Issues That Apply to Both Credits

Eligible Educational Institution

Eligible institutions generally include any accredited public, nonprofit, or proprietary post-secondary institution eligible to participate in the student aid programs administered by the Department of Education.

Eligible Expenses

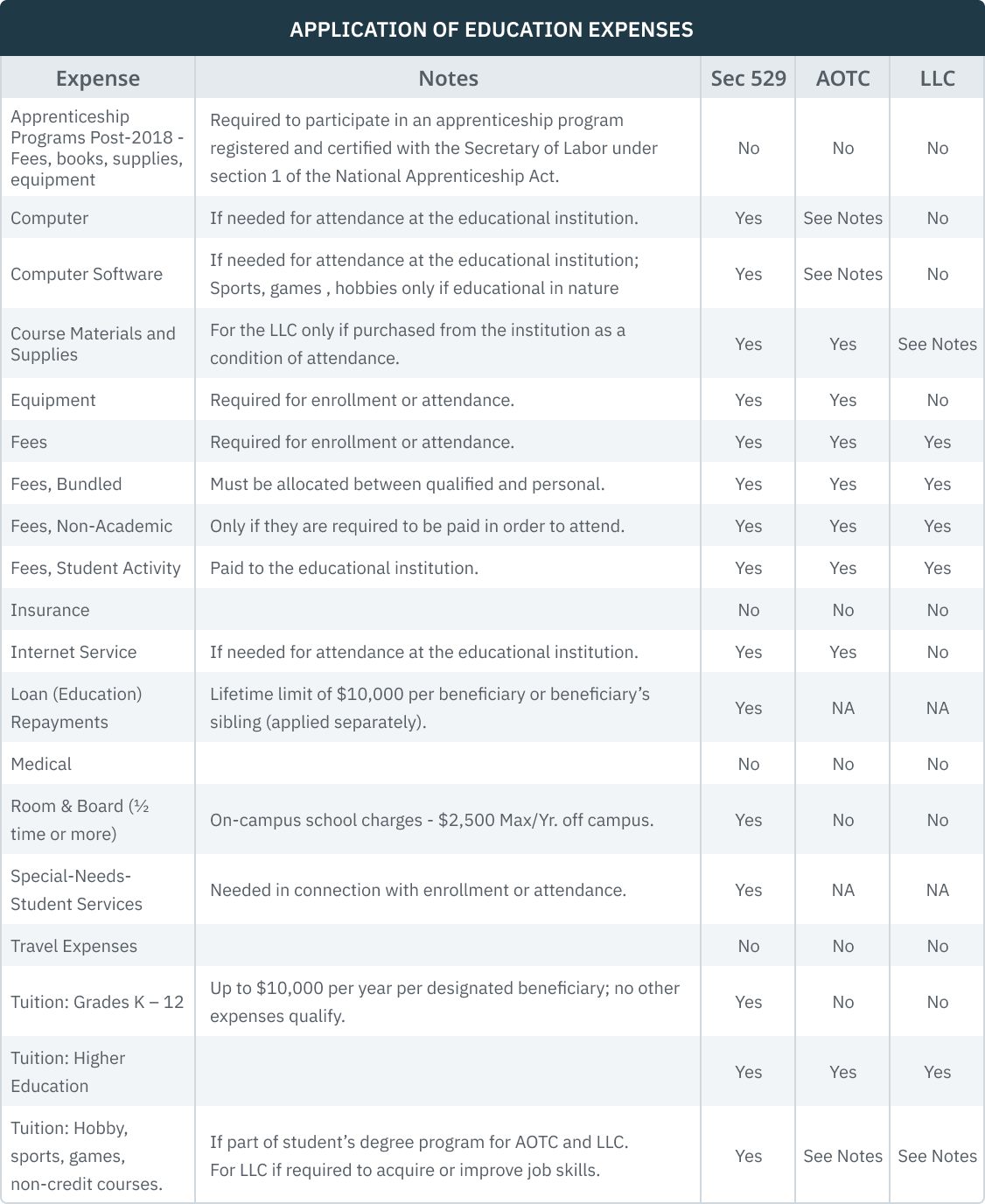

The following table defines the eligible and ineligible expenses that are used in determining the education expenses. This table also includes Sec 529 expenses (see chapter 5.05). There are differences between expenses that qualify for the AOTC and LLC and Sec 529 distributions. (Reg. § 1.25A- 2(d)):

