Credit Amount

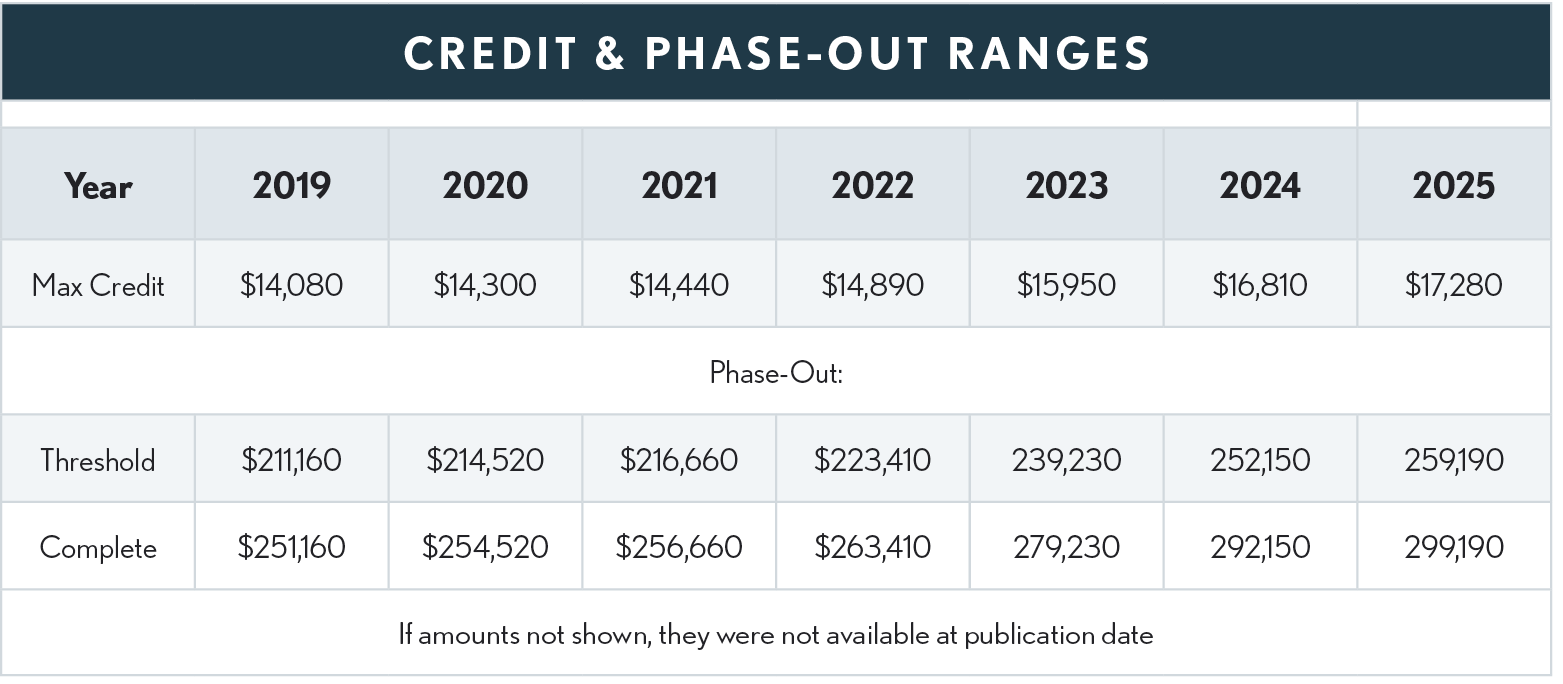

An individual is allowed an income tax credit for qualified adoption expenses. (Code Sec. 23(a)(1)) The total expenses that can be taken as a credit for all tax years with respect to an adoption of a child is an annually inflation adjusted amount as illustrated in the table below.

Special Needs Child

In the case of an adoption of a child with special needs, the full credit limit will be allowed for the tax year in which the adoption becomes final, regardless of whether the taxpayer has qualified adoption expenses. (Code Sec.23(a)(3)). In the case of a taxpayer adopting a U.S. child with special needs, the taxpayer may be able to exclude up to $16,810 (2024) and claim a credit for additional expenses up to $18,810 (minus any qualified adoption expenses claimed for the same child in a prior year). The exclusion may be available, even if the taxpayer or the taxpayer’s employer didn't pay any qualified adoption expenses, provided the employer has a written qualified adoption assistance program (for further details and the definition of a special needs child, see the instructions for Form 8839).