Household Employees

Warning

It is illegal to knowingly hire or to continue to employ an alien who is not legally eligible to work in the U.S. When hiring a household employee who works on a regular basis, Form I-9, Employment Eligibility Verification, must be completed by the employer and employee. The employer must examine documents presented by the employee that establish the employee’s identity and employment eligibility. The employer retains the completed Form I-9; it is not submitted to IRS. Form I-9 is not an IRS form; it can be downloaded from the U.S. Customs and Immigration Services web site.

Employee Retention Credit Doesn’t Apply to Household Employers

A credit created in the CARES Act gave certain employers a refundable credit for 2020 and 2021 for retaining employees in their business operations during the COVID-19 pandemic. However, this credit did NOT apply to household employers because being a household employer is not a trade or business.

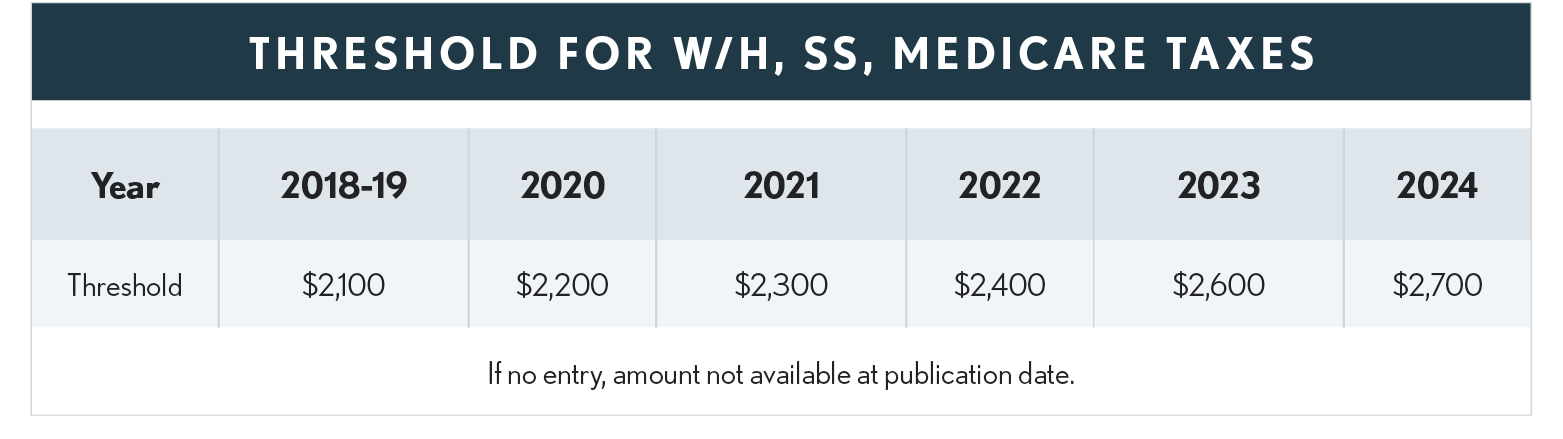

Social Security and Medicare Taxes (FICA)

