American Opportunity Tax Credit (AOTC)

Eligible Student

Generally, an eligible student for the AOTC can be the taxpayer and spouse and their dependents that are enrolled at an eligible educational institution for at least one academic period (semester, trimester, quarter) during the year.

The dependent is any person for whom the taxpayer claims a dependency exemption. It generally includes the taxpayer’s qualified child who is under age 19 or who is a full-time student under age 24. The student must also meet all of the following requirements.

-

Had not completed the first 4 years of post-secondary education before the tax year of the credit.

A student who was an undergraduate during the first part of the taxable year and (1) became a graduate student that same year, (2) has not completed the first 4 years of post-secondary education as of the beginning of the tax year, and (3) has not claimed the AOTC for more than 4 years, will qualify

-

For at least one academic period beginning in the tax year of the credit, was enrolled at least half-time in a program leading to a degree, certificate, or other recognized educational credential.

-

An eligible student is one that has no felony drug conviction. Having no felony drug conviction means the student has not been convicted of a Federal or state felony offense for possession or distribution of a controlled substance as of the end of the taxable year for which the credit is claimed.

Allowance Period

The AOTC is allowed with respect to qualified tuition and related (QT&R)

expenses paid for the first four years

of the student's post-secondary education in a degree or certificate program,

if the student has not completed the first four years of postsecondary

education before the beginning of the fourth tax year. And, for each eligible

student, the AOTC may be claimed for four tax years. (Code Sec 25A(i)(2)) Note:

There is nothing in the law that limits the credit to just expenses incurred to

obtain a bachelor’s degree.

Credit Amount – Allowed on a per-eligible-student basis, the AOTC equals the sum of:

(a) 100% first $2,000 of each eligible student’s QT&R expenses plus

(b) 25% next $2,000 of that student’s QT&R expenses.

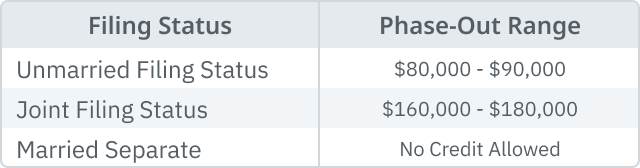

Credit Phase-Out Provisions

For higher-income taxpayers, this credit begins to phase out for modified AGI (MAGI) in excess of $80,000 ($160,000 for married couples filing jointly). The phaseout amounts are not inflation indexed. MAGI is the taxpayer’s regular AGI increased by: Foreign earned income and housing exclusion and housing deduction (Sec 911), amounts excluded by taxpayer from sources in American Samoa (Sec 931), and amounts excluded by taxpayer from sources in Puerto Rico (Sec 933).

