Filling Out Forms 656/433-A/433-B

For joint filers, if only one spouse has tax liability, but both have income, only the spouse responsible for the tax debt needs to prepare the forms. In this case, the responsible spouse should include only his/her assets and liabilities when filling out the forms. Important: The income and expenses of the whole household are required, including income of spouse, domestic partner, significant other, children and others that may contribute to the household.

In community property states, the forms are required from both spouses.

When completing forms, remember that offers based on doubt as to collectability or effective tax administration must include all unpaid tax liabilities and periods for which the taxpayer is liable. For instance, if a taxpayer submits an offer to compromise income tax liabilities, but also owes business liabilities for his/her sole proprietorship, both the income tax and business liabilities must be included in the taxpayer’s offer. On the other hand, doubt as to liability offers should only include the tax year in question, and other tax periods that the taxpayer owes on shouldn’t be included in the offer (IRM 5.8.1.9 (5-25-2023)).

Coverage of Offers

A compromise is effective for a taxpayer’s assessed liability for tax, penalties and interest for the years or periods covered by the offer. When a compromise is accepted, all questions of tax liability for the years covered by the agreement are settled. Neither the taxpayer nor the IRS can reopen a compromised tax year unless there was falsification of documents or some other concealment or mutual mistake in the case.

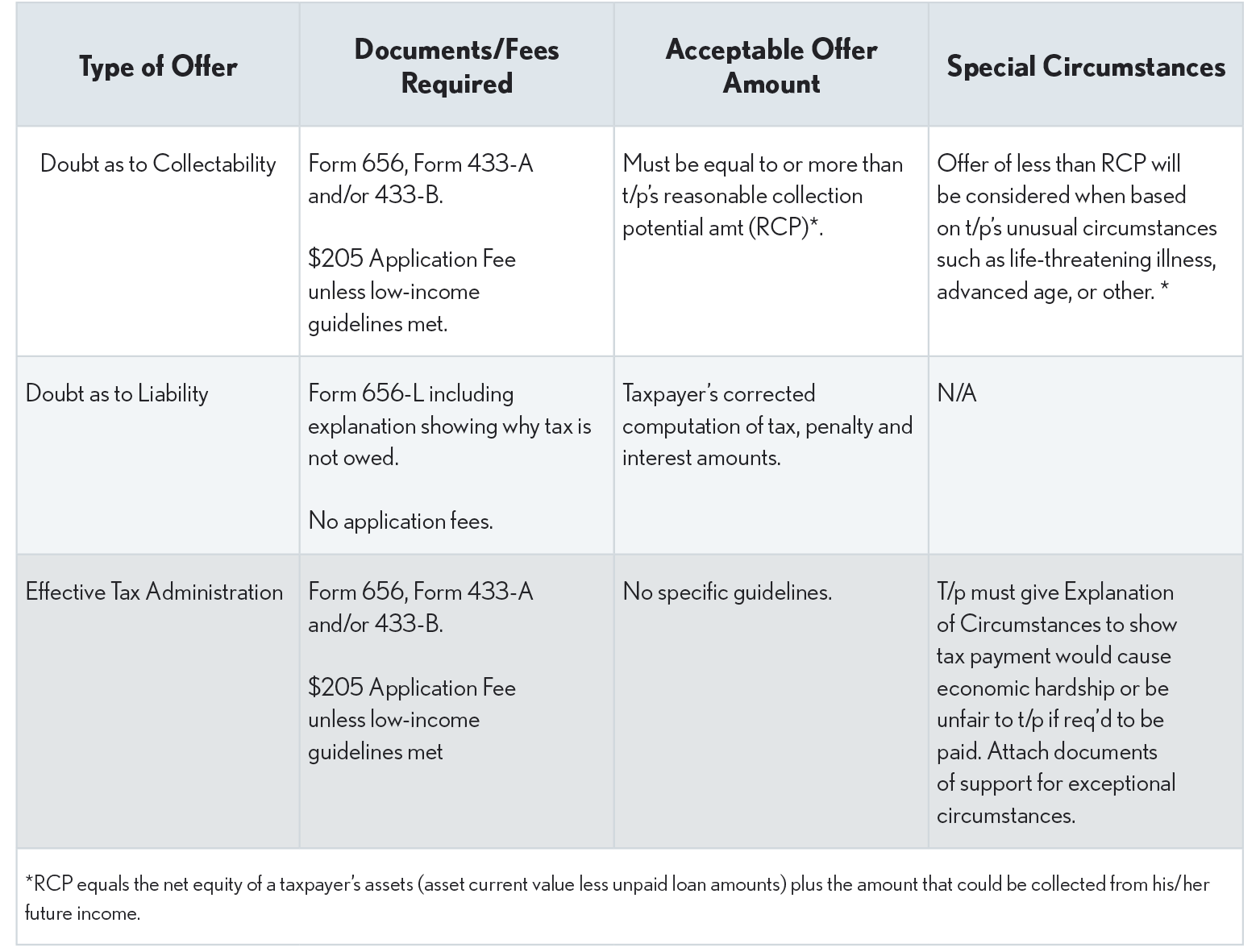

The following table gives an overview of acceptable amounts and documents needed for OICs:

OIC Definitions

Useful in preparing offers based on “doubt as to collectability” or “effective tax administration”:

Current Value of Assets - Is the amount a person could reasonably expect to get from the sale of an asset at a given point in time. In filling out OIC forms, determine current value of various assets by checking, for example, with realtors, used car dealers, newspaper advertisements, etc.

With the ups and downs of the housing market, the IRS recognizes that the real estate valuations used to assess ability to pay may not be accurate. So, in instances where the accuracy of local real estate valuations is in question or other unusual hardships exist, the IRS will do a second review of the information to determine if accepting an offer is appropriate. (IR-2009-2, Jan. 6, 2009)

California RDP’s Assets Considered in OIC - The IRS Chief Counsel’s Office has determined that in considering the reasonable collection potential of a California taxpayer who files an offer in compromise (OIC), the IRS may consider the community property assets owned by the taxpayer’s registered domestic partner. This is so even though the RDPs are not allowed to file a joint federal return.

