CA SALT Cap Workaround

Pass-through Entity Elective Tax

CA Assembly Bill 150 (AB 150) was enacted in 2021 adopting IRS Notice 2020-75 guidance allowing state and local income taxes imposed on and paid by a partnership or S corporation on its income to be allowed as a deduction by the partnership or S corporation, effectively circumventing the SALT limitations by being able to deduct the state tax at the entity level and not as a Schedule A itemized deduction.

Important Notice

For 2022 and subsequent years, the FTB is requiring those that wish to participate in the program to pre-pay an amount that is the greater of $1,000 or 50% of the elective tax paid for the prior taxable year.

Here Is How It Works

Qualified passthrough entities (PTEs) that file a CA tax return can pay and deduct a passthrough entity tax of 9.3% on qualified net income on behalf of those partners or shareholders who elect to participate. Qualified net income is the sum of the K-1 distributive income from the entity including guaranteed payments to partners.

Example: Joe and Barry, California residents, are partners in the JB Partnership (JBP) that operates exclusively in California. In 2024, JBP’s taxable income is $400,000. Joe and Barry are each in the 8% tax bracket for their individual California returns. They are each allocated $200,000 (K-1distribution) of taxable income from JBP and their state tax on that distribution would be $16,000 each. Under the SALT limitation, they would each be limited to a $10,000 deduction of the state tax on their federal returns.If they both elect to participate in CA’s pass-through entity tax scheme, and JBP paid the tax, JBP would get a $37,200 ($200,000 x 9.3% = $18,600 x 2) deduction on its Form 1065 for the state income tax paid on behalf of the partners, thus lowering JBP’s federal taxable income to $362,800 ($400,000 - $37,200). Instead of showing $200,000 of taxable income from JBP, Joe and Barry’s 1065 Schedule K-1s from JBP will each report taxable income of $181,400, and they will each take credit on their Form 540 for the $18,600 of CA tax paid on their behalf by JBP. So, Joe and Barry get the benefit of a federal tax deduction for the CA income tax paid that reduces the taxable income passed through to them from JBP and they get a credit on their individual CA returns for the tax paid by JBP. Each would also be able to deduct up to $10,000 of other state and local income and property taxes that they paid during the year.

-

Effective Dates

Tax years 2021 through 2030

Qualified Pass-Through Entities

Qualified pass-through entities for purposes of this workaround include:

-

S corporations and

-

Partnerships,

-

LLCs taxed as an S corporation or partnership.

A trust, including a grantor trust, that receives a pass-through credit from one of the qualified entities shown above may pass the credit through to its beneficiaries. The credit being passed to a beneficiary will be reported on Form 541 K-1, line 13d, Other Credits.

Qualified entities DO NOT include publicly traded partnerships or entities allowed or required to be part of a combined reporting group.

The Tax

Paying the 9.3% tax at the entity level to avoid the SALT limit may not be beneficial for all entity owners. Luckily the 9.3% election is applied only to owners who elect this treatment rather than to the entity as a whole.

CA Tax Credit

Qualified taxpayers are eligible to claim a nonrefundable credit for tax paid on the qualified taxpayers’ pro rata or distributive share and guaranteed payments included in the qualified entity’s qualified net income. The credit cannot be used against the 1% Mental Health Services Tax.

Excess CA Credit

In the case where the credit exceeds the “net tax,” on the entity, the excess may be carried over to reduce the “net tax” on the individual taxpayer in the following taxable year and succeeding four years (5-year carryover), if necessary, until the credit is exhausted. The 5-year carryover period of credits originally claimed prior to January 1, 2026, applies even after the credit has expired.

Sole Proprietors

May want to consider switching to a partnership, if applicable, or an S corporation to take advantage of this SALT workaround. A sole proprietor operating as a single member limited liability company (SMLLC) cannot make the election.

Election

The PTE election is irrevocable and must be made on an original, timely filed return for the taxable year of the election.

Qualified Net Income

Is defined as the sum of the pro-rata share or distributive share of income and guaranteed payments subject to personal income tax of the electing qualified PTE’s qualified taxpayers.

-

For an S Corporation - the qualified net income for a qualified taxpayer can generally be computed by taking the sum of Schedule K-1 (100S) lines 1-10 minus lines 11 and 12.

-

For a Partnership - the qualified net income for a qualified taxpayer can generally be computed by taking the sum of Schedule K-1 (565/568) lines 1, 2, 3, and 4c through 11 minus lines 12 and 13.

Negative Income

A taxpayer with negative income could never be included in the qualified net income of the entity.

Participation

The electing qualified PTE may still elect to pay the elective tax even if some partners, shareholders, or members do not consent to having their pro-rata or distributive share of income and guaranteed payments included in the electing PTE’s qualified net income.

FTB Forms

The following PTE elective tax forms and instructions:

-

Form FTB 3893, Pass-Through Entity Elective Tax Payment Voucher - The PTE elective tax payment can be made electronically using Web Pay on FTB's website. Using Web Pay ensures the payment is timely credited to their account. Entities can also use the FTB 3893 payment voucher. Once the payment is made, the payment will remain as a PTE elective tax until a tax return is filed.

-

Form FTB 3804, Pass-Through Entity Elective Tax Calculation - Attach the completed form FTB 3804 to the electing qualified PTE’s Form 100S, California S Corporation Franchise or Income Tax Return; Form 565, Partnership Return of Income; or Form 568, Limited Liability Company Return of Income.

