California Differences - Earned Income Tax Credit

California initiated a refundable EITC in 2015. California and at least 29 other states plus the District of Columbia now offer an EITC. In the majority of these states, the credit is refundable. Most states set their EITC as a portion of the federal EITC, and most states conform to the federal EITC program in other aspects such as eligibility requirements and income levels.

The California EITC will only apply for taxable years for which an adjustment factor (see below) is specified in the state’s annual Budget Act and if the Budget Act authorizes resources for the Franchise Tax Board (FTB) to oversee and audit returns associated with the EITC. From 2015 through 2024, the legislature has included an adjustment factor in the annual budget bill.

Medicaid Waiver/IHSS Payments Are Earned Income for EITC

In step with the federal court ruling in the Feigh case, the Office of Tax Appeals (OTA) ruled, in a precedential decision, that the wages paid to an In-Home Supportive Service (IHSS) worker for providing care to someone they lived with is earned income for purposes of the California EITC, even though the wages are excluded from income. The OTA reached this decision in spite of no California income tax having been withheld on the wages. (Appeal of F Akhtar and M Akhtar, 2021-OTA-118P, May 5, 2021) Eligible taxpayers may file amended returns for all open years to claim a refund of EITC. For more information on filing for refunds, go the FTB web site and in the search, box enter "In-home Supportive Services".

California SSN Requirement

AB 93, signed by the governor June 29, 2020, and effective for 2020 and future returns, allows the EITC when eligible individuals, their spouses (if married) and any qualifying children have an SSN (without regard to whether it was issued for employment or issued solely for the purpose of receiving federally funded benefits), or a federal ITIN if there is a qualifying child under age 6. This provision was modified by AB 1876, signed into law September 18, 2020, removes the requirement for an ITIN tax filer to have at least one child under the age of six to qualify for the California EITC.

If an ITIN is used, eligible individuals should provide identifying documents upon request of the FTB. These are:

-

Identifying documents acceptable for purposes of obtaining a California driver’s license or identification card as authorized by the California Vehicle Code and related regulations for purposes of establishing documents acceptable to prove identity.

-

Identifying documents used to report earned income for the taxable year.

By expanding the eligibility for the California EITC, the bill also expands eligibility for the Young Child Tax Credit (YCTC) by allowing a “qualified taxpayer” and “qualifying child” to have either an SSN or federal ITIN.

The California EITC will generally follow the eligibility requirements of the federal EITC (but legislation would be required to conform to changes made by recent federal law changes). Additionally, the earned income limitations for the California EITC (the amount where the CA EITC will be fully phased-out) will be lower than those for the federal EITC.

Prior to tax year 2017, California limited the EITC to wage earners only. This limitation was lifted and therefore self-employment income is also treated as earned income. Domestic workers whose income is not subject to withholding are also eligible.

