Notes on the Allocation Worksheet

Important Reminder

Community property laws aren’t considered to determine whether an item belongs to the innocent or non-innocent spouse.

LINE 1, Column (a)

-

Allocate income and deductions to compute understatement of tax in the same manner that would have been used if separate returns had been filed.

-

Generally, enter items allocable to the innocent spouse in column (a).

-

Allocate wages to the spouse who performed the underlying services., Business income should be allocated to the spouse who owned the business., This rule also applies to capital gains., If spouses own property together, allocate according to each one’s ownership interest.

-

To allocate items subject to different tax rates, first separate erroneous items into categories according to tax rate.Then use a separate worksheet for each category.

EXAMPLE - Allocating Items Subject to Differing Tax Rates: Dan and Holly filed a joint tax return in 2020 but were divorced in 2021. In 2022, the IRS audited the 2020 return and found that the couple owed $4,700 additional income tax. Of that amount, $1,500 was tax on an unreported net capital gain of $10,000 (15% tax rate). The remaining $3,200 was assessed due to unreported interest and nonqualified dividend income of $10,000 (32% tax rate). This is the breakdown of the erroneous items attributable to each spouse.

-

Holly decides to ask for relief by separation of liability. She will complete 2 worksheets, one for each different tax rate. On the first worksheet (for 15% rate items) on line 1, she will enter $6,000 in column (a); $10,000 on line 2; .60 on line 3, column (a); and $1,500 on line 4. The remainder of the worksheet will be completed as appropriate.

-

On the second worksheet (for 32% rate items) on line 1, column (a), she will enter $3,000; $10,000 on line 2; .30 on line 3 column (a); and $3,200 on line 4.The remainder of the worksheet will be completed as appropriate.

5. If there is income subject to special limits on separate returns (like social security), figure the income on a joint return basis and allocate it between the spouses.

EXAMPLE - Allocating Income with Special Separate Return Limits: Belle and Riordon filed their 2022 return jointly. Riordon received social security income in that year, but it was not taxable because the couple’s total income was under the base amount of $32,000 for joint filers. Eventually, the couple received an IRS notice advising them that they hadn’t reported certain interest income. The notice recomputed their 2022 tax based on this increased income and showed that half of Riordon’s social security was taxable because total income was over the $32,000 base amount. Had Riordon filed a separate return for 2022, 85% of his social security would have been taxable. When figuring his separation of liability, Riordon allocates only half of the social security. This is true even though 85% would have been taxable had he and Belle filed separately.

-

LINE 1, Column (b)

Income and deductions allocated jointly to the spouses need to be

entered in Column (b), including items of the non-innocent spouse which created

a tax benefit for the innocent spouse and erroneous items the innocent spouse

knew about.

EXAMPLE - Tax Benefit Items Allocated to Innocent Spouse: Terry’s joint return shows his wages of $50,000 and $15,000 gross self-employment income allocated to his spouse. An audit disallowed $20,000 in expenses of the self-employed spouse. Only $15,000 of the disallowed expense offset the spouse’s income. The remaining $5,000 must be allocated to Terry because the amount offset his income.

-

LINE 5

Enter the part of the understatement of tax that came from an adjustment to a credit. In addition, enter adjustments to a child’s tax that the taxpayer chose to report on a joint return and any tax other than income tax. Examples of the latter could be:

-

Alternative minimum tax

-

Net investment income tax

-

Household employment taxes

-

Recapture of investment, low-income housing, qualified electric vehicle, Indian employment, or new markets credits

-

Recapture of federal mortgage subsidy

-

Self-employment tax

-

Social security and Medicare tax on unreported tips

-

Premature retirement account distribution penalties

-

Additional taxes on Coverdell education savings accounts

-

Tax on excess contributions to IRAs, education savings accounts, or Archer MSAs

-

Tax on golden parachute payments

-

Tax on accumulation distribution of trusts, and

-

Uncollected social security and Medicare or RRTA tax on tips or group-term life insurance.

LINE 8, Column (a)

Generally, allocate credits and other taxes in the same manner as if the spouses had filed separate returns.

EXAMPLE - Allocating Credits, Taxes, Etc., to the Innocent Spouse: Alice reported $800 in self-employment tax on her return. In an audit, the IRS concluded that she owed $1,200 in self-employment tax. Since all this tax applies to Alice, she would enter the increase in self-employment tax of $400 ($1,200 less $800) in column (a) of the worksheet.

-

If a child’s tax liability is reported on the joint return (using Form 8814), include the tax attributable to the child’s income in Column (a) only if the child is the innocent spouse’s and hasn’t been legally adopted by the non-innocent spouse.

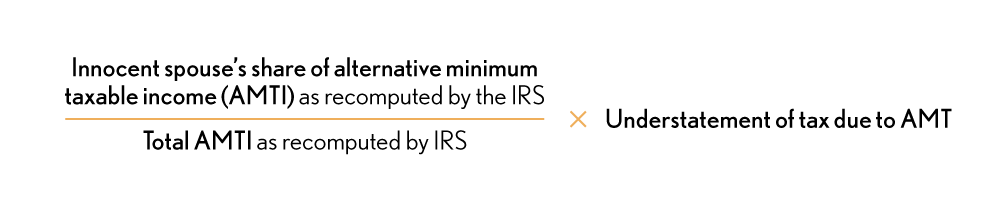

In addition, enter the innocent spouse’s share of alternative minimum tax in Column (a) using the following formula to figure it:

Credits that wouldn’t be allowed had the innocent spouse filed separately should be figured as on a joint return and then allocated between the spouses. Examples of this might be child and dependent care credits, adoption or education credits and the EIC.

EXAMPLE - Allocating Credits between Spouses: Fred and Alta claimed an $860 childcare credit on their joint tax return. However, $360 of the credit was disallowed in audit. Had the couple filed separate tax returns, none of the credit would have been allowed. However, they are entitled to $500 for purposes of figuring separation of tax liability. The amount allocated between Fred and Alta on the Worksheet is the $360 disallowed portion

-

Line 8, Column (b)

Credits and other taxes allocated jointly to the spouses need to be entered in Column (b) on this line. They should not be entered in Column (a). The following are examples of items to be listed in Column (b):

-

Credits allocable to the non-innocent spouse that created a tax benefit for the innocent spouse;

-

Erroneous items the innocent spouse was aware of;

-

A child’s tax liability reported by filing Form 8814., However, if one spouse is the child’s stepparent, enter this liability in Column (b) only if the stepparent legally adopted the child;

-

Household employment taxes.