Beneficiary Basis Adjustment

Overview

Inherited Property

The basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent will be one of the following:

-

The fair market value of the property at the date of the decedent’s death (except in rare cases this one applies).

-

The executor can make an irrevocable election to use the “alternate valuation date” under IRC Sec 2032 provided doing so reduces the value of the gross estate and the estate tax on Form 706. If the value of the estate is below the filing threshold for filing Form 706, there cannot be a reduction of the estate tax, and therefore, the alternate valuation date method cannot be used. When eligible, and if the executor makes the alternate valuation date election, then the basis is determined as follows:

-

For property distributed, sold, exchanged, or otherwise disposed of within 6 months after the decedent's death, that property is valued as of the date of distribution, sale, exchange, or other disposition.(IRC Sec 2032(a)(1))

-

If the property is not distributed, sold, exchanged, or otherwise disposed of within 6 months after the decedent's death, the property is valued as of the date 6 months after the decedent's death. (IRC Sec 2032(a)(2))

-

-

In the case of an election under IRC Sec 2032A, its value is determined under such section. Relates to farm or real property used in a closely held business and is referred to as “special use valuation”. There is a limitation on the reduction in value resulting from the special use valuation, which is $1.31 million for 2023 and $1.23 million for 2022.

-

To the extent of the applicability of the exclusion described in IRC Sec 2031(c), the basis in the hands of the decedent. Relates to conservation easements.

Property acquired by bequest, devise, or inheritance includes:

-

Items required to be in the decedent’s gross estate (whether or not an estate tax return is filed).

-

Gifts from the decedent within three years of death, ONLY IF these items are required to be included in the estate tax return.

-

Joint tenancy and community property. If COMMUNITY PROPERTY, the whole property is acquired by inheritance; if JOINT TENANCY, only the decedent’s part that is required to be included in the gross estate is inherited property. However, if the joint tenancy is between spouses and the property would otherwise be community property, it may be possible to establish that the property is actually community property for this purpose.

However, it does not include:

-

Appreciated property received as a gift by a decedent within one year of death, if the property passes back to the donor or spouse of the donor. Basis of this kind of property is the same as the decedent’s basis immediately before death.

-

Payments received by the heirs from sales of property which were reported on the installment basis by the decedent.

Income in Respect of a Decedent (IRD)

There is no basis adjustment for IRD income. IRD refers to untaxed income that a decedent had earned or had a right to receive during their lifetime. IRD is taxed to the individual beneficiaries or entity that inherits this income. Common examples of IRD include:

-

Uncollected compensation, wages, bonuses, commissions.

-

Uncollected vacation and sick pay.

-

Uncollected rents.

-

Retirement income.

-

Distributions from deferred compensation and stock options plans.

-

Gains from the sale of property (where sale occurred before death, but proceeds are not collected until after death. Would include installment notes.

-

Pension and qualified plan distributions.

-

Annuity contracts - If the owner-annuitant of a deferred annuity contract dies before the annuity starting date, and the beneficiary receives a death benefit under the annuity contract, the amount received by the beneficiary in a lump sum in excess of the owner annuitant’s investment in the contract is includible in the beneficiary’s gross income as IRD.

-

if the holder of a contract dies on or after the annuity starting date and before the entire interest in such contract has been distributed, the remaining portion of such interest will be distributed at least as rapidly as under the method of distributions being used as of the date of the holder’s death (IRC Sec 72(s)(1)(A)), and

-

if any holder of such contract dies before the annuity starting date, the entire interest in such contract will be distributed within 5 years after the death of such holder. (IRC Sec 72(s)(1)(B))

-

-

Traditional IRA Distributions – The IRA is not taxable to a beneficiary until the beneficiary receives a distribution.

Items of IRD income are taxed to the beneficiary in the same manner as they would be to the decedent if still living. Thus, capital gains are taxed as capital gains, and uncollected compensation is taxed as ordinary income to the beneficiaries in the year they receive it.

