Proving Losses

Taxpayers will need to show evidence of the cost of the lost property, evidence of the event causing the loss, and evidence of the amount of the loss. It is helpful to have photos of the property before and after the casualty, notes describing the disaster and the property damaged, appraisals, and news clips describing the event. Blue Book values can be helpful in disaster losses that involve vehicles.

A qualified appraiser should be used to determine FMV of real property and scheduled personal property. The appraisal should cite values just before and after the disaster. In a disaster, it may be difficult to get an appraiser to “commit” to FMV until prices stabilize. Absent an appraisal, a possible alternative may be to get the written opinion of a real estate broker.

The question how to value trees, plants, etc., often comes up in disaster situations. For example, to value a mature tree, appraisers will often use historical data and estimate the overall loss of FMV in the property. A landscape firm could perhaps determine the cost of bringing landscaping back to its original state--this is a case where cost of repair work may be a good indicator of the amount of loss.

Use of Estimates of Repairs

Where the taxpayer relies on the cost of repairs, and not a competent appraisal, to measure the amount of a disaster loss, the repairs and associated expenditures must actually be made (Abrams, Paul, (1981) TC Memo 1981-231). Thus, a taxpayer couldn't use the estimated costs of repairs where no repairs were in fact made (Farber, Jack, (1972) 57 TC 714) or where taxpayer did part of the repair work himself and had a contractor do some of the work (Wheeler, Elvin, (1984) TC Memo 198442). If the taxpayer doesn't intend to have the repairs done, he should get a competent appraisal of the property which shows the decline in the value of the property because of the disaster. However, see “Safe harbor methods” below for situations where estimates of repairs will suffice.

But, where a taxpayer uses a competent appraiser to establish the decrease in fair market value of the property resulting from the disaster, the appraiser is entitled to consider the probable costs of repairing the damaged property, even though the repairs to the property are not, in fact, ever actually made. In computing the probable cost of repairs, however, the cost of repair immediately after the disaster is the relevant figure.

-

Safe Harbor Methods – The IRS recognizes that taxpayers often have difficulty determining disaster losses based on the decline in fair market value which has frequently resulted in time consuming and expensive litigation. So, to provide certainty to both taxpayers and the IRS, in Rev Proc 2018-08, effective December 13, 2017, the IRS provides safe harbor methods, that a taxpayer may choose to use in determining the decrease in FMV of personal-use residential real property (which we sometimes shorten to “residence” in this discussion) and for personal belongings in lieu of the actual reduction in FMV.

Caution

Rev. Proc. 2018-8 can be quite misleading. The “purpose,” part of the Rev. Proc. leads the reader to believe that the Rev. Proc. provides an alternate and more taxpayer beneficial way of determining a disaster loss. The problem is the purpose of the Rev. Proc. is to provide safe harbors to determine fair market value of a property for disaster loss purposes, NOT the disaster loss itself. A disaster loss is still the lesser of the adjusted cost basis or the fair market value on the date of the disaster reduced by any insurance reimbursement.

Definitions for This Purpose

-

Personal-use residential real property – is real property, including improvements (such as buildings and ornamental trees and shrubbery), that is owned by the individual who suffered a disaster loss and that contains at least one personal residence, which can be a single-family residence, or a single unit within a contiguous group of attached residential units (for example, a townhouse or duplex), and any structures attached to the residence or single unit. Ineligible property includes:

-

a condominium unit or cooperative unit,

-

mobile home or trailer,

-

property of which the taxpayer owns a fractional interest or no interest in the structural components, and

-

a personal residence where part is used as rental property or a home office used in a trade or business or transaction entered into for profit.

-

-

Personal belonging - is an item of tangible personal property that is owned by the individual who suffered a disaster loss and that is not used in a trade or business or in a transaction entered into for profit, and does not include a boat, aircraft, mobile home, trailer, or vehicle, or an antique or other asset that maintains or increases its value over time.

-

No-cost repairs – these are repairs made for a de minimis or token cost, donation, or gratuity, such as the repair or rebuilding of an individual’s residence by volunteers.

Estimated Repair Cost Safe Harbor Method for Residence Disaster Losses of $20,000 or Less

To determine the decrease in the FMV of the personal-use residential real property, the lesser of two repair estimates prepared by two separate and independent contractors, licensed or registered in accordance with state or local regulations, may be used, provided the costs to restore the residence to pre-casualty condition are itemized. Costs that improve or increase the value of the residence above pre-disaster value must be excluded from the estimate. This safe harbor only applies if the loss is $20,000 or less before applying the per-disaster and percentage of AGI reductions.

