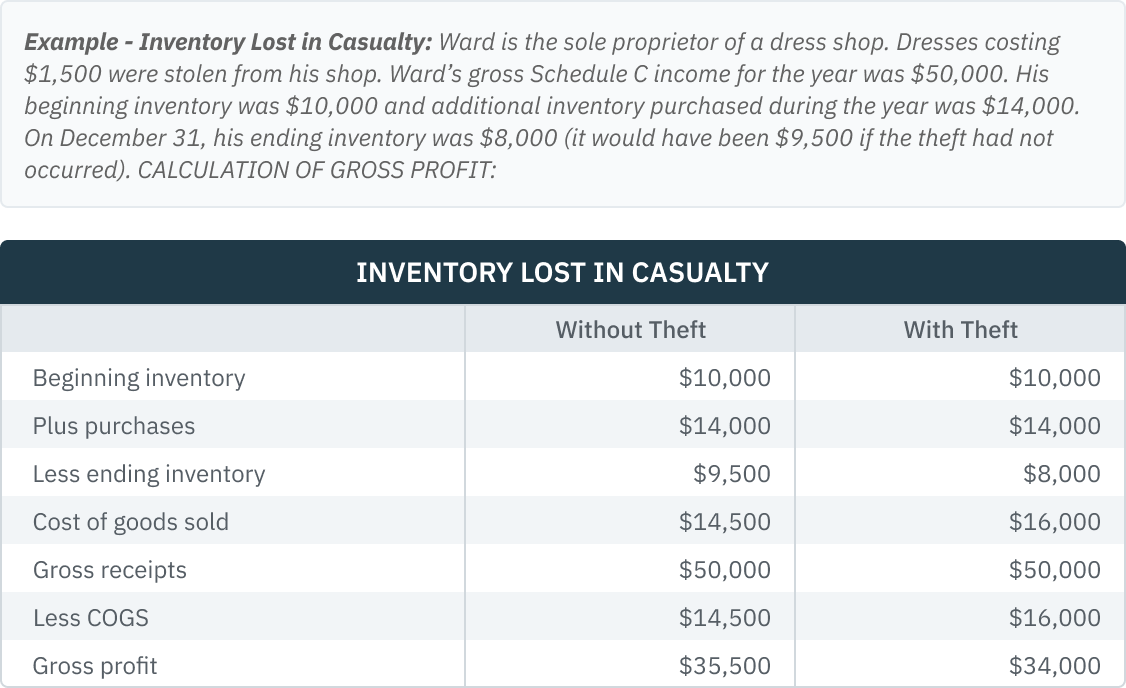

Inventory Losses

Theft and other types of inventory casualties are accounted for through the cost of goods sold. There is no separate casualty deduction when there is no reimbursement. If a taxpayer is reimbursed for lost inventory in the year of the loss, the taxpayer may include the reimbursement in income, and adjust the closing inventory accordingly.

Note - Inventory and Disaster Loss Election

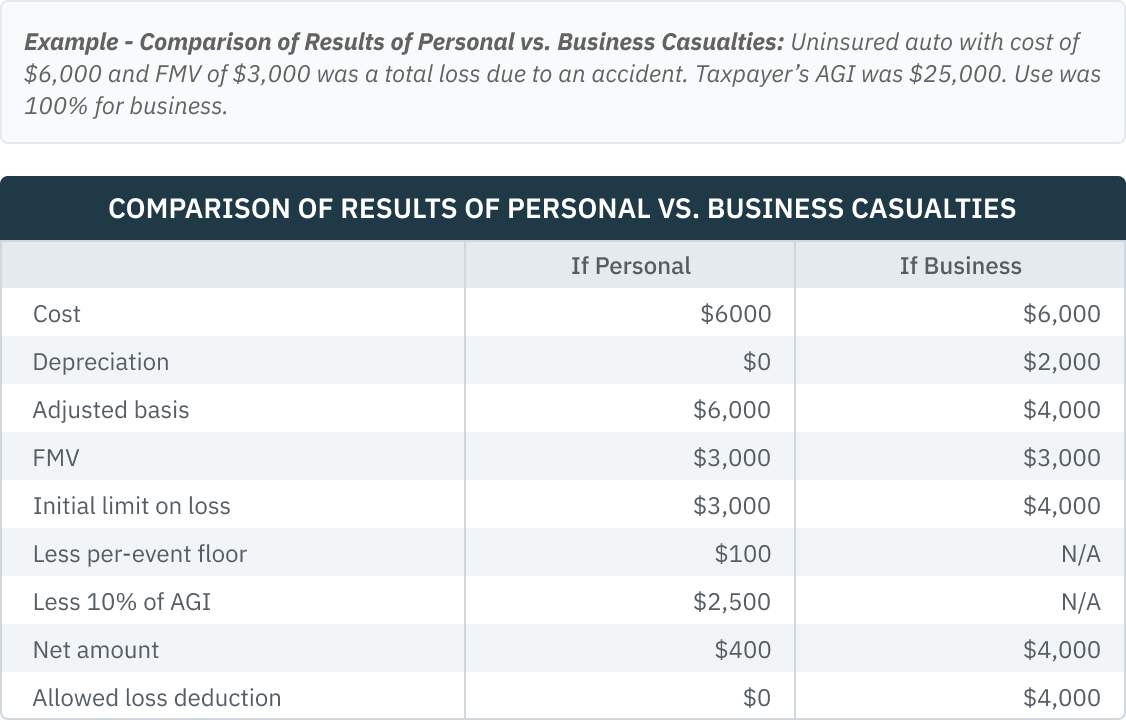

For income tax purposes, a taxpayer can elect to deduct a casualty loss sustained in an area the President declares to be a disaster area either in the year the loss is sustained or in the preceding year. If the loss is attributable to self-employment income, the deduction must be taken into account for self-employment tax purposes in the same year the taxpayer elects to deduct it for income tax purposes. Thus, where a self-employed individual incurred a casualty loss from damage to inventory in a disaster area and elected to deduct the loss in the previous year, the deduction must also be taken into account in the previous year in figuring the self-employment tax. (Rev Rul 77-94, 1977-1 CB 265)