Refundability

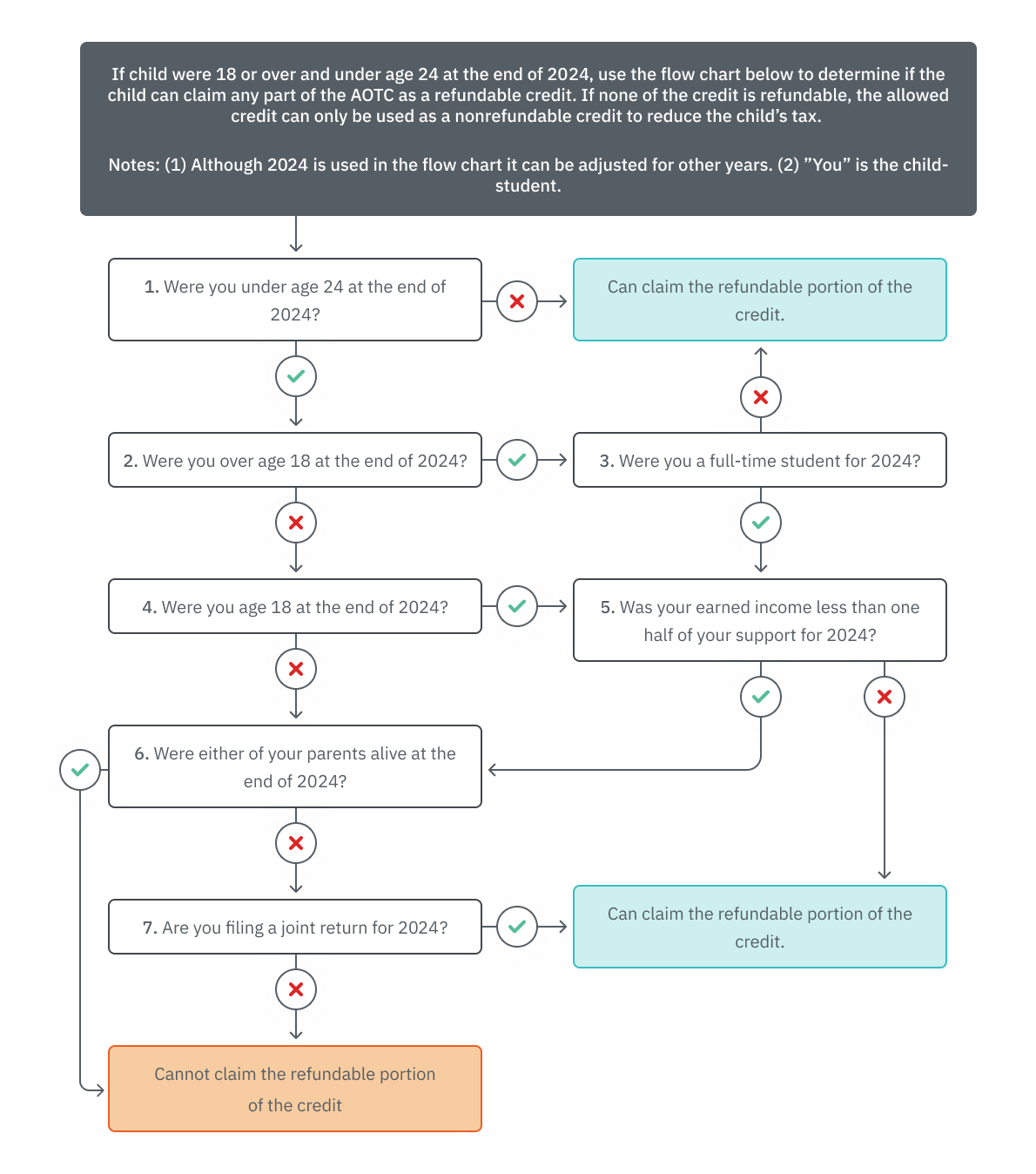

40% of the AOTC (after application of the phase-out limitation) is refundable (Code Sec 25A(i)(5)). The refundable provision does not apply to:

-

A taxpayer who is a child subject to the kiddie tax rules. (Generally, any child under age 18 or any child under age 24 who is a student whose earned income is less than one-half of the child’s support, who has at least one living parent, and does not file a joint return may be subject to the “kiddie tax,” depending on the amount of the child’s investment income). (Com Report; Chief Counsel Advice 201509030) See chapter 8.02 for more information about the Kiddie Tax.

-

Residents of a U.S. possession. However, the refundable portion may be claimed as a credit in the possession in which they reside.

Any portion of the credit that isn’t used to offset the taxpayer’s regular tax or that isn’t refundable is lost and cannot be carried over or carried back to another year.

Example – Refundable Portion of AOTC: Albert, who is not subject to the kiddie tax rules, is eligible for a $2,500 AOTC and his MAGI is below the phaseout threshold. The maximum refundable portion of Albert’s AOTC is $1,000 ($2,500 x .4). His tax liability is $1,900. After first using the credit to offset his tax liability, he has $600 of credit remaining ($2,500 – 1,900). He is entitled to a refundable credit of $600, the lesser of the maximum portion of the credit that could be refunded ($1,000) or the balance of the credit left after reducing his regular tax to zero. If Albert’s tax had been $1,300, he would have $1,200 of credit left after offsetting his tax ($2,500 –1,300). But he could only claim a refund of $1,000 of the remaining credit.

-

Example – Refundable Portion of AOTC: Bob and Carlene are married and file a joint return. They are eligible for a $2,500 AOTC, and their modified AGI is $170,000, which exceeds the phaseout threshold, so they must reduce their AOTC by 50% ((170,000 -$160,000)/$20,000) to $1,250. Therefore, the maximum refundable portion of their AOTC would be $500 ($1,250 x .4).

-

Student Credit When Parents Don’t Claim

There is an often-overlooked opportunity to claim at least a portion of the AOTC when the parents’ AGI is too high to claim the credit. The regulations provide that if a taxpayer is eligible to, but does not claim a student as a dependent, only the student can claim the education credit for the student’s qualified tuition and related expenses. (Reg § 1.25A-1(f))

Refundability - 40% of the AOTC (after application of the phase-out limitation) is refundable. (Code Sec 25A(i))

However, the refundable provision does not apply to a taxpayer who is a child subject to the kiddie tax rules (a qualified child). Generally:

-

Any child under age 18, or 18 or over and under age 24 who is a student,

-

Whose earned income is less than one-half of the child’s support,

-

Who has at least one living parent, and

-

Who does not file a joint return…

May be subject to the “kiddie tax,” depending on the amount of the child’s investment income. (Com Report; Chief Counsel Advice 201509030)

Thus, if a parent does not claim the child as a dependent and the child is not self-supporting, the child can claim the credit, but not the refundable portion.

Alternative Minimum Tax

The AOTC is allowed against the AMT. (IRC Sec 25A(i)(5))

Integrity Provisions

These provisions prohibit:

-

An individual from retroactively claiming the AOTC by amending a return for any prior year in which the individual, or a student for whom the credit is claimed, did not have a taxpayer identification number (Act Sec 206).

-

The credit from being claimed for any year unless the taxpayer includes the employer identification number of any institution to which qualified tuition and related expenses were paid with respect to the individual (student) (Act Sec 211).