Who Pays and Who Gets the Tuition Credit

The regulations provide that solely for education credit purposes, if a third party (someone other than the taxpayer or a claimed dependent) makes a payment directly to an eligible educational institution for a student’s qualified tuition and related expenses, the student is treated as receiving the payment from the third party, and, in turn, paying the qualified tuition and related expenses. Furthermore, qualified tuition and related expenses paid by a student are treated as paid by the taxpayer if the student is a claimed dependent of the taxpayer. (Reg §1.25A-5(a), Reg §1.25A-5(b))

The regulations also provide that if a taxpayer is eligible to but does not claim a student as a dependent, only the student can claim the education credit for the student’s qualified tuition and related expenses. (Reg § 1.25A-1(f))

Example: Connie has one dependent, her son Frank. Frank pays qualified tuition and related expenses to attend State University during the year. Although Connie is eligible to claim Frank as a dependent on her federal return, she does not do so. Frank is allowed to claim an education tax credit on his return, assuming he meets all other requirements for the credit. Connie cannot claim the credit for Frank’s education expenses.The result is the same even if Connie had paid Frank’s tuition and related expenses – if she doesn’t claim Frank as a dependent, the credit can only be claimed by Frank.

-

Example – Fees Paid Directly to Educational Institution - University V offers a degree program in Dentistry. In addition to tuition, all students enrolled in the program are required to pay a fee to University V for the rental of dental equipment. Because the equipment rental fee must be paid to University V for enrollment and attendance, the tuition and the equipment rental fee are qualified tuition and related expenses (applies for both the AOTC and LLC).

-

Example – University Required Expenses - First-year students at College W are required to obtain books and other reading materials used in its mandatory first-year curriculum. The books and other reading materials are not required to be purchased from College W and may be borrowed from other students or purchased from off-campus bookstores, as well as from College W's bookstore. College W bills students for any books and materials purchased from College W's bookstore. Under the proposed regulations: - If the taxpayer claims the LLC - the expenses paid to College W for the first-year books and materials purchased at its bookstore are not qualified tuition and related expenses, because the books and materials are not required to be purchased from College W for enrollment or attendance at the institution.- If the taxpayer claims the AOTC – the expenses paid to College W for the books and materials are qualified tuition and related expenses, provided they are needed for meaningful attendance in the student’s course of study. (Prop Reg 1.25A-2(d)(7), Ex. 3), is this final yet?

-

Treatment of a Comprehensive or Bundled Fee

If a student is required to pay a fee (such as a comprehensive or a bundled fee) to an eligible educational institution that combines charges for qualified tuition and related expenses with charges for personal expenses, the portion of the fee that is allocable to personal expenses is not included in qualified tuition and related expenses. The determination of what portion of the fee relates to qualified tuition and related expenses and what portion relates to personal expenses must be made by the institution using a reasonable method of allocation. (Reg. § 1.25A-2(d)(4))

Example – Bundled Fees - College Y requires all students to live on campus. It charges a single comprehensive fee to cover tuition, required fees, and room and board. Based on College Y's reasonable allocation, sixty percent of the comprehensive fee is allocable to tuition and other required fees not allocable to personal expenses, and the remaining forty percent of the comprehensive fee is allocable to charges for room and board and other personal expenses. Therefore, only sixty percent of College Y's comprehensive fee is a qualified tuition and related expense.

-

Prepayment Rule

If qualified tuition and related expenses are paid by the taxpayer during one tax year for an academic period that begins during the first three months after that tax year, that academic period is treated as beginning during the tax year in which the payment is made. In other words, if qualified tuition and related expenses are paid during one tax year for an academic period that begins during the first three months of the taxpayer's next tax year (i.e., in January, February, or March of the next tax year for calendar year taxpayers), an education credit is allowed with respect to the qualified tuition and related expenses only in the tax year in which the expenses are paid. (Reg § 1.25A-5(e)(2)(i); Terrell, TC Memo. 2016-85, Dec. 60,599(M))

CAUTION: The opposite is not true. Tuition payments made in one year for the next year cannot be credited to the next year because of the cash basis taxpayer rules (McCarville, TC Summary Opinion 2016-14). This is a mistake your clients can easily make.

