Penalties for Federal Tax

The following is a listing of the penalties that are most commonly assessed by the IRS. The codes which the IRS uses on its penalty notices are also included.

Filing and Paying Late (Code 01)

These penalties are assessed because a taxpayer did not timely file and did not pay the tax owed. The combined penalty is 5% of the unpaid tax for each month or part of a month the return is late, but not for more than 5 months. The late filing penalty is reduced by the late payment penalty. Thus, the 5% includes a 4 1/2% penalty for filing late and a 1/2% penalty for paying late. (IRC 6651).

The 25% combined maximum penalty includes 22 1/2% for filing late and 2 1/2% for paying late. The 1/2 % penalty for paying late is not limited to 5 months. This penalty will continue to increase to a maximum of 25% until the taxpayer pays the tax in full. The maximum 25% penalty for paying late is in addition to the maximum 22 1/2% late filing penalty for a total penalty of 47 1/2%.

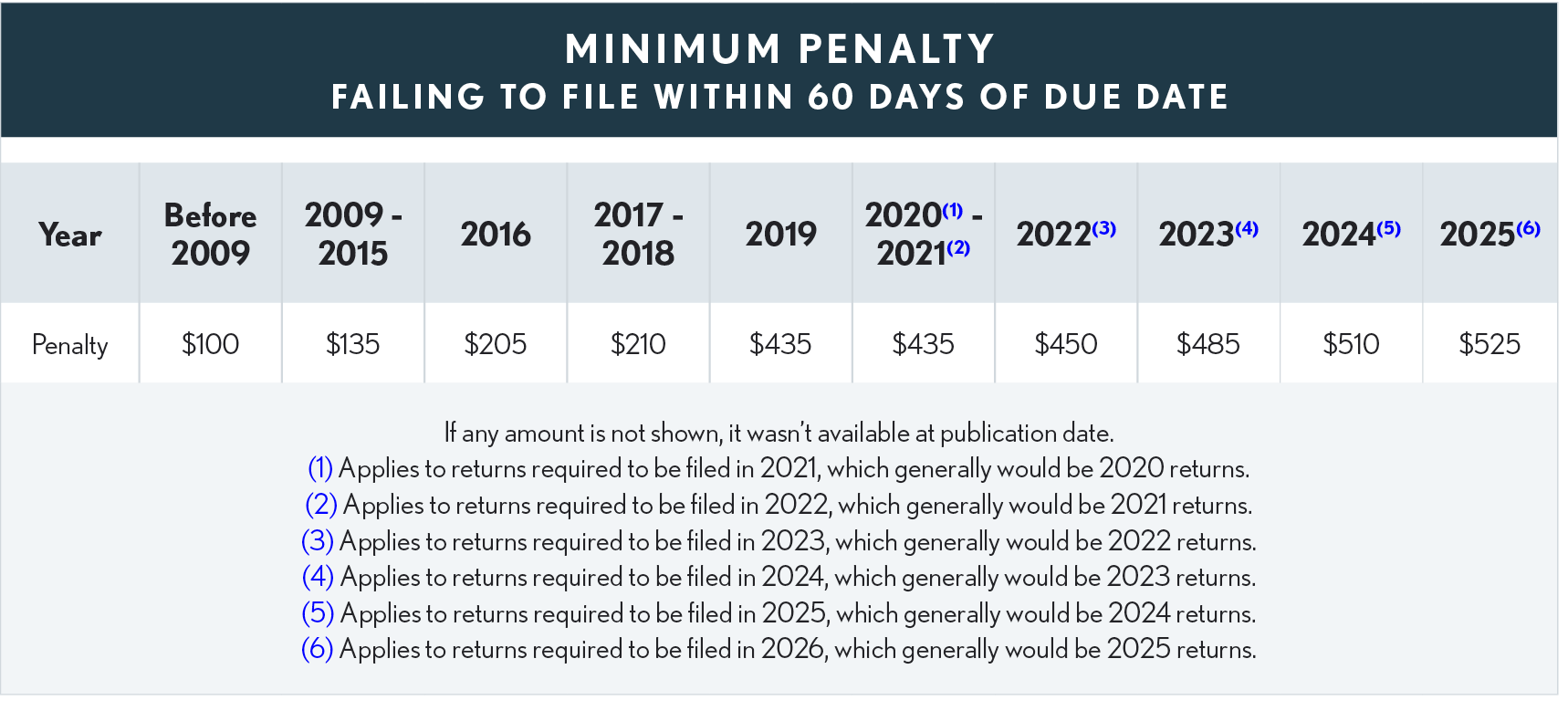

If a taxpayer didn't file a return within 60 days of the due date, the minimum penalty is the lesser of 100% of the tax due or $485 for returns required to be filed in 2024 (SECURE Act; IRC Sec 6651(a)). Current and historical penalties are shown in the table below.