Form FTB 3804 also includes a Schedule of Qualified Taxpayers that requires the electing qualified PTE to identify the qualified taxpayers, report the pro-rata share or distributive share and guaranteed payments of qualified net income amounts, and calculate the elective tax credit amounts. This schedule will allow the FTB to trace the elective tax credit payments from the electing qualified PTE return to the qualified taxpayers’ returns upon receipt of the completed form FTB 3804.

-

Form FTB 3804-CR, Pass-Through Entity Elective Tax Credit - Is used to claim the amount of the credit that equals 9.3 percent of the sum of the taxpayer’s pro rata share or distributive share and guaranteed payments of qualified net income subject to the election made by an electing qualified entity. Attach the completed form FTB 3804-CR to the back of Form 540, 540NR, or Form 541 to claim the credit.

When to Pay the Elective Tax

The payment date must be within the following time frames:

-

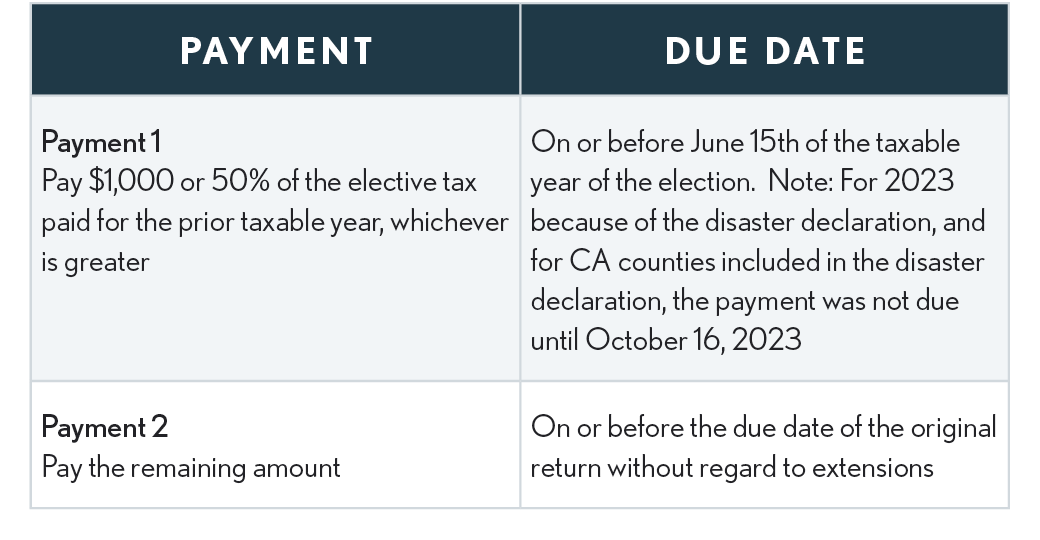

2021 taxable year - Pay the elective tax on or before the due date of the original tax return.

-

2022 to 2025 taxable years - Use the following table:

-

Taxable years 2026 through 2030 - SB 132, enacted 6/27/25, removes the requirement that the electing entity make the specified payment by June 15. The bill also reduces the credit allowed to a taxpayer against personal income tax if the electing entity does not make a payment by June 15, or makes a payment that is less than the required amount. The credit is reduced by 12.5%.

Caution

Beginning on or after January 1, 2022, and before January 1, 2026, the PTE may not make an election if the initial payment is not made by June 15.

Electronic Payment May Be Mandatory

S corporations and LLCs taxed as S corps, but not partnerships, are subject to mandatory electronic payment of tax for all future payments once the total tax reported on the state return exceeds $80,000. This would include future estimated tax payments and the June 15th PTE payment.

What Happens if the Payment is Incorrectly Applied?

If the entity incorrectly identified the PTET payment as an estimated tax payment, a request can be made to the FTB to correct the error. The request should be made before the return is filed, and must be made in writing and include an acknowledgment that reapplying the erroneous payment may cause penalties and interest for the tax year for which the payment was originally credited.

Taxpayers can make the request through a MyFTB account, while tax professionals can contact the Tax Practitioner Hotline and speak with a representative to adjust the payment, although a written request will still be required.

This procedure does not apply to an individual owner’s estimated tax payment; FTB will only move an entity’s misdirected estimated payment.

FTB FAQs about the PTE payment and credit can be found at: https://www.ftb.ca.gov/file/business/credits/pass-through-entity-elective-tax/help.html

Other State Tax Credit (OSTC)

Governor Newsom signed SB 851 on Sept. 29, 2022, which includes a remedy to the “net tax” issue when claiming the “Other State Tax Credit” and also claiming the Passthrough Entity Elective (PTE) Tax, effective for years beginning on or after January 1, 2022.

SB 851 increases the amount of the California “net tax” used to calculate the OSTC by the amount of the Passthrough Entity Elective Tax Credit claimed, thereby allowing taxpayers who claim both credits to receive the full amount of the OSTC they would have claimed if they had not claimed the Passthrough Entity Elective Tax Credit.

IRS Notice 2020-75

(Nov. 9, 2020) The IRS announced they will propose regulations that will clarify that state and local income taxes imposed on and paid by a partnership or S corporation on its income are allowed as a deduction by the partnership or S corporation in computing its non-separately stated taxable income or loss for the year of payment.

Thus, these taxes paid are not subject to the SALT deduction limitation for partners and shareholders who itemize deduction on their individual returns.