Example - Prepayment Rule - Alan, who is a calendar year taxpayer and not a dependent of another taxpayer, enrolls full-time at College Z, with the Spring 2022 his first semester of attendance. He continues at College Z through the Spring 2023 semester. The following recaps his tuition payments during that period:

| Amount Billed | Date Bill Rec'd | Applies to Semester | Amount Paid | Date Paid |

| $5,000 | Dec 2022 | Spring 2023 | $1,000 | 12/15/22 |

| $4,000 | 2/15/23 | |||

| $7,000 | Aug 2023 | Fall 2023 | $7,000 | 9/1/23 |

| $7,000 | Dec2023 | Spring 2024 | $1,000 | 12/15/23 |

| $6,000 | 2/15/24 |

He may claim an education tax credit on his 2023 return with respect to the $1,000 he paid to College Z on Dec. 15, 2022 for the 2023 spring semester. Alan may claim an education credit on his 2023 return with respect to the $12,000 he paid to College Z during 2023 ($4,000 + $7,000 + $1,000). On his 2024 return, he may claim an education credit with respect to the $6,000 he paid to College Z on Feb. 15, 2024. (Reg 1.25A-5(e)(2)(ii))

Hobby Courses

Qualified tuition and related expenses do not include expenses that relate to any course of instruction or other education that involves sports, games, hobbies, or any noncredit course, unless the course or other education is part of the student's degree program, or in the case of the Lifetime Learning Credit, the student takes the course to acquire or improve job skills. (Reg. § 1.25A-2(d)(5))

Example – Hobby Courses- As a degree student at College Z, Amy is required to take a certain number of courses outside of her chosen major in Economics. To fulfill this requirement, Amy enrolls in a square dancing class offered by the Physical Education Department. Because Amy receives credit toward her degree program for the square-dancing class, the tuition for the square-dancing class is included in qualified tuition and related expenses.

