What is an FSA?

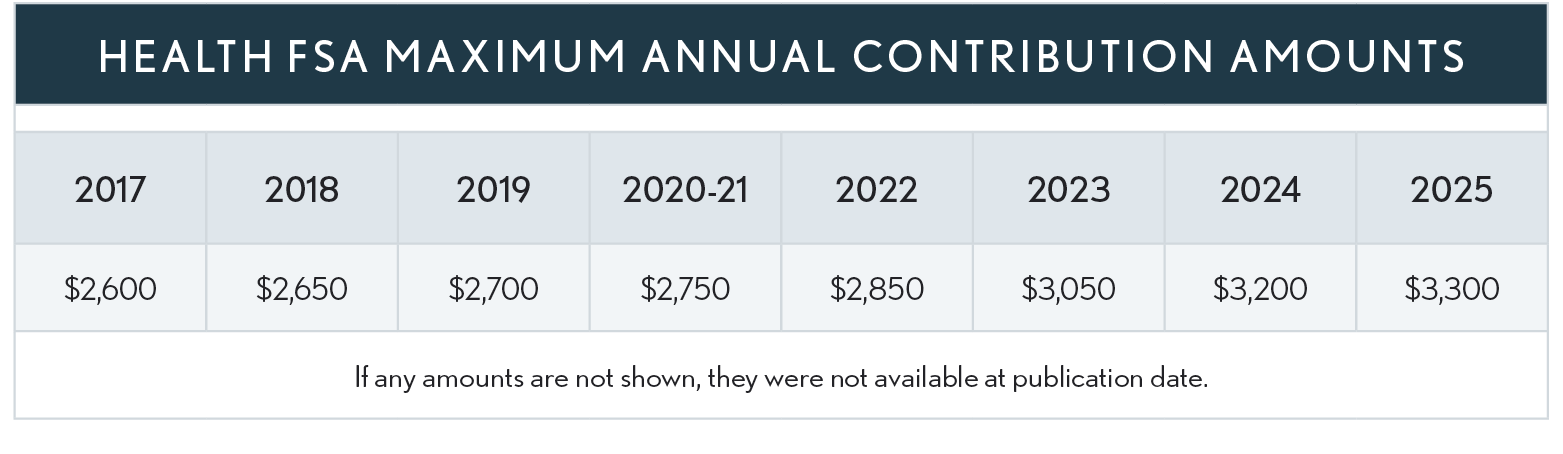

A Health Flexible Spending Account (FSA) is part of a qualified cafeteria plan offered by an employer, that allows employees to contribute pre-tax dollars annually to be used by the individual to pay medical expenses of the individual, their spouse and dependents during the year. The maximum contribution allowed for 2024 is $3,200. Amounts for other years are in the following table.

In the case of a married couple and each spouse has an FSA account with an employer, both can contribute the maximum.

A cafeteria plan can include one or more FSAs and is a benefit designed to reimburse employees for expenses incurred for certain qualified benefits, up to a maximum amount not substantially in excess of the salary reduction and employer flex-credits allocated for the benefit. The three types of FSAs are:

-

Dependent care assistance (See chapter 9.02),

-

Adoption assistance (See chapter 9.08) and

-

Medical care reimbursements (Health FSA covered in this chapter).

Years 2020 and 2021 Relief - As part of the COVID-19 emergency relief the government temporarily allowed flexibility for § 125 cafeteria plans to permit employees to make certain prospective mid-year election changes for employer-sponsored health coverage, health FSAs, and dependent care assistance programs during calendar year 2020 that the plan chose to permit (including an initial election to enroll in the plan). See Notice 2020-29 for details. Also see Notice 2021-15 regarding similar provisions for 2021 enacted in the Consolidated Appropriations Act, 2021.

Another relief provision allowed an employee who ceased to participate in an FSA during the plan years 2020 or 2021 to continue to receive reimbursements from unused benefits or contributions through the end of the plan year, including any extended grace period.

Child of Divorced Parents - A child who is a dependent of one parent of divorced parents shall be treated as a dependent of both parents for purposes of FSA allowed spending.

Common Features of an FSA

-

Funds can be used for deductibles, copays, medication, and other health care related out-of-pocket costs.

-

The employer owns the account — if an employee leaves the company, the employee can’t take the account with him.

-

All money deposited is untaxed.

-

For ease of use, most FSA accounts come with a debit card.

-

Employees can spend the money in the account before it’s fully funded.

Allowable Medical Expenses Include:

-

The diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body,

-

Prescription Drugs,

-

Medication available without a prescription (an over-the-counter medicine or drug) that is prescribed,

-

Insulin,

-

Transportation primarily for and essential to medical care,

-

Supplementary medical insurance for the aged,

-

Feminine menstrual products (added by the CARES Act and effective for years after 2019), and

-

Personal Protective Equipment (COVID) (Ann. 2021-7)

Long-Term Care Insurance and Services - A health FSA is not allowed to reimburse expenses for long-term care insurance premiums or for long-term care services. However, a cafeteria plan may offer an HSA as a qualified benefit, and HSA funds may be used to pay eligible long-term care insurance premiums on a qualified long-term care insurance contract or for qualified long-term care services. (Reg. 1.125-1(q)(3))

Transportation Costs Include:

-

Travel by the taxpayer to and from home to obtain medical care.