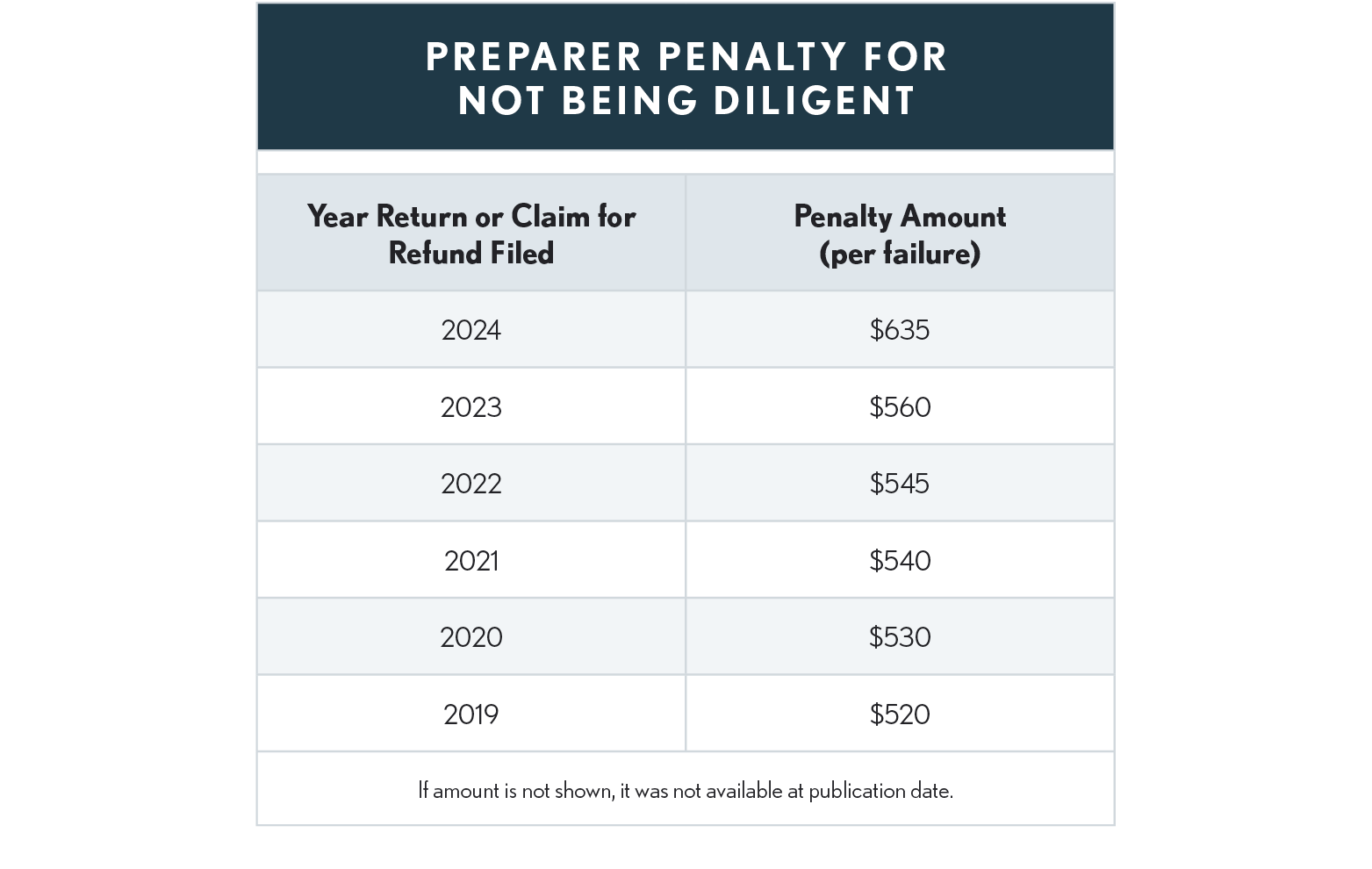

Preparer Due Diligence

The PATH Act of 2015 added preparer due diligence requirements similar to those imposed for the EITC. This penalty, which originally started at $500, is inflation adjusted annually. See table for amount for the last few years.

Due diligence requirements apply for AOTC, EITC and child tax credits, with Head of Household filing status added beginning for tax year 2018. A completed Form 8867, Paid Preparer’s Due Diligence Checklist, or successor form must be included with any return on which any of these tax benefits is claimed. The data entered on the Form 8867 must be based on information provided by the taxpayer or otherwise reasonably obtained by the preparer. The preparer must retain for the period described in the Form 8867 instructions copies of any documents provided by the taxpayer and on which the preparer relied in completing Form 8867 and, for the AOTC, the worksheet from Form 8863 instructions (or a comparable worksheet).

Taxpayer Disallowance Periods

There are disallowance periods for taxpayers who improperly claim the credit. Where a taxpayer improperly claims the credit, a disallowance period applies where no credit is allowed. Where the improper claim is due to:

-

Fraud - the disallowance period is 10 years.

-

Reckless or intentional disregard of rules and regulations (not fraud) - the disallowance period is 2 years.