IRD Deduction

IRD also counts toward the decedent’s estate for federal estate tax purposes, potentially creating double taxation. Where there is double taxation, the beneficiaries may be able to take a tax deduction for the amount of estate tax paid on the IRD. BUT BE AWARE: The only way a tax preparer will be aware of a potential IRD deduction when IRD is included on a 1040 is being astute enough to ask if there was an estate tax return filed and an estate tax paid. This slips by practitioners that are unaware of the tax issues created by IRD. The deduction is claimed on 1040 Schedule A Line 16.

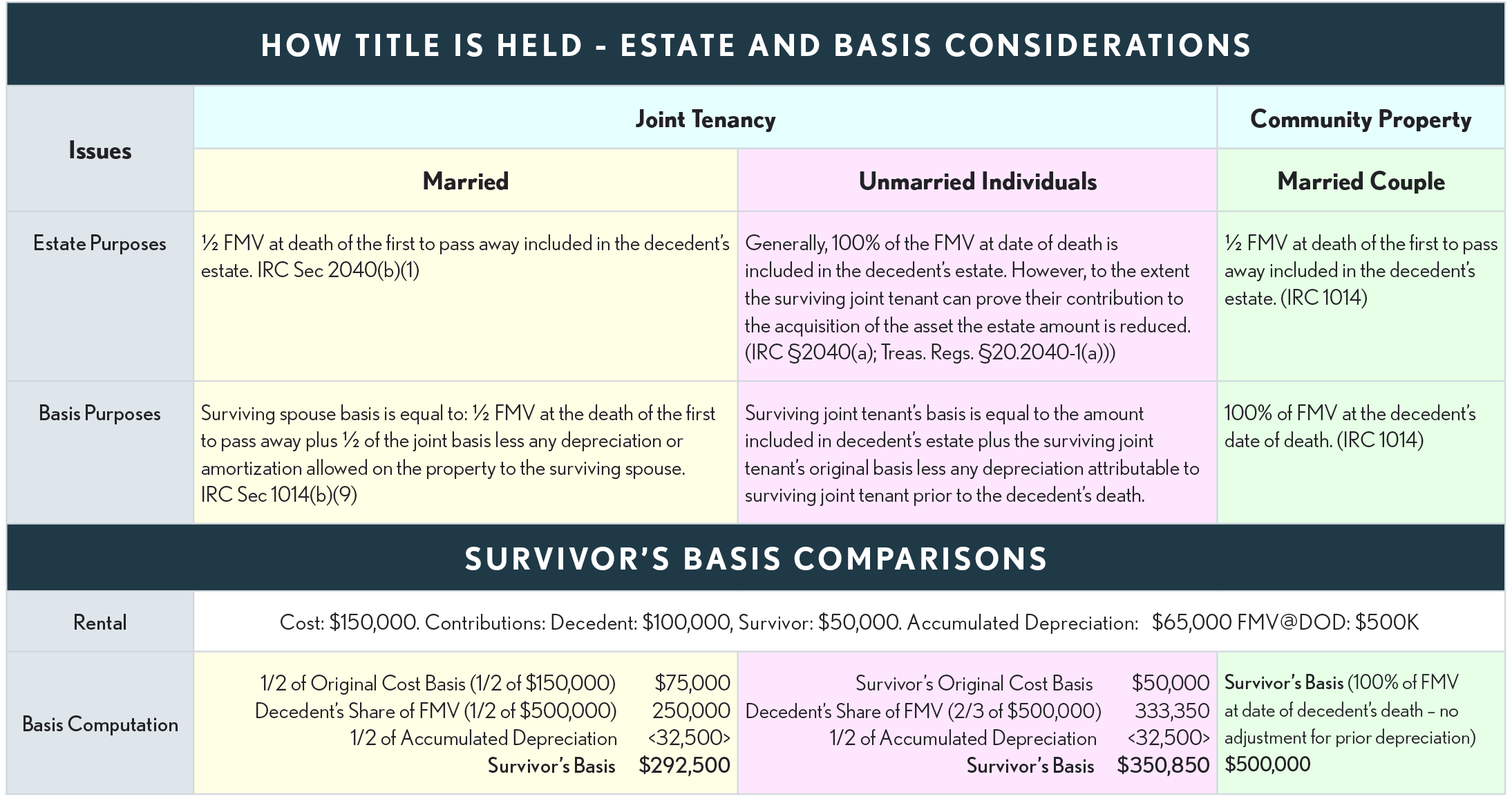

Property Jointly Owned with Non-Spouse

In the case of unmarried joint tenants, when the first joint tenant dies, the presumption is that the entire value of a joint tenancy asset is included in the decedent’s estate. However, if the surviving joint tenant can prove what amount he or she contributed toward purchasing the property, the surviving joint tenant’s basis is stepped up by an amount equal to the amount included in the decedent’s estate. Add the surviving tenant’s original basis to the value of the property that was included in the decedent’s estate and subtract any depreciation or depletion allowed to the surviving joint tenant.

Example: Non-Spouse Joint Tenants - Ross and Rachel, who are not married to each other, own a rental property as joint tenants that they bought for $200,000. Ross contributed $120,000 (60%) to the purchase and Rachel paid $80,000 (40%). When Ross died, the property’s FMV at his date of death was $300,000. Prior to Ross’ death they had claimed depreciation of $70,000. After his death, Rachel’s basis in the rental will be $225,000, figured as follows:

-

| Rachel's original basis (40% of $200,000) | $80,000 |

| Inherited from Ross (60% of $300,000) | 180,000 |

| Less 50% of depreciation (50% x $70,000) | <35,000> |

| Rachel's new basis | $225,000 |

Married Taxpayers

Inheritances between spouses create some unique tax conditions related to inherited basis based, in part on whether their property is held as community property or separate property. In community property states, property can be held either as community property or separate property. While in other states property can be separately or jointly owned.

