Program Requires Participation By Many Employers

California has created a retirement savings program, now called CalSavers, that was initially implemented over a 3-year period. The law creating this program requires California employers that don’t offer an employer-sponsored retirement plan to participate. Originally, the minimum number of employees that would trigger an employer’s participation was five, but a 2022 law change (see “Eligible Employer Redefined,” below) reduced the number to one.

The program is administered by a private-sector financial services firm (Ascensus College Savings Recordkeeping Services, LLC) and overseen by the California Secure Choice Retirement Savings Investment Board (the Board) chaired by the State Treasurer. Investments are managed by BNY Mellon Investment Adviser, Inc. [(CalSavers Sustainable Balanced Fund (Environmental, Social, Governance)] and State Street Global Advisors (all other funds).

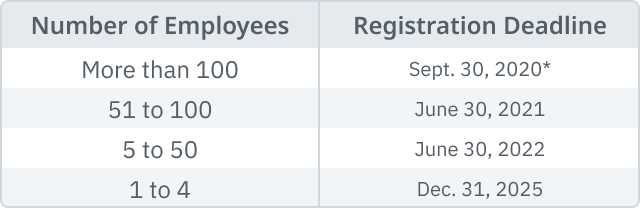

Registration of employers opened July 1, 2019, and the state encouraged eligible employers to join the program any time prior to their registration deadline. Employers can register on the CalSavers web site: https://www.calsavers.com even if they missed the registration deadline. The staggered deadlines for registering with the state, based on employer size, are:

*Originally scheduled to be June 30, 2020, the deadline was extended due to the COVID-19 emergency.

Eligible Employer Redefined

SB 1126, approved by the governor on August 26, 2022, expands the definition of which employers are required to participate to include a person or entity that has at least one eligible employee. California Government Code Sec.100000(d)(1) now defines an “eligible employer” for this purpose as a person or entity engaged in a business, industry, profession, trade, or other enterprise in California, whether or not for profit, excluding sole proprietorships, self-employed individuals, or other business entities that do not employ any individuals other than the owners of the business, the federal government, the state, any county, any municipal corporation, or any of the state’s units or instrumentalities that has at least one eligible employee and that satisfies the requirements to establish or participate in a payroll deposit retirement savings arrangement.

By December 31, 2025, employers with one or more eligible employees that do not provide a retirement savings program must have a payroll deposit savings arrangement to allow employee participation in the program. Based on the definition in the code, it would seem that household employers would be exempt from the requirement to participate in the CalSavers program.

Employer’s Responsibility

Employers have a limited role in the program, mainly to sign up employees, create and update a roster of eligible employees that is submitted to CalSavers, disseminate information about CalSavers, and submit participating employees' contributions that come from payroll deductions. Employers cannot make contributions to the program and there are no fees for employers. Since CalSavers is not sponsored by the employer, the employer is not responsible for the program or liable as a program sponsor. Employers are not permitted to endorse the program or encourage or advise employees on whether to participate, how much (if any) to contribute or provide investment help.

Employees’ Accounts

Each participating employee’s CalSavers account is an after-tax Roth IRA, and the employee is responsible for their investment choices, which initially include a money market fund, target retirement date funds, bond fund, global equity fund, and environmentally and socially conscious fund. If the employee hasn’t made an investment selection, the first $1,000 contribution will go into the money market fund and thereafter contributions will be put into a Target Retirement Date Fund. Investments in CalSavers are not guaranteed or insured by the Board, the State of California, the Federal Deposit Insurance Corporation (FDIC), or any other organization.

Eligible Participants and Contribution Rates

To participate the employee, whether full-time or part-time, must be at least 18 years old and have either an SSN or an ITIN. (A sole proprietor or partner in a partnership that is an eligible employer also qualifies to participate.) The default contribution rate for each employee is 5% of gross pay but employees can opt out of the program or change their contribution rate at any time. The minimum contribution rate is 1% and the maximum is 100% of available compensation up to the federal annual IRA contribution limits. An employee who doesn’t opt out will be enrolled automatically after 30 days. The contribution percentage automatically increases by 1% each year starting January 1, 2020, up to a maximum contribution rate of 8%, but the employee can choose to opt out of automatic escalation.

Employees can join the program on their own if they do not have access to a retirement savings plan through their employer. Those who choose to self-enroll in CalSavers separate from an employer arrangement need to link their bank account to their CalSavers account through the CalSavers website.

Participating employees should be mindful of the AGI limitations for contributing to Roth IRAs and the annual IRA contribution limitations to avoid over-contributions that could result in tax and penalty liabilities. According to the CalSavers web site, an employee who earns more than the Roth IRA income limits set by the federal government may need to opt out of CalSavers or recharacterize to a Traditional IRA. CalSavers offers savers the option to recharacterize their contributions to a Traditional IRA. This action can be completed online.

Potential Employer Penalty

AB 102, signed by the governor June 29, 2020, added Government Code Sec 100033(b)(2) that allows the CalSavers Retirement Savings Board (CRSB) to penalize an eligible employer that, without good cause, fails to allow its eligible employees to participate in the CalSavers Retirement Savings Program. The penalty is $250 per eligible employee and an additional $500 per eligible employee if noncompliance continues. The FTB is tasked with issuing the first notice of penalty after being informed of the employer’s noncompliance by the CRSB; employers may appeal the penalty in writing to the FTB.

Administrative Fees

A fee to cover the costs of the administration of the program and operating expenses is collected in the form of an annual asset-based fee of 0.325% to 0.49%, , depending on the employee’s investment choice, plus a fixed fee of $4.50 per quarter. This means the employee will pay between 33 cents and 49 cents per year for every $100 in their account, based on their investment choice, plus a quarterly fixed fee of $4.50. The employer does not receive any of the fee.