Figuring The Contributions

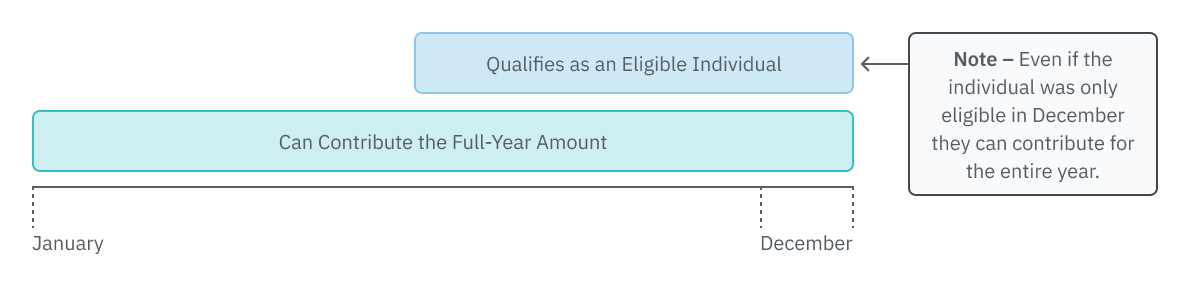

Individuals Who Are Eligible on the Last Day of the Year

An eligible individual who establishes an HSA plan during the year and is still an eligible individual during the last month of the year (December) can contribute the full-year amount (does not need to prorate the contribution). Notice 2008-52, 2008-25 IRB 1166

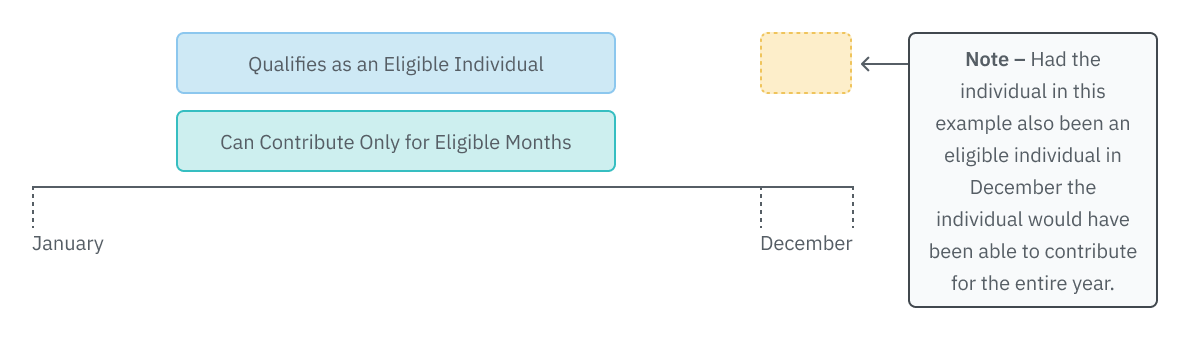

Individuals Who Are NOT Eligible on the Last Day of the Year

An individual who was eligible during the year but not eligible during the last month of the year (December) must prorate their contributions for the year. Notice 2008-52, 2008-25 IRB 1166

Correcting Contributions Made for Ineligible Periods

When an individual’s full-year contribution was based on the “last month” rule (i.e., when considered to be an eligible individual for the entire year if an eligible individual on the first day of the last month of the tax year – December 1 for most taxpayers), the individual must remain eligible during a “testing period.” The testing period begins with the last month of the tax year and ends on the last day of the 12th month following that month. For example, the testing period for a calendar-year individual who became eligible on December 1, 2024, would be December 1, 2024, through December 31, 2025. If, at any time during a particular testing period the individual is not an “eligible individual”, except by reason of death or a disability, then:

-

The individual's gross income for the tax year that includes the first month in the testing period for which he is not an eligible individual is increased by the aggregate amount of all of his HSA contributions which could not have been made; and

-

A 10% additional tax will be imposed for any tax year on the amount of the increase described in item (a), above. (Code Sec. 223(b)(8)(B); Notice 2008-52, 2008-25 IRB 1166)

No Contributions After Enrollment in Medicare

After an individual has reached the Medicare eligibility age (generally 65), and has actually enrolled in Medicare, including Medicare D, no further contributions, including catch-up contributions, can be made to the individual’s HSA.

Example – Computing Contribution in Year Enrolling in Medicare: Becky’s 65th birthday is in July 2025, at which time she enrolled in Medicare. Becky was participating in self-only coverage under an HDHP with an annual deductible of $1,800. She is not eligible to make HSA contributions after June 2025. Her monthly contribution limit is $441.66 (($4,300/12) + ($1,000/12)) and the maximum she may contribute for the year is $2,650 (6 x $441.66)) for coverage from January through June.

-

Spouse with Family Coverage

Where a husband and wife each has family HDHP coverage, the general rule is that each spouse may set up a separate HSA and they may divide the HSA annual contribution limit between them as they wish. If each spouse has just self-only HDHP coverage, each spouse may contribute to their respective HSA. If either spouse of a married couple has family coverage, both are treated as having family coverage. If each spouse has family coverage under a separate health plan, both spouses are treated as covered under the plan amount divided equally between the spouses, unless they agree to a different division. Both spouses may make the catch-up contribution for individuals age 55 or over without exceeding the family coverage limit.

When Can Contributions Be Made?

Contributions can be made in one or more payments at any time from January 1 of the tax year up to the unextended due date for filing the eligible individual’s federal return for the tax year (usually April 15 for calendar year filers). Although the annual contribution is determined monthly, the maximum contribution may be made on the first day of the year. However, if the individual is later determined not to be eligible for the entire year, some or all of the contribution is treated as an excess contribution.