-

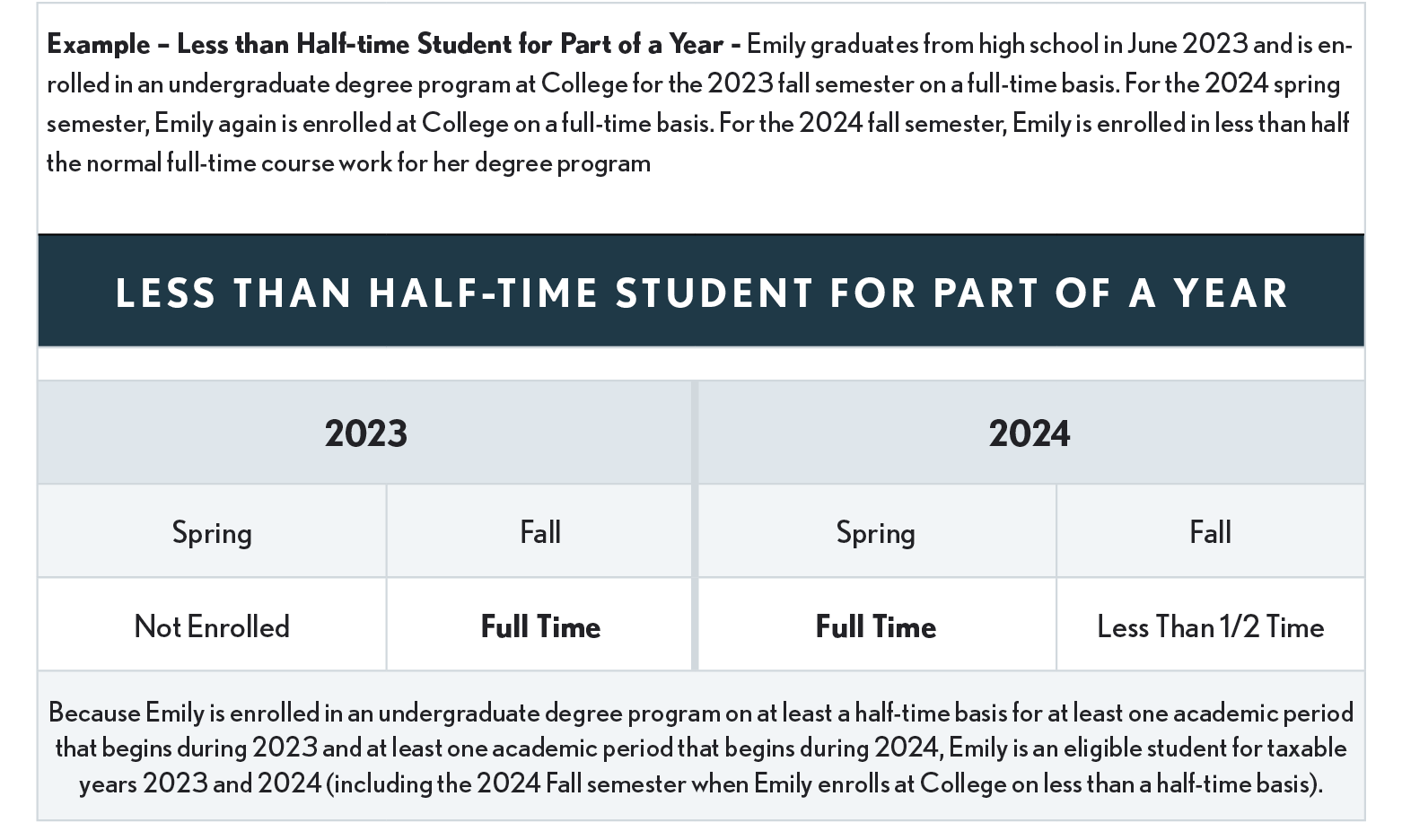

Half-Time Student Requirement

For purposes of the AOTC for at least one academic period during the year, the student must be enrolled for at least half of the normal full-time workload for his course of study. (Code Sec. 25A(b)(3)(B)) Form 1098-T, Tuition Statement, has a check box for the institution to indicate if the student was a half-time student.

Interaction of Scholarships and Tax Credits

For education credit purposes, qualified tuition must be reduced by tax-free scholarship amounts (including fellowships) excluded from income under Code Sec. 117 except to the extent, by the terms of the scholarship, it may (or must) be applied to room and board, in which case it is reported as taxable income if the student is required to file a tax return. (Reg. § 1.25A-5(c)(3))

Scholarship Terms

The use of scholarship funds depends upon the terms of the scholarship. If the scholarship specifies it must be used towards tuition and expenses, then the scholarship is non-taxable and must reduce expenses that qualify for the education credits. If the scholarship species it is for room and board, then it must be used for room and board and is therefore taxable income. Where the funds can be used for any education purpose (discretionary), the use of the funds can be allocated among the educational expenses that provides the best overall tax benefits.

Federal Student Aid

Federal student aid, including Pell Grants, can be used to cover a variety of costs, generally including tuition and fees normally assessed; books, supplies, transportation, and miscellaneous personal expenses; and living expenses such as room and board.

GI Bill

Payments to vets under the GI Bill for tuition and allowances is treated as support provided by the government when determining who pays over half of a student’s support. (2021 Pub 17 page 36)

