Preparer Due Diligence Requirement

A paid preparer is subject to diligence requirements in determining a client’s eligibility for the:

-

Head of Household filing status

-

Earned Income Credit (EIC)

-

American Opportunity Tax Credit (AOTC)

-

Child Tax Credit (including the Additional Child Tax Credit (ACTC) and, Credit for Other Dependents (ODC))

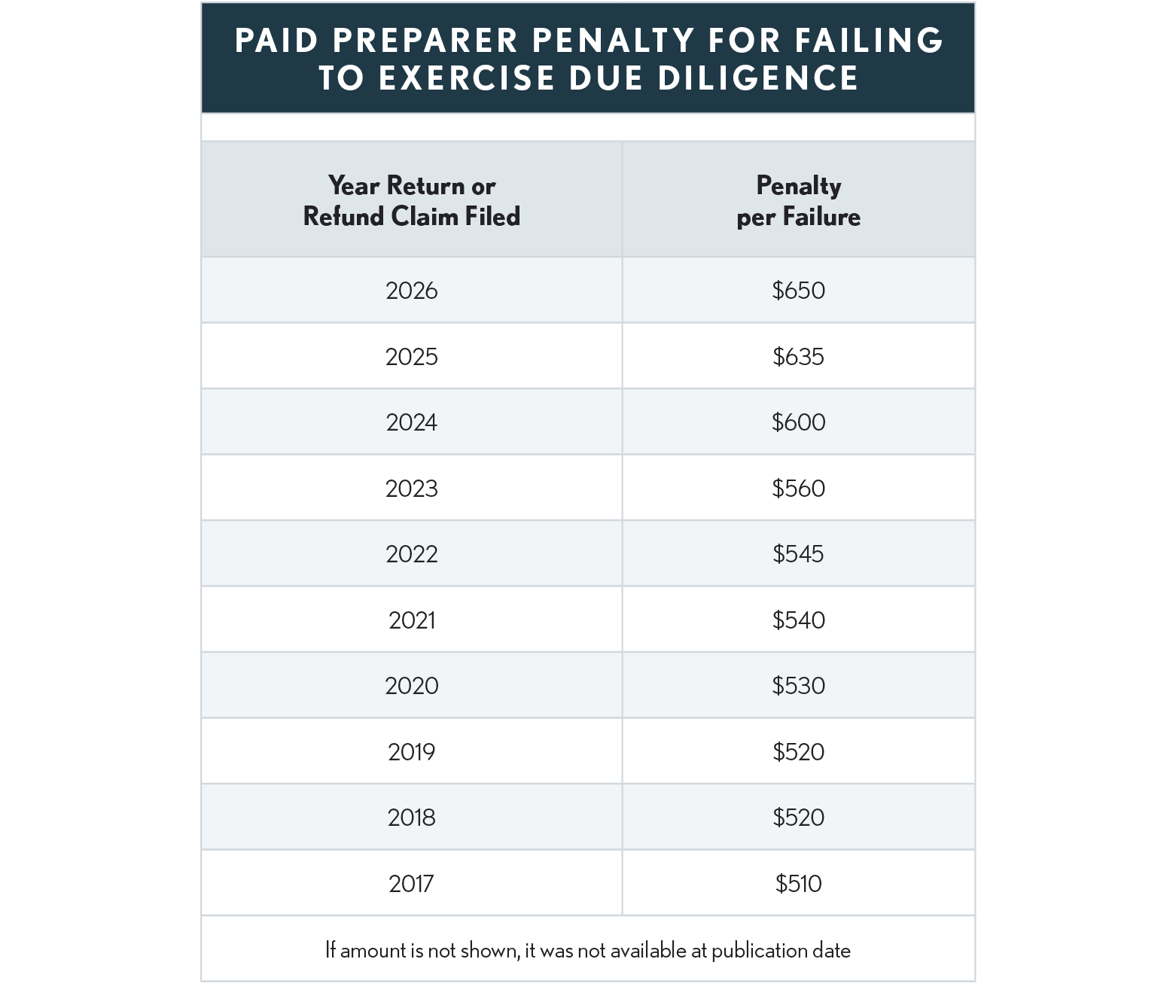

The penalty amounts for failing to exercise due diligence with respect to any of these tax credits or, starting with 2018 returns, head of household filing status are shown in the table below. The penalty applies for each failure, so for example, if a preparer failed the due diligence requirement for claiming the head of household status and the EIC on a client’s 2022 return filed in 2023, the preparer’s penalty would be $1,120 (2 x $560). IRS Form 8867, Paid Preparer’s Due Diligence Checklist, is required whenever a return includes the head of household status, the earned income credit, American Opportunity credit, and/or child tax credit (including the additional child tax credit and credit for other dependents). See chapter 9.03 for additional information about the due diligence requirements.