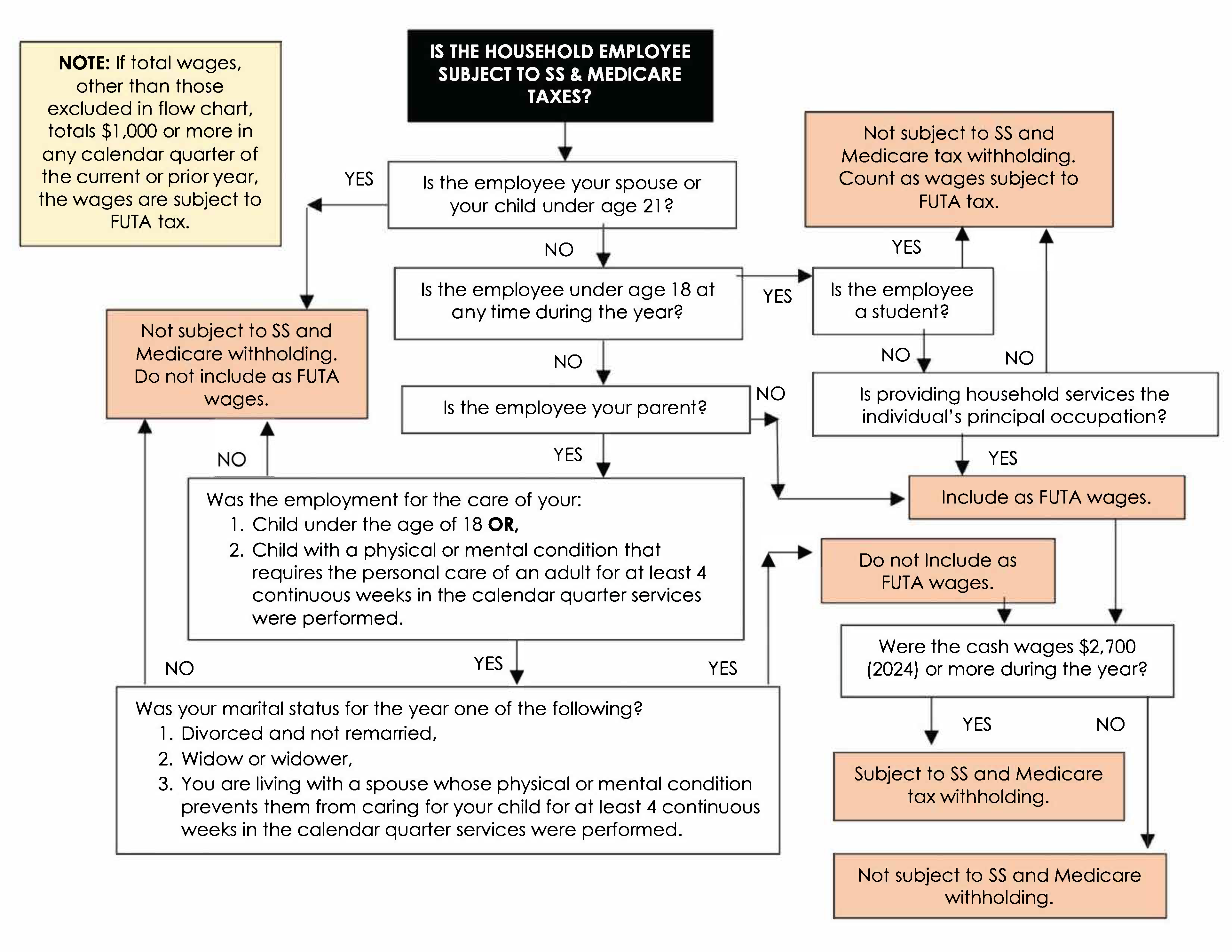

A household employer, except as noted in the the flow chart that follows, must withhold both social security and Medicare taxes from a household employee’s cash wages if they equal or exceed the threshold for the year – see table above.

The employer must match from his/her own funds, the FICA amounts withheld from the employee’s wages.

The value of food, lodging, clothing or other noncash items given to household employees isn’t subject to FICA taxes. However, cash given in place of these items is subject to such taxes.

Income Tax Withholding

A household employer doesn’t have to withhold income taxes on wages paid to a household employee, but if the employee requests such withholding, the employer can agree to it. If income taxes are to be withheld, the employer can have the employee complete Form W-4 and base the withholding amount on the data the employee provides. IRS Publication 15 (sometimes referred to as Circular E) provides the federal income tax and FICA withholding tables.

Wages Subject to Withholding

This includes salary, vacation pay, bonuses, clothing and other noncash items, meals and lodging. Meals are not subject to income tax withholding if they are furnished for the employer’s convenience and on the employer’s premises. The same goes for lodging if one additional requirement applies--that the employee lives on the employer’s premises. Reimbursement for (a) transit passes, up to $315 per month for 2024 used by the employee to commute to the employer’s premises, or (b) commuting-related parking, up to $315 per month for 2024 are not counted as wages.

In lieu of withholding the employee’s share of FICA taxes from the employee’s wages, some employers prefer to pay the employee’s share themselves. In that case, the FICA taxes paid on behalf of the employee are treated as additional wages for income tax purposes.

Federal Unemployment Tax (FUTA)

A household employer who pays more than $1,000 in cash wages to household employees in any calendar quarter of either the current or the prior year, is liable for FUTA tax. There is a credit against this tax for payments made to a state unemployment fund.