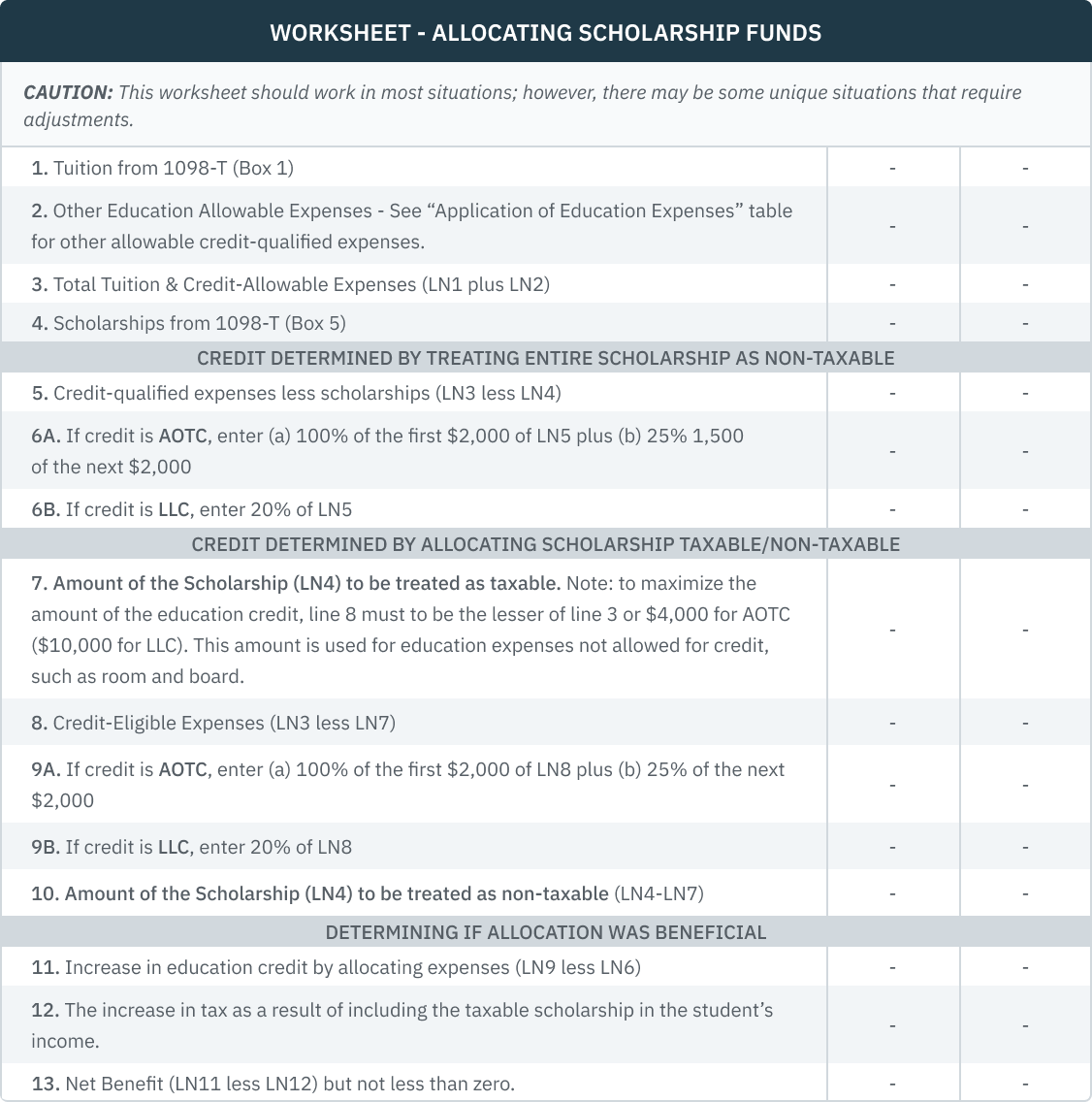

Scholarship Strategy

Being able to allocate scholarships where the terms permit provides a significant strategy for maximizing the education credits. Consider the following:

-

If the terms of a scholarship permit, a student may choose to allocate (in any portions) the use of scholarship funds to either credit-qualified expenses or other education expenses, such as room and board, that are not qualified for the credits. (Reg § 1.25A-5(c)(3))

-

Any amount allocated to credit-qualified expenses is non-taxable and reduces the expenses that are qualified for an education credit.

-

Any amount allocated to other than credit-qualified expenses (such as room and board) becomes taxable income on the student’s tax return if the student is required to file a tax return.

Observation: If the parent(s) claim the student as a dependent, the parent(s) get the education credit, but the taxable scholarship amount is included in the student’s income, and since it is considered earned income, it is taxed at the student’s tax rate.

Making this allocation can become complicated since one must take into consideration the benefit of the education credit versus any tax to the student as a result of treating some portion of the scholarship amount as taxable.