-

Traveling between home and a special school or program.

-

Cost of a relative traveling with the taxpayer if the taxpayer's circumstances or condition requires him to be accompanied.

-

A relative's trips to visit the taxpayer when ill where the visit is part of the treatment.

-

Travel to a medical conference on taxpayer's condition.

-

Travel to a therapeutic location.

-

Where travel includes the use of an automobile, the actual expenses may be used, or the standard medical mileage rate.

-

Although the costs of meals and lodging while away from home are generally not deductible medical expenses unless they are part of a hospital's (or similar institution's) fees, lodging costs incurred while away from home to get a physician's services in a hospital (or similar facility) on an out-patient basis are deductible, subject to a $50 per night per person limit.

-

Meals and lodging costs incurred en route between home and medical treatment and, in some cases, related to medical care obtained outside of a hospital (or similar facility) may also qualify.

-

Where a companion provides nursing-type services for a taxpayer while away from home, the meals and lodging costs of the companion may also be allowable medical costs.

No Double Dipping - Medical expenses reimbursed from the FSA cannot be claimed as a Schedule A medical itemized deduction.

Unused Amounts (Use It or Lose It) - Unused amounts at the plan’s year end are generally forfeited by the employee. However, a plan can have either:

-

A grace period of up to 2½ months after the end of the plan year in which to use up the unused amount or,

-

Allow up to 20% of the annual contribution limit, indexed for inflation) of unused amounts from the end of the plan year to be used to pay or reimburse qualified medical expenses in the following year.

Unused amounts in excess of the carryover amounts are forfeited (cannot be returned to the employee). The carryover amount does not reduce the maximum contribution amount allowed for the carryover year.

Extension for 2020 Unused Amounts - Notice 2020-29 allows an employer to amend its Sec 125 cafeteria plan(s) that have a grace period or provide for a carryover to permit employees to apply unused amounts remaining in a health FSA as of the end of a grace period ending in 2020 or a plan year ending in 2020 to pay or reimburse health expenses incurred through December 31, 2020. This relief applies to all health FSAs, including limited purpose health FSAs compatible with HSAs (see below). An individual who had unused amounts remaining at the end of a plan year or grace period ending in 2020 and who is allowed an extended period to incur expenses will not be eligible to contribute to an HSA during the extended period (except in the case of an HSA-compatible health FSA, including a health FSA that is amended to be HSA-compatible).

Carryover Period Extended for Plans Ending in 2020 and 2021 - The Consolidated Appropriations Act, 2021, § 214, expands the carryover period of any unused funds in health FSA plans for the 2020 year to plans ending in 2021, and for the 2021 year to plans ending in 2022. For plans that include a grace period, an extension of the grace period is permitted for plan years ending in 2020 and 2021 to 12 months after the end of such plan year for any unused benefits and contributions to health FSAs. See Notice 2021-15 for more information.

Types of Health FSAs

There are two types of health FSA plans:

-

General Purpose Health FSA – One that reimburses all qualified medical expenses without restriction that is classified as a “health plan that constitutes other coverage” and having such coverage would make the individual ineligible to make contributions to an HSA.

-

HSA-compatible Health FSA – One that is a limited-purpose health FSA, a post-deductible health FSA, or a combination of the two.

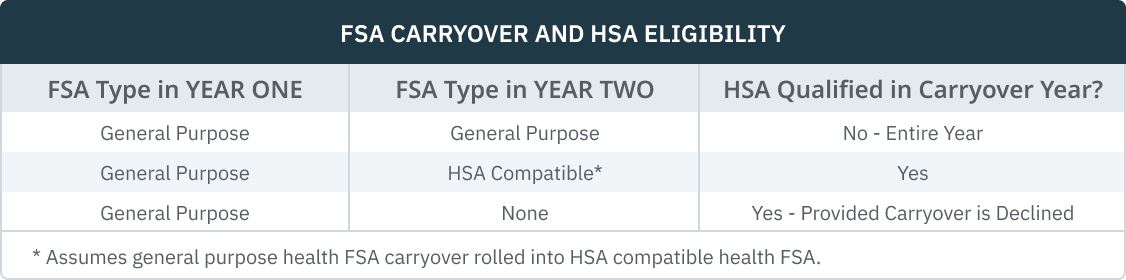

FSA Carryover and HSA Eligibility

The impact on HSAs of health FSA carryover from one year to the other is dealt with in Chief Counsel Advice 201413005. The following is a synopsis of the Chief Counsel’s advice where there is carryover from year 1 to year 2: