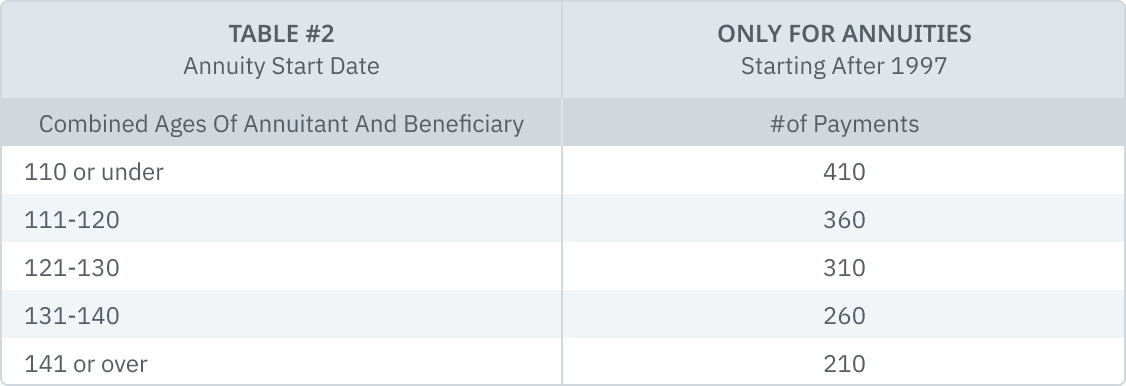

For pensions that begin after 1986, the “Simplified General Rule” is used to compute the taxable portion of a pension when there is an investment in the contract. There are two “General Rules” - one effective for pensions that began after 11/18/1996 and those started before that date.

To determine the taxable portion of a partially taxable pension using the general rule, use the adjacent Simplified General Rule tables and the worksheet below.