Extensions - Extension of Time to File Not Found

IRM 20.1.2.2.3.1.1 (03-19-2019) – Provides guidance to IRS employees when a taxpayer claims to have filed an extension, but the extension has not been posted on the IRS system. It requires the IRS agent to check if the extension filed was erroneously posted to another account. It also requires the IRS to examine the facts of each case and apply the more likely than not criteria. The following is an excerpt from the Revenue Manual:

. . . if all the known facts would lead a reasonable person to presume that it is more likely than not, that a valid, and timely, extension request was submitted, then the more likely than not criteria has been met. Examples would include a certified mail receipt along with a copy of the extension; or a list of extensions filed by a tax professional where most extensions on the list have been received and posted; or a payment posted to the account that was mailed with the extension request. (This list is not all-inclusive.)

A history of approved extensions alone, a mere statement that an extension request was filed, or even a copy of the extension request that was allegedly filed, are not in and of themselves evidence of filing an extension for the current year. However, collectively with other facts, such as the reason the taxpayer would have had for filing an extension, the earlier mentioned facts could be sufficient to meet the more likely than not criteria. Additionally, Facts can be used collectively to show that it was reasonable for the taxpayer to believe that an extension had been requested and approved. For example, a list of extensions allegedly filed by a tax professional, where most extensions on the list have not been received and processed, still may be used to show that it was reasonable for the taxpayer to believe that an extension of time to file had been requested and approved.

Extension Precautions: Many practitioners take filing extensions far too lightly and are unaware of, or ignore, the nuances of properly completing an extension and the potential penalties. Properly and timely filing the Form 4868 extends the individual income tax return filing due date for a calendar-year filer to October 15 (or the next business day if October 15 falls on a weekend or holiday) and avoids the 5% per month (or part of a month) failure-to-file penalty.

Properly Estimate the Tax Liability – The 4868 instructions clearly indicate that to have a valid extension, a taxpayer must:

-

Properly estimate their tax liability using the information available to them, and

-

Enter their total tax liability on line 4 of the 4868 and

-

File the extension by the regular due date for their return.

This requirement was reinforced in Tax Court (Laidlaw v. Commissioner) where the court determined the extension was invalid because the taxpayer (through their tax preparer) did not make a bona fide and reasonable estimate of their tax liability or attempt to secure the information necessary to complete a valid estimate. They had merely entered a zero for the estimated tax liability without making a proper estimate of the liability.

Underpayment of Estimated Tax (Code 02)

If a taxpayer owes tax of $1000 or more for the tax year, the taxpayer must prepay the tax by having tax withheld or by making estimated tax payments. Failure to do so will result in the taxpayer being subject to the current published interest rates for underpayment of estimated taxes. See chapter 10.03 on estimated taxes and safe harbor rules. (IRC Sections 6654, 6621)

Dishonored Check Payment (Code 04)

A penalty is charged if a taxpayer's payment is dishonored and returned from a financial institution. The penalty is the greater of $25 or 2% of the payment amount. For checks of less than $1,250, the penalty is the lesser of $25 or the amount of the check. (IRC Section 6657)

Fraud (Code 05)

This penalty is 75% of the tax unpaid due to fraud. (IRC Section 6663)

Negligence (Code 06)

This “accuracy-related” penalty is 20% of the tax underpayment that is due to negligence or tax valuation misstatements (IRC Section 6662(a)). Substantial understatement is the greater of 10% (5% if the Sec 199A deduction is claimed) of the tax shown on the return or $5,000. (IRC Section 6662(d)(1)) A 40% accuracyrelated penalty is imposed for underpayment of tax that is attributable to an undisclosed foreign financial asset understatement (IRC Sec. 6662(j)).