Example: Student receives a scholarship (Pell Grant) in the amount of $5,000. Her tuition for the year was $5,000. So, her 1098-T will show $5,000 in box 1 (payment received for qualified tuition and related expenses) and $5,000 in box 5 (scholarships or grants). She also had other credit-qualifying expenses of $1,500, bringing the total expenses to $6,500. Without allocating her scholarship funds, the scholarship would be non-taxable and reduce her expenses qualifying for the credit to $1,500 and a resulting AOTC of $1,500 (100% of $1,500). The student is in the 12% tax bracket.

-

By using the worksheet and allocating the scholarship between taxable and non-taxable income, the credit can be increased by $1,000 to $2,500 ((100% x $2000) + (25% x $2000)). However, the portion of the scholarship treated as taxable is taxable to the student, and in our example increases the student’s tax by $300, resulting in a net tax benefit of $700.

Payments for Services

Scholarship or fellowship grants are taxable to the recipient if they are paid for teaching, research, or other services as a condition for receiving the grant, unless the payments are received under:

-

The National Health Service Corps Scholarship Program,

-

The Armed Forces Health Professions Scholarship and Financial Assistance Program, or

-

A comprehensive student work-learning-service program (as defined in section 448(e) of the Higher Education Act of 1965) operated by a work college (as defined in that section).

When part of the scholarship is taxable because it was payment for services, i.e., wages, the scholarship provider should issue a Form W-2 for the taxable amount. It is possible that this amount may also be included in the Box 5 (scholarships or grants) amount on Form 1098-T. Therefore, an analysis of the make-up of the Box 5 amount must be performed to ensure that there isn’t duplicate reporting of income.

Third-Party Installment Plan

Where an outside company agrees to collect tuition payments over a period of time (usually 10 months) and remits the payments to the educational institution on a predetermined schedule, the date of the payment for purposes of computing the education credit is determined as follows:

-

Where the outside agent is an agent of the taxpayer, the taxpayer is treated as having paid qualified expenses on the date the company pays the higher-education institution.

-

Where the outside company is an agent of the higher-education institution, the taxpayer is treated as paying the qualified expenses on the date the taxpayer pays the outside company. (Reg. § 1.25A-5(e)(4))

Form 1098-T Issues

Form 1098-T Mandatory - A taxpayer is not allowed to claim the AOTC, the Lifetime Learning credit or, for years before 2021, the higher education tuition deduction, unless the taxpayer has received a Form 1098-T from the educational institution (Trade Act Sec 804(a)(1)). Thus, taxpayers won’t be able to file their returns on which they claim education tax benefits until they have received the Form 1098-T.

An eligible educational institution will send the student a Form 1098-T, Tuition Statement, generally by January 31 of the year following the year of attendance. The 1098-T also provides other information, such as adjustments made for prior years; the amount of scholarships or grants, reimbursements, or refunds; and whether the student was enrolled at least half-time or was a graduate student.

Missing 1098-T - Many educational institutions do not mail the form, but rather make the form available to the student online. If a student claims not to have received the form, have them double check their online account with the school.

1098-T Received by a Dependent - 1098-Ts received by a dependent of the taxpayer are treated as received by the taxpayer (Trade Act Sec 804(a)(2)).

Expenses Not Included on the 1098-T - A taxpayer that substantiates payment of qualified tuition and related expenses that are not reported on Form 1098–T, may include those expenses in computing the amount of the education tax credit allowable for the taxable year. (Prop Reg 1.25A-1(f), NPRM REG-131418-14))

CAUTION

Practitioners should avoid claiming the education credits or the higher education tuition deduction for clients that have not received a corresponding 1098-T or can substantiate the tuition as indicated above.