De Minimis Safe Harbor Method for Residence Disaster Losses of $5,000 or Less

Under the de minimis method, the cost of repairs required to restore the residence to pre-disaster condition may be estimated by the taxpayer. Costs that improve or increase the value of the residence above pre-disaster value must be excluded from the estimate. The estimate must be done in good faith, and the individual must maintain records detailing the methodology used for estimating the loss. This safe harbor only applies if the loss is $5,000 or less before applying the per-disaster and percentage of AGI reductions.

Insurance Safe Harbor Method for Residence Disaster

To determine the FMV decrease of the individual’s residence, the estimated loss determined in reports prepared by the individual’s homeowners’ or flood insurance company may be used.

Contractor Safe Harbor Method (Federally Declared Disasters Only)

The contract price for the repairs specified in a contract prepared by an independent and licensed contractor (or one registered in accordance with state or local regulations) may be used if the contract itemizes the costs to restore the residence to the condition existing prior to the disaster. Costs that improve or increase the value of the residence above pre- disaster value must be excluded from the contract price for purposes of this safe harbor. To use the Contractor Safe Harbor Method, the contract must be a binding contract signed by the individual and the contractor.

Disaster Loan Appraisal Safe Harbor Method (Federally Declared Disasters Only)

Under this method, to determine the decrease in FMV of the individual’s residence, an appraisal prepared for the purpose of obtaining a loan of Federal funds or a loan guarantee from the Federal Government may be used. The appraisal should include the estimated loss the individual sustained as a result of the damage to or destruction of their residence from the Federally declared disaster.

De Minimis Safe Harbor Method for Casualties or Thefts of $5,000 or Less of Personal Belongings

The rev proc allows an individual to make a good faith estimate of the decrease in the FMV of the individual’s personal belongings, provided the individual maintains records describing the personal belongings affected and detailing the methodology used for estimating the loss. This safe harbor only applies if the loss is $5,000 or less before applying the per-disaster and percentage of AGI reductions.

Replacement Cost Safe Harbor Method for Personal Belongings in Federally Declared Disasters

This method may be used to determine FMV of most personal belongings located in a disaster area immediately before the disaster to compute the disaster loss. If used, this method must be applied to all eligible personal belongings for which a disaster loss is claimed. This method may not be used for the following: boats, aircraft, mobile homes, trailers, vehicles, and antiques or other assets that maintain or increase in value over time.

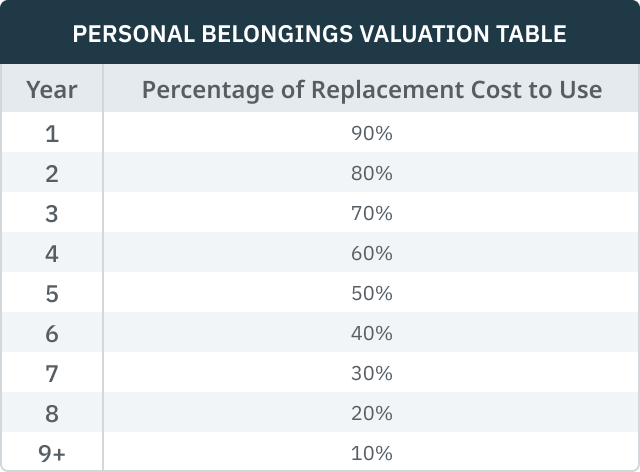

Under this method, first determine the current cost to replace the personal belonging with a new one and reduce that amount by 10% for each year the personal belonging was owned, using the percentages in the Personal Belongings Valuation Table below. A personal belonging owned by the individual for nine or more years, will have a pre-disaster FMV of 10% of the current replacement cost.

Example: Joe’s uninsured furniture was destroyed in a disaster. He purchased his couch 4 years prior to the hurricane for $800. It would cost $1,100 to replace it. Using the replacement cost safe harbor method, the fair market value of the couch just before the storm would be $660 ($1,100 x 60%). Since the couch was destroyed, its FMV after the disaster is $0, so the decrease in FMV is $660, which is less than his basis of $800. Therefore, Joe’s disaster loss for the couch is $660.

-

Effect of No-Cost Repairs

If any of the safe harbor methods provided in Rev Proc 2018-08 are used to determine the fair market value of or the amount of loss of an individual’s residence or personal belongings, the loss must be reduced by the value of any no-cost repairs.