Employer Identification Number

A household employer is required to have an employer identification number (not the same as a Social Security number). It is used on any employment tax forms required to be filed. Use Form SS-4, Application for Employer Identification Number, to request an EIN (or one can be obtained by completing an on-line application at the IRS’ web site; enter “EIN” in the search box). A household employer who has had an EIN as the sole proprietor of a business should use that number.

Reporting and Paying Employment Taxes for Household Workers

Household employers will generally report and pay employment taxes on household employee wages as part of their Form 1040 filing. This includes social security, Medicare, and income tax withholding plus FUTA taxes. Schedule H is used for this purpose and is attached to Form 1040 when paying the taxes. To avoid an underpayment of estimated tax penalty, the household employer should be sure that his or her own income tax withholding or estimated tax payments is sufficient to cover the Schedule H taxes as well as regular income tax.

If the employer runs a sole proprietorship with employees, the social security, Medicare, and income tax withholding for any household employees may be included on Form 941, Employer’s Quarterly Federal Tax Return, filed for the business. In that event, FUTA tax for the household employees is included on the business’ Form 940 or 940-EZ, Employer’s Annual Federal Unemployment Tax Return. Some employers may be required to file Form 944, Employer’s ANNUAL Federal Tax Return, instead of Form 941. Caution: when preparing the proprietor’s Schedule C, care should be taken to make sure that the wages and related payroll taxes of the household employee aren’t included as a business expense on the Schedule C.

Form W-2 and Form W-3

Household employers must provide W-2s to their household employees for whom they paid social security and Medicare taxes. The W-2 is due in the employee’s hands by January 31 of the year following the one in which the wages were paid (unless that date falls on a holiday or weekend; then it’s extended to the next working day). The W-2s and Form W-3 that are filed with the Social Security Administration are due by January 31 also.

Example - Household Employees and Employment Taxes – In 2024 Sherri hired Ruby White to clean her house once a week. Ruby is to receive a gross amount of $70 weekly. Sherri expects to pay Ruby an amount in excess of the tax threshold during the tax year, so she withholds social security and Medicare tax from each of Ruby’s paychecks. Unfortunately, Ruby experienced family problems and was forced to resign her job. Up to that poiand Medicare tax. Sherri must refund the withheld amounts to Ruby. She is not required to give Ruby a W-2.nt, Sherri had paid Ruby $910 in gross wages, and she had withheld social security

-

Sherri hired a new house cleaner, Kathy, to replace Ruby. Kathy worked the remainder of the year and received gross wages of $2,730 on which Sherri withheld $208.85 in social security and Medicare taxes. Kathy did not earn more than $1,000 in any quarter of 2024. By January 31, 2025, Sherri must give Kathy a W-2 showing the gross wages and the withheld tax amounts, and provide a copy of the W-2, along with transmittal Form W-3, to the government.

Then when Sherri files her own tax return, she will include Schedule H with her 1040 and pay a total of $417.70 (Kathy’s share and Sherri’s employer share of social security and Medicare tax) in employment taxes on Kathy’s behalf. (For 2024, the employee’s rate and the employer’s rate for Social Security tax is 6.2%; each pays 1.45% Medicare tax.) Sherri will owe no FUTA tax, because she did not pay $1,000 or more in cash wages to household employees in any calendar quarter during the tax year or in the previous year.