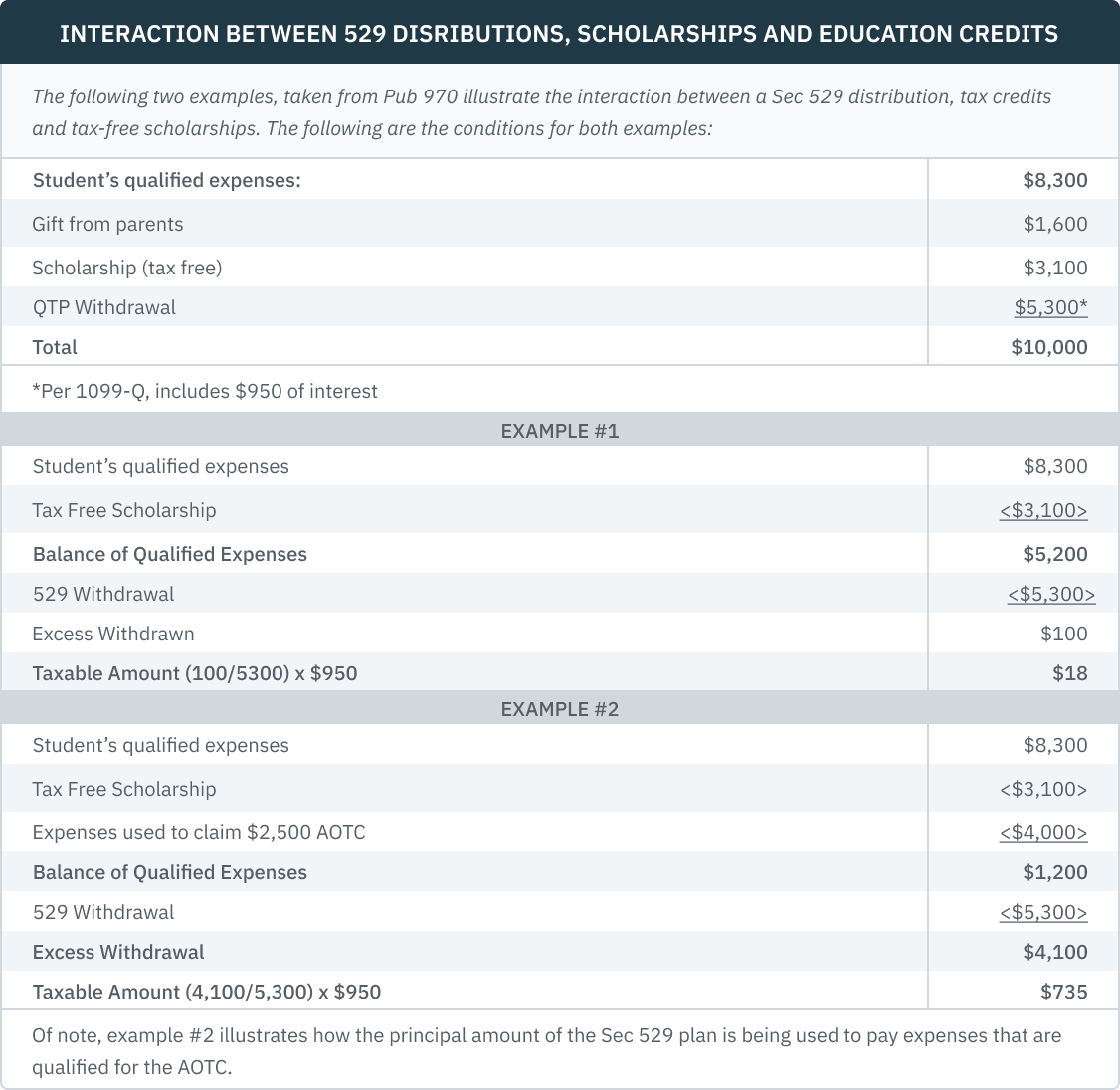

Coordination with Coverdell ESAs & Qualified Tuition Programs

A taxpayer can claim an AOTC or LLC for a tax year and exclude from gross income amounts distributed (both the principal and the earnings portion) from a Coverdell Education Account for the same student, as long as the distribution is not used for the same educational expenses for which a credit was claimed.

Special Situations

-

Source of Funds Used to Pay Expenses - The credits can be claimed for expenses paid with a student’s earnings, loans, gifts, inheritances, and personal savings. However, if higher education expenses are paid with a tax-free scholarship, Pell grant, or employer-provided educational assistance, no credit is allowed for those amounts. See “Scholarship Strategy” above.