Paying Late (Code 07)

The penalty is 1/2% of the unpaid tax for each month or part of a month the tax is unpaid. If the IRS issues a Notice of Intent to Levy and the taxpayer doesn't pay the balance within 10 days, the penalty increases to 1% per month. The penalty can't be more than 25% of the tax paid late. The late payment penalty is reduced to 1/4% per month for those paying in installments. (IRC Section 6651)

Missing ID Number (Code 08)

This penalty is $50 for each missing number. This penalty is charged when a taxpayer doesn't provide a social security number (SSN) for themself, a dependent, or another person or doesn't provide his/her SSN to another person when required. The penalty can't exceed $100,000 in any calendar year. (IRC Section 6723)

Penalty on Tips (Code 27)

This penalty is charged if a taxpayer didn't report tips to his/her employer. It equals 50% of the social security tax on the unreported tips. (IRC Section 6652(b))

“Excessive” Claim Penalty

Is equal to 20% of the excessive amount. (Code Sec. 6676(a), as amended by the PATH Act of 2015) The “excessive amount” is the amount by which the amount of a person's claim for refund or credit for any tax year exceeds the amount of the claim allowable under the Code for that tax year. (Code Sec. 6676(b)) The penalty doesn't apply if it is shown that the claim for the excessive amount is made with reasonable cause. The penalty also does not apply if any portion of the excessive amount or credit is subject to an accuracy related penalty imposed under Code Sec. 6662 or Code Sec. 6662A or under the Code Sec. 6663 fraud penalty. (Code Sec. 6676(c))

Frivolous Return

In addition to any other penalties, the law imposes a penalty of $5,000 for filing a frivolous return. A frivolous return is one that does not contain information needed to figure the correct tax or shows a substantially incorrect tax because the taxpayer takes a frivolous position or desire to delay or interfere with the tax laws. This includes altering or striking out the preprinted language above the space where the taxpayer signs. For a list of positions identified as frivolous, see Notice 2010-33, I.R.B. 2010-17, April 7, 2010, which modifies and supersedes Notice 200814, 2008-4, IRB 310, both of which are available at: www.irs.gov/irb. (Code Sec 6702) Under limited circumstances the IRS may reduce the penalty from $5,000 to $500; see Rev. Proc. 2012-43, 2012-49 IRB 643 for details.

Minimum Penalty for Failure to Report on Foreign Trust

For notices and returns required to be filed after Dec. 31, 2009, the initial penalty for failing to report under Code Sec. 6048 is the greater of $10,000 or 35% of the gross reportable amount (5% for U.S. persons treated as owners of the trust). (Code Sec. 6677(a)) Thus, an initial penalty of $10,000 is imposed even where IRS has insufficient information to determine the gross reportable amount. The additional $10,000 penalty for every additional 30 days of delinquency continues to apply. The penalty applies if the required information or return is not filed by the due date, does not include all required information or includes incorrect information. Form 3520-A is used to report a foreign trust; see page 1.13.17.