In community property states, of which California is one, the IRS’ position is that the assets of both owners of community property (the owner submitting the offer and the non-offering owner) should be considered in the offer.

The Internal Revenue Manual (Section 25.18.4.4 (06-05-2017)) provides that if under applicable state law, all or part of the non-offering owner's share of community property and community property income would be available to satisfy the tax liability at issue, these items should be considered in the offer in compromise. Since California registered domestic partners share an equal interest and liability in community property in the State of California, the Chief Counsel concluded that the IRS can consider the assets of the taxpayer’s RDP in determining whether to accept the taxpayer’s OIC. (CCA 201021049)

Future Income - Is the amount the IRS figures they could collect by subtracting a taxpayer’s necessary living expenses from his/her monthly income over a set period of time.

Necessary Expenses - Are payments a person makes to support the health and welfare of himself/herself and his/her family. Necessary expenses can also be those for items used in the production of income for the taxpayer.

IRS to be More Flexible with OICs from Unemployed Taxpayers - The IRS announced that its employees will be permitted to consider a taxpayer's current income and potential for future income when negotiating an offer in compromise. Normally, the standard practice is to judge an offer amount on a taxpayer's earnings in prior years. This new step provides greater flexibility when considering offers in compromise from the unemployed.

The IRS may also require that a taxpayer entering into such an offer in compromise agree to pay more if the taxpayer's financial situation improves significantly. (IR-2010-29, 3/9/2010) Note: Commenting on this change, the National Taxpayer Advocate raised concerns that “procedures do not clearly instruct IRS employees to apply flexibility and good judgment when calculating future income.” (Taxpayer Advocate Service, Fiscal Year 2011 Objectives report to Congress, page 22)

Living Expenses Generally NOT Allowed By IRS As “Necessary Expenses” - Include school (including college) tuition, charitable gifts, voluntary retirement contributions, cable TV charges and the like. Such expenses can only be claimed as necessary when the taxpayer shows they are vital to the health and welfare of his/her family or needed for the production of income. The IRS in IR-2012-53 has revised their necessary expenses to include payments on federally guaranteed student loans for post-secondary education.

Quick Sale Value (QSV) - Is the amount a person can reasonably expect from the sale of an asset if it had to be sold in 90 days or less.

Realizable Value - Is QSV less any amount owed to a secured creditor on the asset.