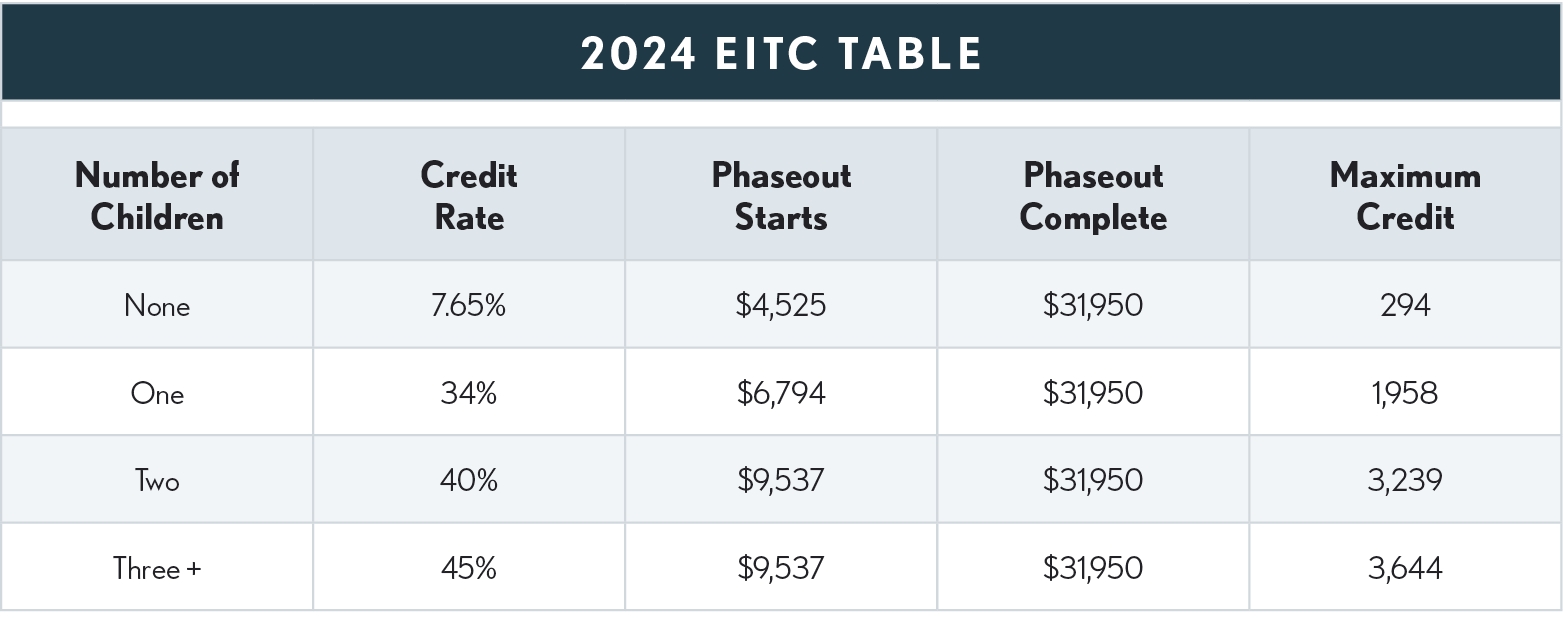

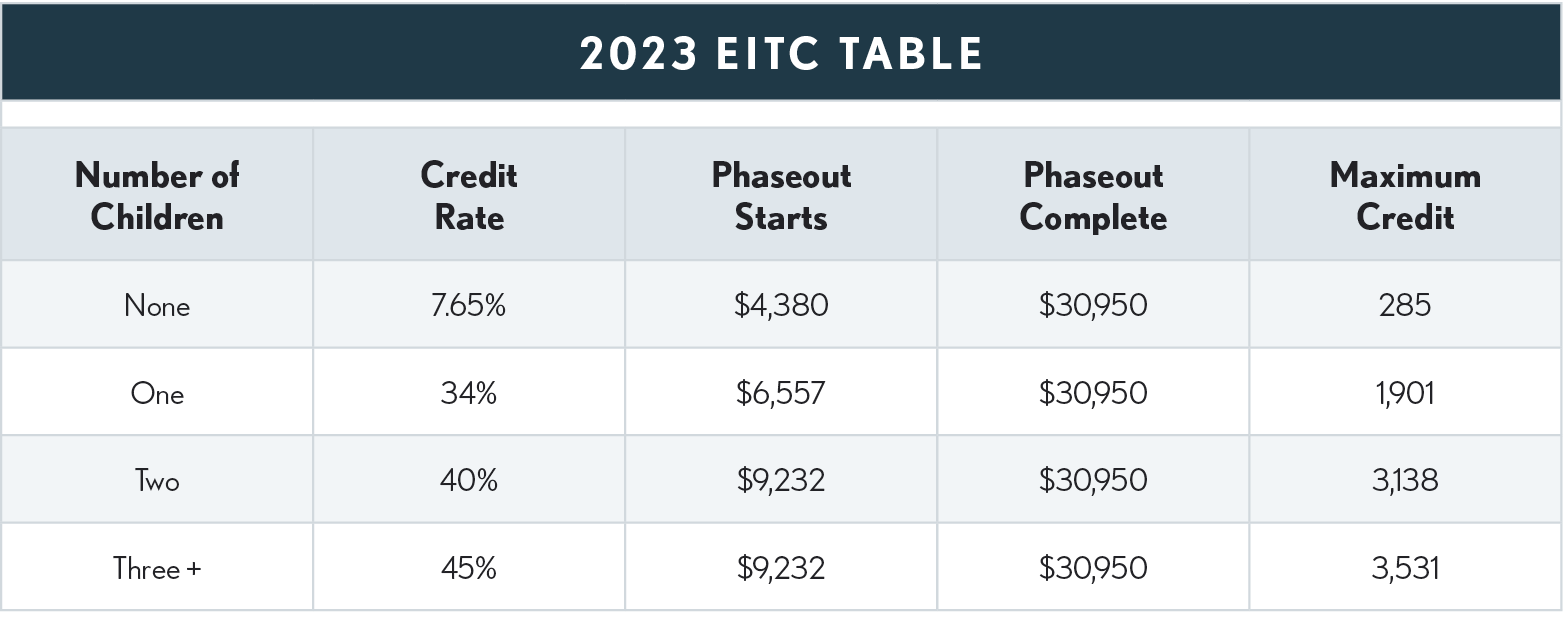

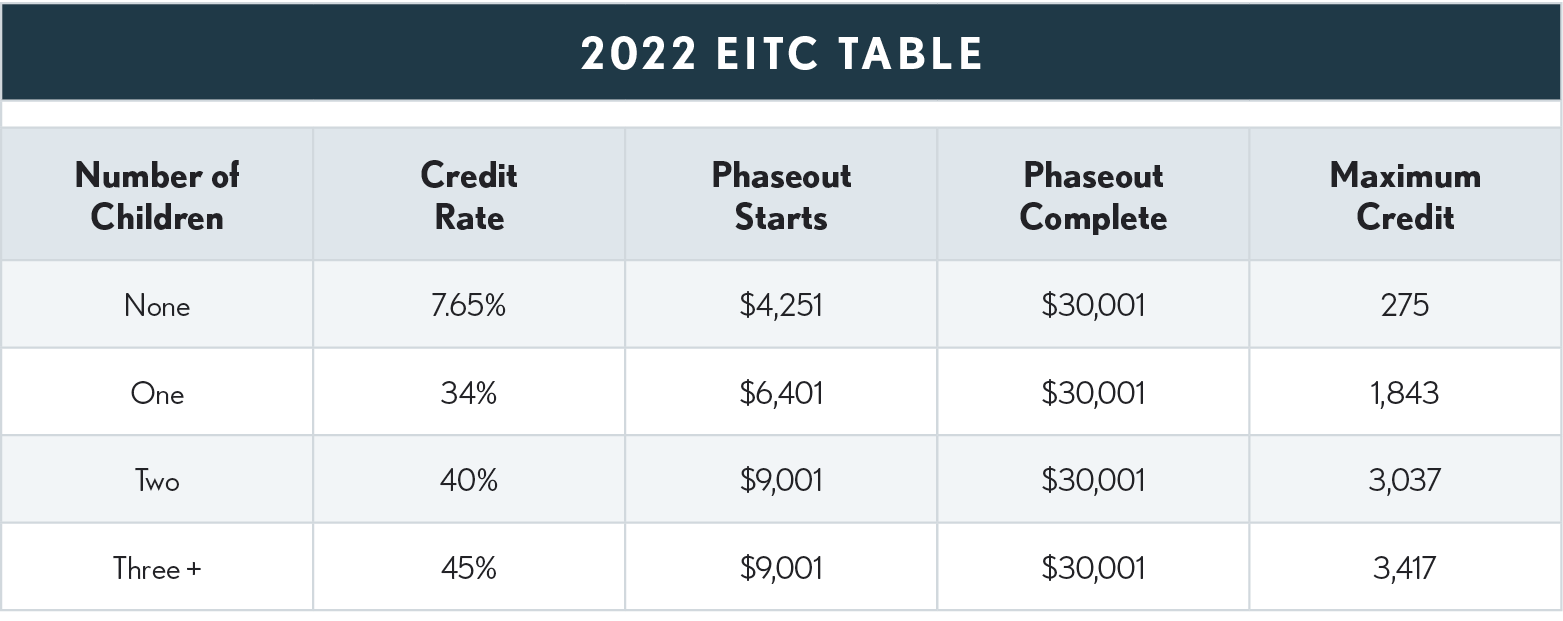

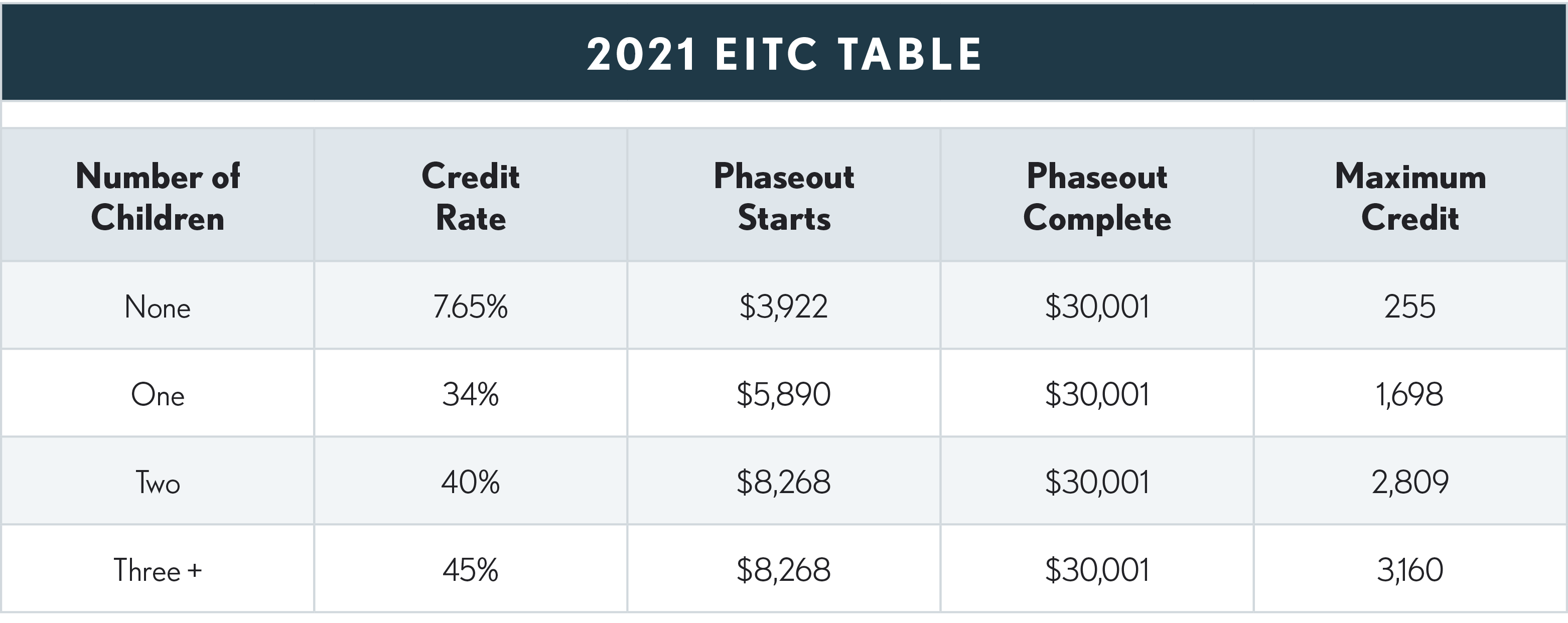

Annual Adjustment Factor - CA has built a factor into its computation that permits the state to limit the CA credit while still following the federal computation. For 2015 through 2024, that factor is 85%. Thus, a tentative credit is computed in the same fashion as the