*Community Property States & Territories include:

| Arizona | Nevada | Wisconsin |

| California | New Mexico | Guam |

| Idaho | Texas | Puerto Rico |

| Louisiana | Washington |

*Community property laws of foreign countries, related to the taxation of U.S. citizens or residents, are recognized, and applied for U.S. tax purposes. Thus, where a determination must be made of whether a property located in a foreign country or income derived from a foreign country is community property or separate property, the community property laws of that country will apply. (IRM 3.38.147.17.1 (01-01-2016).

| Belgium | Guatemala | Portugal |

| Brazil | Mexico | Spain |

| Colombia | Montenegro | Sweden |

| Dominican Republic | Netherlands | Venezuela |

| France | Phillippines |

Example #1 - Where a property is held as separate property by one of the spouses and inherited by the other spouse, the basis in the hands of the inheriting spouse will be FMV of the entire property at DOD. Reason: the inheriting spouse owned no portion of the property and therefore inherited 100% of the property.

-

Example #2 – Where a property is jointly owned (not community property) by both spouses and one spouse passes away, the surviving spouse already owns 50% and only inherits the deceased spouse’s 50%. Thus, the surviving spouse’s basis in the inherited portion will be 50% of the property’s FMV at DOD plus 50% of the joint basis.

Example #3 – Where the taxpayers reside in a community property state and hold the property as community property, when one of the spouses dies, the other spouse’s basis becomes 100% of the FMV at DOD.

Example #4 - Where the taxpayers reside in a community property state, jointly own the property but do not hold the property as community property, the results would be the same as Example #3. Note: In some circumstances where the property was purchased with community funds an attorney may be able to make the case that the property is community property, providing the surviving spouse with a basis equal to 100% of the FMV at DOD. Also, where the taxpayers relocated from a community property state or foreign community property country, an attorney might make the case the property retained its community property character.