-

Credits Not Available for Same Student in One Tax Year - For each eligible student, a taxpayer can elect for any tax year only one of the credits. For example, if the taxpayer elects to take the AOTC for a child, he/she can’t, for that same child, also claim the LLC for that year.

-

AOTC vs. LLC - A taxpayer can claim the AOTC for four years of a child’s post-secondary education and claim the LLC for that same child in other tax years.

-

Multiple Students in Family - If a taxpayer pays qualified expenses for more than one eligible student in the same year, he/she can choose to take credits on a per-student, per-year basis., This means that, for example, the taxpayer can claim the AOTC for one child and the LLC for another child in the same tax year.

-

Recapture of Credits - If a taxpayer receives a refund in a later year of an amount used to figure a higher education credit, the credit may have to be recaptured.

-

Nonresident Alien Taxpayers and Dependents - If a taxpayer or the taxpayer's spouse is a nonresident alien for any portion of the taxable year, no education tax credit is allowed unless the nonresident alien is treated as a resident alien by reason of an election under Section 6013(g) or (h). In addition, if a student is a nonresident alien, a taxpayer may not claim an education tax credit with respect to the qualified tuition and related expenses of the student unless the student is a claimed dependent (as defined in §1.25A-2(a)). A “claimed dependent” is a dependent the taxpayer can claim on their tax return., Among other requirements, a nonresident alien student must be a resident of a country contiguous to the United States in order to be treated as a dependent.

-

Pandemic-related Emergency Financial Aid Grants – Emergency financial aid grants to a student from a federal agency, state, Indian tribe, higher education institution or scholarship-granting organization due to an event related to the COVID-19 pandemic are not included in the student’s gross income. These payments were intended to assist the student with unexpected expenses for food, housing, course materials, technology, health care (including mental health care), or child care when campus operations were disrupted due to COVID-19. Such payments need not be reported by higher education institutions on Form 1099-MISC (because the payments are nontaxable) nor on Form 1098-T, Box 5 (scholarships or grants). However, amounts that qualify for the education credits must be included by the school in 1098-T, Box 1 (payments received for qualified tuition and related expenses), and students who used the grants to pay for qualified tuition and related expenses may use them in determining their education credit. (Various provisions in the CARES Act, CCA 2021, and ARPA; IR-2021-70) See IRS website for specific citations to the Acts, more information, and FAQs: https://www.irs.gov/newsroom/higher-education-emergency-grants-frequentlyasked-questions.,

Potential Gifting-Education Credit Strategy

Prior to the kiddie tax age being increased to include full time students through age 23, a commonly used tax strategy was to gift appreciated stock to a child and then have the child sell the stock at a lower tax rate and use the funds to pay for the child’s education. Since there is no longer any tax benefit to gifting appreciated stock to a full- time student under 24 to pay for education, what if the grandparents or other trusted relative or friend are in a lower tax bracket and....

The child's parents gift each grandparent or sets of grandparents enough appreciated stock that when sold would yield an after-tax amount that the grandparent in turn uses to pay the child's tuition?

-

Gifts used for education (only tuition) are not subject to gift tax so the grandparents would have no gift tax issues. Caution - grandparents (or whoever) would need to make tuition payments directly to the educational institution to avoid the gift tax issue if the amount gifted exceeds the annual gift exclusion.

-

If the grandparents are retired their income might be such that they would be in the zero capital gains tax rate., Caution – Be careful that the additional income from including the gain upon sale of the stock doesn't cause the grandparents to have more taxable Social Security or have other detrimental effects on AGI-based limitations.

-

Assuming the parents claim the child as a dependent, and their MAGI permits, they would be able to claim the education tax credit since the credit goes to the individual claiming the dependent even if they did not pay the tuition.

CAUTION

If the parents' MAGI causes the education credit to be phased out (or eliminated), it makes using this strategy less appealing – but if the parents would have sold the stock to pay for the education expenses anyway, transferring the gain to the grandparents would still be an appropriate strategy as it will reduce the parents' AGI for various phaseouts. It would help lower the parents' state tax, especially if the state doesn't have a capital gain tax rate but could increase the grandparents' state tax – so you’d need to run the actual numbers to see if there's an overall family savings.