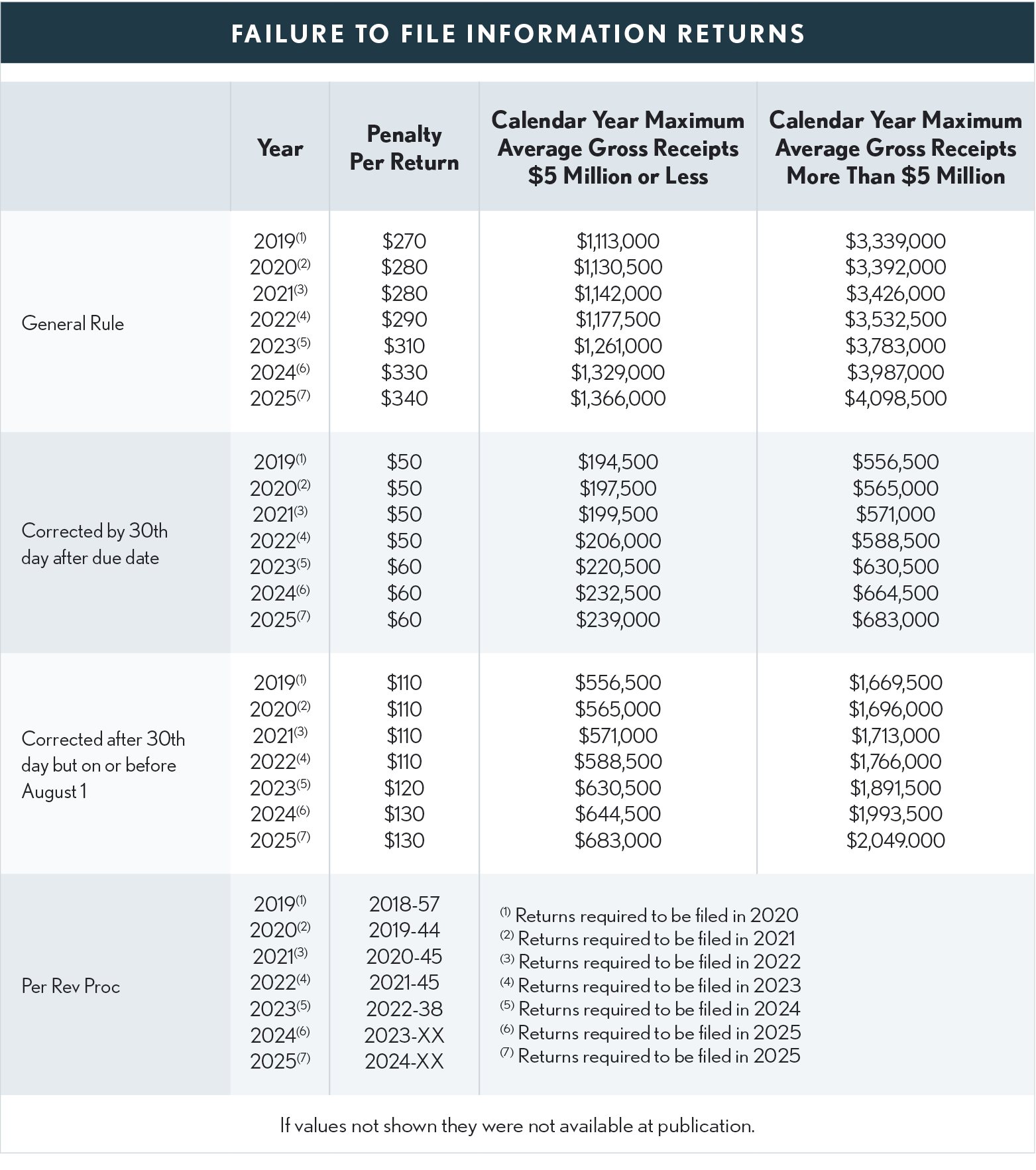

Failure to File Information Returns

A payer who, without reasonable cause, fails to timely file a required information return in the required manner, or fails to include all of the information required to be shown on the return, or includes incorrect information, is subject to a penalty. For a correct information return filed late, but on or before 30 days after the required filing date, the penalty amounts are reduced; returns filed after the 30th day after the due date but on or before August 1 have a lesser reduced penalty. For tax years beginning in 2015, the penalty amounts are inflation-adjusted (see tables below covering years starting with 2019). Income for the maximum penalty amount is determined by averaging the gross annual receipts of the most recent three tax years. If failure to file a correct information return is due to intentional disregard of the filing requirement or the correct information reporting requirement, there is no limit to the penalty that IRS can assess, and the per return penalty is roughly twice the general rule penalty or, if greater, 5% or 10% (depending on the code section that was violated) of the aggregate amount of items required to be reported correctly. (Code Sec 6721)

De Minimis Failures

An otherwise correctly filed information return that has one or more incorrect dollar amounts does not need to be corrected in some cases. It is treated as having been filed or provided with all correct required information, if no single incorrect dollar amount differs from the correct amount by more than $100; and no single amount reported for tax withheld on any information return differs from the correct amount by more than $25. (Code Sec. 6721(c)(3)) However, if the person receiving the payee statement elects out of the exception, and elects to receive a corrected payee statement, this safe-harbor rule won’t apply.

Restitution Collection

The IRS is allowed to assess and collect the amount of restitution under an order made pursuant to title 18 USC § 3556 for failure to pay any tax imposed under the Code, in the same manner as if the restitution amount were the tax itself (Code Sec. 6201(a)(4)(A)). In other words, IRS can assess and collect restitution owed by defendants in criminal tax cases as if it were a tax. An assessment of such a court-ordered restitution amount won't be made before all appeals of the order are concluded and the right to make all those appeals has expired. (Code Sec. 6201(a)(4)(B))

W-4 Falsification

A penalty of $500 may be assessed if Form W-4 is completed in such a way as to reduce the withholding and there is no reasonable basis for doing so. There is also a $1,000 criminal penalty or one year of imprisonment, or both, if convicted of willfully providing fraudulent information in order to reduce withholding. (Code Section 6682)

Overstatement of Non-Deductible IRA Contributions

$100 for each overstatement unless due to reasonable cause.

Failure to file Form 8606 – Non-Deductible IRA

$50 unless due to reasonable cause. (Form 8606 Instructions)

Failure to Provide TIN to Payer of Alimony

$50 (IRS Pub 504).

"Seriously Delinquent" Tax Debt Warranting Revocation or Denial of Passport

The State Department can take action to revoke or limit the passport of an individual with a "seriously delinquent tax debt," as defined in Code Sec. 7345, of more than $62,000 in 2024, $59,000 in 2023, $55,000 in 2022, $54,000 in 2021.