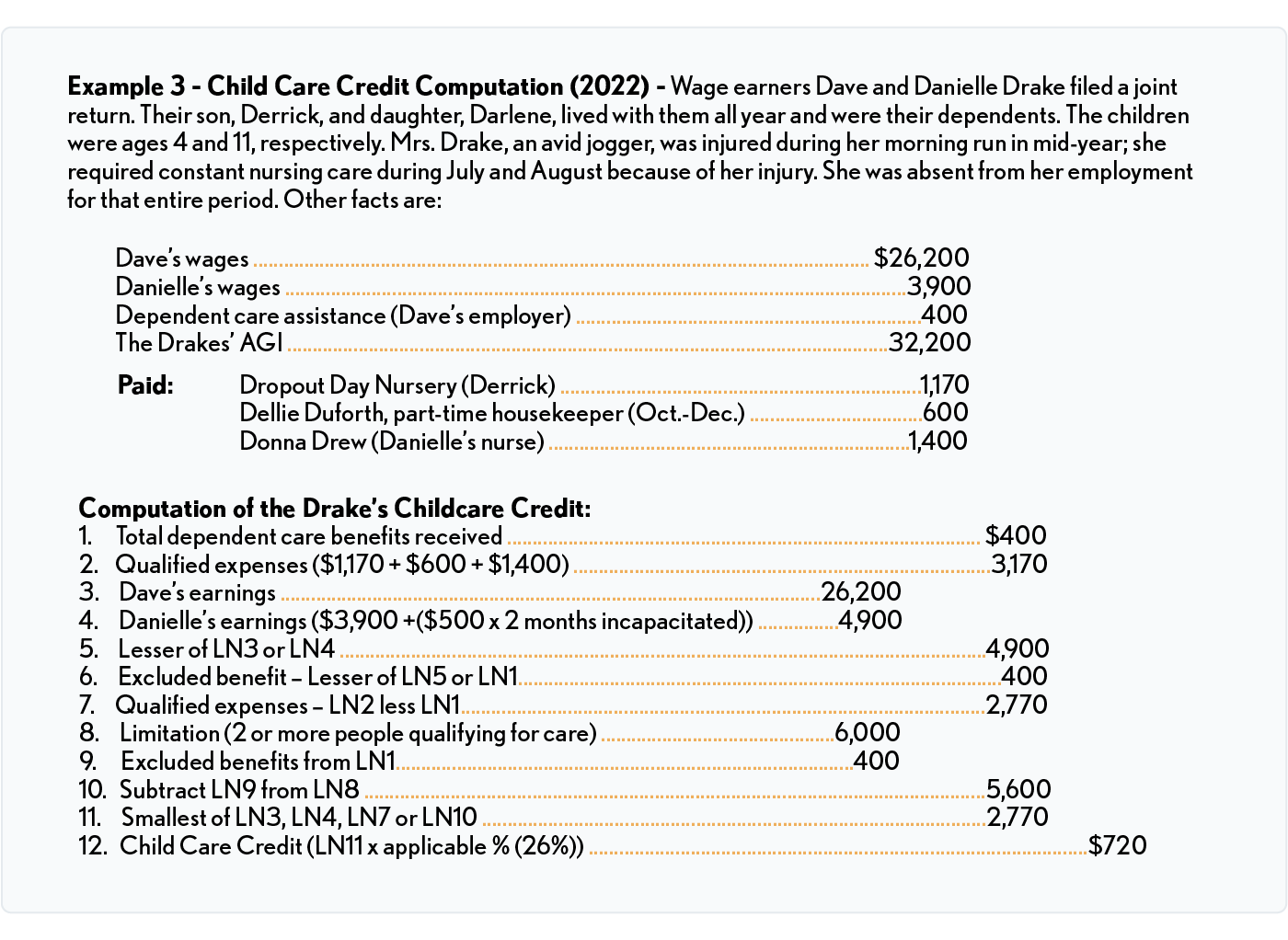

Strategy - Excess Contributions to Dependent Care Assistance Plan

Employers may have a Sec 129 dependent care assistance plan. If they do, up to $5,000 of the employee’s wages can be set aside to pay child and dependent care expenses. Those benefits will appear in box 10 of the employee’s W-2. The amount is not included in box 1 as wages nor is it included in box 3 Social Security wages and Box 5 Medicare wages.

For married couples, if both spouses’ employers have a Sec 129 plan, the spouses can each contribute $5,000 to their respective plan. Thus, the couple shields $10,000 from Social Security and Medicare taxes withholding.

However, regardless of marital status the maximum that can be claimed on the Form 2441 is $5,000 and any amount more than the actual expenses must be included on line 1e of the 1040 or 1040-SR. Thus, any excess will have escaped the Social Security and Medicare taxes but will still be subject to income tax.

Example 2: Joe and Susan both are employed in 2025 by firms that have a Sec 129 dependent care benefits plan. They both contribute the maximum $5,000 to their plan. They have $6,000 of actual childcare expenses for the year. They both use the same expenses to apply for reimbursement from their respective dependent care benefits plans. When they complete Form 2441, they will end up with $4,000 of excess dependent care benefits which must be included in income on line 1e of their 1040. So, the $4,000 escaped being subject to the 6.2% Social Security withholding and 1.45% Medicare tax withholding. Thus, they saved $306 ($4,000 x (.062 + .0145).

-

As an aside, the employer saves on payroll taxes as well because the employer also avoids the Social Security and Medicare taxes on the amount contributed to the Sec 129 plan.

Other Plan Requirements

A dependent care assistance plan must meet various requirements to be effective:

-

No more than 25% of the assistance the plan provides during the year may be paid on behalf of owners (Including spouses and dependents) of more than 5% interest in the employer’s business.

-

Employers must inform eligible employees about the availability of the plan.

-

Employees must receive a written statement of benefits they received during the year – usually provided on Form W-2.

-

The program cannot discriminate in favor of “highly-compensated” employees or their dependents.

W-2 Reporting of Dependent Care Exclusion Amounts

Form W-2, Box 10 shows the amount of dependent care benefits paid by the employer. The amount should not be included in Box 1 (Wages).