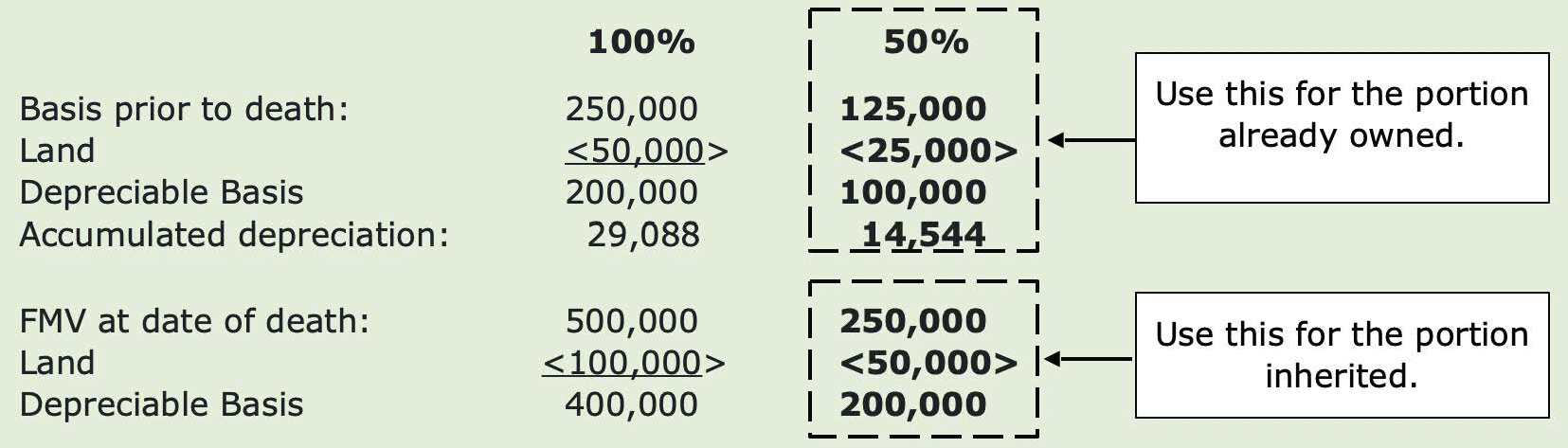

Inherited Depreciable Property

When a depreciable business asset is inherited the depreciation starts over and any accumulated depreciation is disregarded. However, this rule only applies to the inherited portion of the property.

Example 1: Where a property is jointly owned (not community property) by both spouses and one spouse passes away, the surviving spouse already owns 50% and only inherits the deceased spouse’s 50%. Thus, the surviving spouse’s basis in the inherited portion will be 50% of the property’s FMV at DOD and the depreciation starts over for that 50% portion of the property and any pre-death accumulated depreciation associated with that inherited portion is disregarded. The 50% already owned will continue to be depreciated using 50% of the joint depreciable basis and 50% of the accumulated depreciation.

Example 2: Where the taxpayers reside in a community property state and hold the property as community property, when one of the spouses dies, the other spouse’s basis becomes 100% of the FMV at DOD ($500,000 in the example above) and 100% of the prior accumulated depreciation is disregarded. In which case the depreciable basis would start anew at $400,000.

Suspended Passive Losses

When a passive interest is transferred due to death, the accumulated suspended losses from the activity are deductible on the decedent’s final return. The deduction amount is limited to the excess of the basis of the property in the hands of the transferee (heir) over the decedent’s adjusted basis in the property just before death. In other words, the amount of the passive activity loss that equals the step-up in basis due to the decedent's death is not allowed as a deduction to anyone in any tax year. (Code Sec. 469(g)(2))

Example: Robert was the sole owner of a residence used as a rental, a passive activity, when he died in 2022. In his will he left the property to his brother Tom. At Robert’s date of death, the value of the rental was $500,000, his adjusted basis was $494,000, and he had unused passive activity losses of $8,000. Since Tom’s basis of the rental is increased by $6,000 ($500,000 – $494,000), the deduction on Robert’s final return for the year of death would be limited to $2,000 ($8,000 - $6,000). If the stepped-up basis had been $502,000 or more, none of the suspended passive loss would have been deductible ($502,000 – 494,000 = $8,000; $8,000 - $8,000 = $0).