federal and then that amount is multiplied by the factor to determine the actual credit awarded. The EITC adjustment factor is set by the legislature in the annual Budget Act.

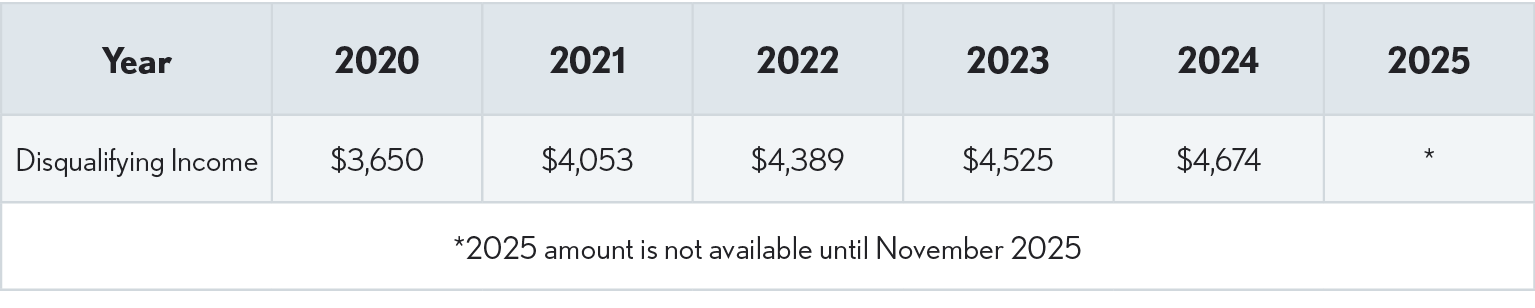

Disqualifying Income

The credit isn't available to individuals when their “disqualified income” (i.e., investment income) is more than the amount in the table.

Eligible Individual Age Requirement

An individual (or if married, either the individual or their spouse) who does not have a qualifying child will be eligible for the California EITC if age 18 or older at the end of the tax year. (R&TC § 17052(c)(2), as amended by SB 855).

If a taxpayer’s earned income is $30,000 (adjusted for income) or more, the phaseout will reduce the California EITC to zero. (AB 91, signed by the governor 6/27/2019) See tables for year-specific phaseout amounts.