Due Diligence Requirements

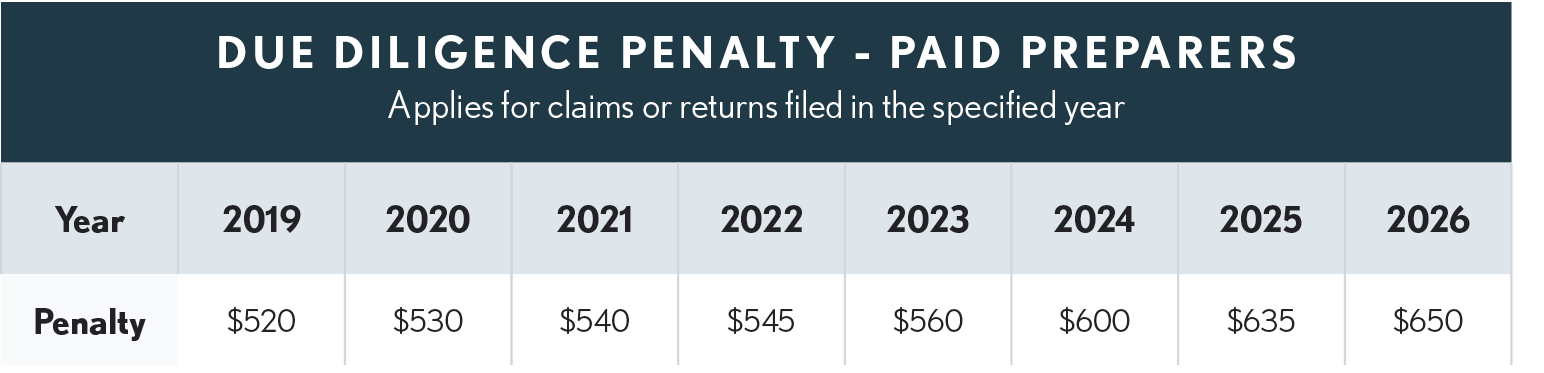

Beginning with 2016 tax returns, the PATH Act of 2015 (Act Sec 207) adds the child tax credit to the paid preparer due diligence requirements that apply to the EITC, including a due diligence penalty, indexed for inflation as shown in the table below. Form 8867 provides a 2-page due diligence checklist for EITC, AOTC and Child Tax Credit (including the Additional Child Tax Credit and the Other Dependents Credit) and the head of household filing status and must be completed by the paid preparer if the taxpayer claims any one of the credits or the taxpayer files as head of household. Form 8867 must be filed with the taxpayer’s return. Of importance here is understanding that the penalty applies to each credit and the H of H status, so if for a 2024 return filed in 2025 the taxpayer claims all three credits and H of H and the preparer has not met the due diligence requirements, the preparer’s penalty could be as high as $2,540.

Specific questions on Form 8867 relating to the child, additional child, and other dependents credit that the preparer needs to answer are whether the preparer:

-

Determined that each qualifying person for these credits is the taxpayer’s dependent who is a citizen, national or resident of the U.S. (yes or no)

-

Explained to the taxpayer that the credit may not be claimed if the taxpayer didn’t live with the child for over half the year, even if the taxpayer supported the child, unless the custodial parent released their claim to the child’s exemption. (Yes, no or not applicable)

-

Explained to the taxpayer the rules about claiming the credit for a child of divorced or separated parents, or parents who live apart, including the requirements to attach Form 8332 or similar statement to the return. (Yes, no or not applicable)