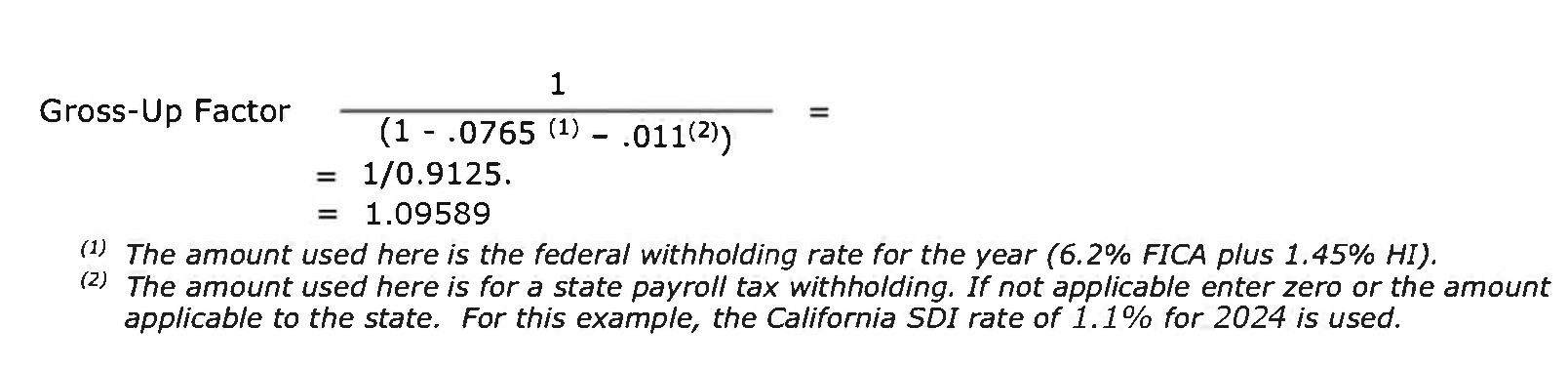

Grossing Up Wages

Frequently a household employer will not withhold employment taxes from the household employee’s payments. When this happens, the employer must then pay the taxes and include the taxes in the employee’s wages (W-2). This is referred to as grossing up the wages. In other words, the payments to the employee are treated as if they were net payments after withholding the required amounts for FICA and, if applicable, state payroll payments.

Gross Up with Both Federal and State Payroll Taxes

In this example we use California SDI payments. The gross-up calculation shown is for 2024 when the SDI rate is 1.1%.

Example – Proof:

Net payment = $200

Grossed up payment = $200 X .09589 = 219.18

W-2 Wage = 219.18

FICA (.0765) = <16.77>

SDI (.009) = < 2.41>

Net Check = 200.00

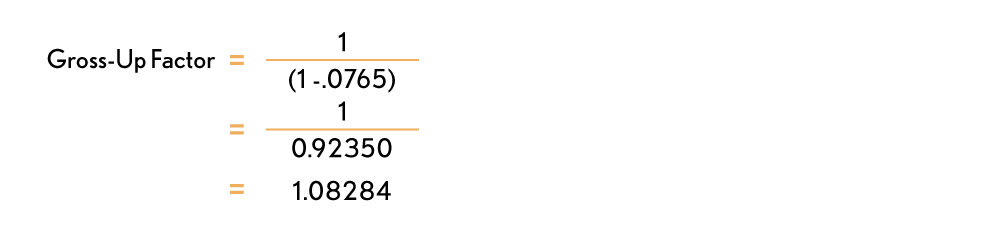

Gross Up With Only Federal Payroll Taxes

Thus, for wages subject just to FICA and HI withholding, the Factor is 1.08284.

Hiring Household Help Through an Agency

Hiring household employees through an agency may be a way for a taxpayer to avoid becoming an employer for these purposes. When help is hired through an agency or service, the agency/service is considered the employer; the taxpayer pays the agency, which, in turn, pays the employee. There are also companies that specialize in payroll services for household employees. Search the internet.

Nursing Services

Wages and other amounts, such as the employer’s portion of employment taxes, paid for nursing services can be included in medical expenses. Services need not be performed by a nurse as long as the services are of a kind generally performed by a nurse. This includes services connected with caring for the patient's condition, such as giving medication or changing dressings, as well as bathing and grooming the patient. These services can be provided in the home or another care facility.

Generally, only the amount spent for nursing services is a medical expense. If the attendant also provides personal and household services, these amounts must be divided between the time spent performing household and personal services and the time spent for nursing services. However, certain maintenance or personal care services provided for qualified long-term care can be included in medical expenses.

Part of the amounts paid for that attendant's meals are also included in medical expenses. Divide the food expense among the household members to find the cost of the attendant's food. If additional amounts for household upkeep were paid because of the attendant, include the extra amounts with the medical expenses. This includes extra rent or utilities paid, because a larger apartment or house was needed to provide space for the attendant.

Additionally, certain expenses for household services or for the care of a qualifying individual incurred to allow the taxpayer to work may qualify for the child and dependent care credit – but the same expense can’t be used both as a medical expense and for the child and dependent care credit. The employer’s share of employment taxes paid on eligible expenses may be included when figuring the credit.