Disaster Losses

Federally Declared Disaster

This is a disaster that occurred in an area declared by the President to be eligible for federal assistance under the Robert T. Stafford Disaster Relief and Emergency Assistance Act. A list of the designated areas is available on the Federal Emergency Management Agency (FEMA) web site: www.fema.gov. Taxpayers in these areas are eligible for special tax breaks as well as non-tax related assistance.

Taxpayer's Principal Residence

If a taxpayer's principal residence, or any of the residence's contents, is compulsorily or involuntarily converted because of a disaster:

-

Gain isn't recognized from the receipt of insurance proceeds for contents of the residence that was unscheduled personal property for insurance purposes.

-

Insurance proceeds for the residence or any of its contents other than unscheduled personal property are treated as if received for a single item of property. Property that is similar or related in service or use to the converted residence or its contents is treated as property similar or related in service or use to this single item of property.

The rules apply to a taxpayer's principal residence or any of its contents if it is located in a disaster area and is compulsorily or involuntarily converted as a result of a federally declared disaster. (Code Sec. 1033(h)(1))

Qualified Disaster Relief Payments

Certain “qualified disaster relief payments” received by an individual are excluded from gross income.

Disaster Losses in General

Special rules apply to losses which occur in areas the President of the United States declares eligible for Federal disaster assistance. The losses must result from the disaster. The FEMA web site noted above lists the designated disaster areas. Taxpayers may elect to claim the loss on the tax return for:

-

The year it occurs, or

-

The preceding year (either an original or amended return).

Disaster Losses Offer Special Options

When to take the loss depends upon a number of factors and should be carefully analyzed to determine which year is the most beneficial for the taxpayer. Some of the factors to consider include:

-

The tax brackets for each year – From purely a tax standpoint, each year should be carefully examined as to which will provide the greatest overall tax benefit and without wasting other tax benefits.

-

The need for immediate cash – The primary purpose of the special rules allowing the casualty loss to be claimed on the prior year’s return is to provide taxpayers access to a tax refund without the need to wait – often many months - to file their return for the year of the loss.

-

Self-employment tax – Self-employed taxpayers will also need to consider whether to take a business casualty loss that affects inventory in the current or prior year since the loss can offset self-employment tax as well as income taxes (also see “Note” in “Inventory Losses” section above).

-

Whether the loss will be used up – If the casualty loss is not fully used up in the year it is first deducted, it can create a net operating loss (NOL).

Making the Election to Claim the Disaster Loss on Preceding Year’s Return

The election must be made in writing no later than six months after the due date of the taxpayer’s federal income tax return for the disaster year, without regard to any extension of time to file ((Reg Sec. 1.165-11T(f)); Rev Proc 2016-53).

Example: A Federally declared disaster occurred in Year 2. A calendar-year taxpayer who incurred a loss in that disaster can claim their casualty loss on either their Year 2 return or their Year 1 return. If the prior year (Year 1) return has already been filed, it can be amended by filing a Form 1040X. Either the original or amended prior year return must be filed no later than 6 months after the original due date of the Year 2 return. Thus, the due date will usually be October 15 of Year 3.

-

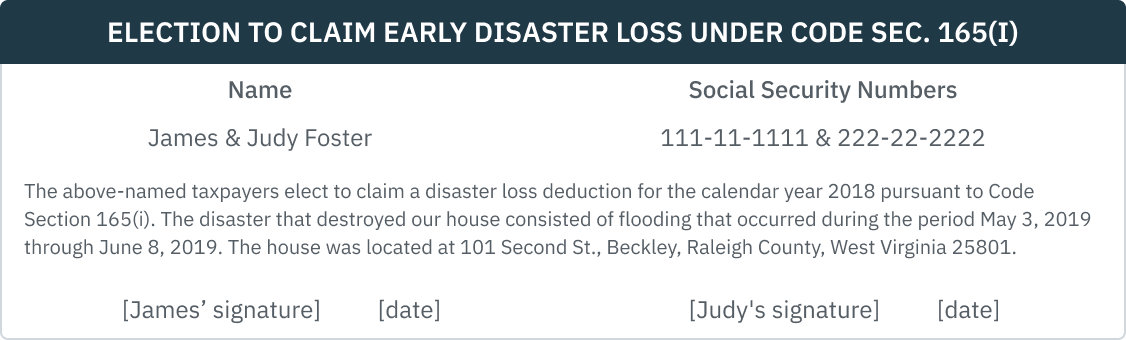

A taxpayer makes a Sec.165(i) election by deducting the disaster loss on either an original or amended federal tax return for the preceding year. An election statement indicating the taxpayer is making a Sec.165(i) election must be included with the original or amended return. The election statement must contain the following information:

-

The name or a description of the disaster and date or dates of the disaster which gave rise to the loss.

-

The address, including the city, town, county, parish, State, and zip code, where the damaged or destroyed property was located at the time of the disaster.

For an election made on an original federal tax return, a taxpayer must provide the above information on Lines 1 or 19 (as applicable) of Form 4684. A taxpayer filing an original return electronically may attach a statement as a PDF document if there is insufficient space on Lines 1 or 19 of the Form 4684 to provide the required information. For an election made on an amended return, a taxpayer may provide the information required by any reasonable means, such as writing the name or a description of the disaster, the State in which the damaged or destroyed property was located at the time of the disaster, and “Section 165(i) Election” on the top of the Form 4684 and providing the rest of the information as required in (1) and (2) above in either the Explanation of Changes on Form 1040X, or directly on the Form 4684, attaching a statement if there is insufficient room on the form. A sample of a disaster loss election follows:

When completing Form 4684 (2021), and the casualty or theft loss is attributable to a federally declared disaster, above line 1 check the box and enter the associated FEMA disaster declaration number, which can be found at https://www.fema.gov/Disasters.

Revoking the Election

The election can be revoked up to ninety (90) days after the due date for making the election.