Residence Used as Day Care Facility

It is not uncommon for day care owners to provide childcare in their own homes. When these individuals use their homes as their workplaces, special IRS tax rules can apply. Find details in this TaxBuzz Guide.

Day care facilities are not subject to the exclusive use requirement that applies to other home offices, but the exception to that requirement applies only if the owner or the operator:

-

Has applied for (and the application has not been rejected) a license, certification, registration or approval as a day care center or as a family or group care home under the provisions of any applicable state law, or

-

Has been granted (and the grant has not been revoked) a license, certification, registration or approval as a day care center or as a family or group day care home under the provisions of any applicable state law, or

-

Is exempt from having a license, certification, registration or approval as a day care center or as a family or group day care home under the provisions of any applicable state law. (Code Sec. 280A(c)(4)(B))

The day care facility exception does not apply where the services performed are primarily educational or instructional in nature (e.g., musical instruction). However, the exception does apply if the services are primarily custodial, and the educational, development or enrichment activities are only incidental to the custodial services. The determination depends generally on the facts and circumstances of each particular case. (S Rept No. 3340 (PL 95-30) p. 7) The services must be provided for individuals age 65 or older, children, or individuals who are physically or mentally incapable of caring for themselves.

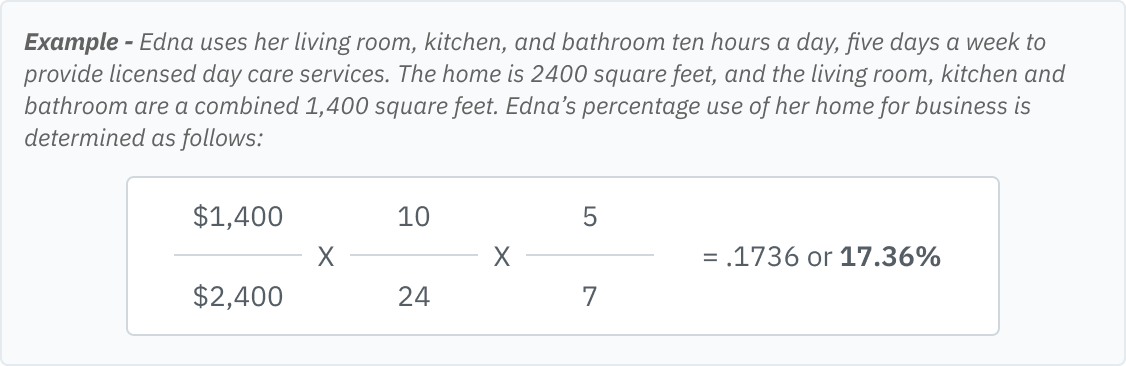

When calculating the percentage of business use of the home, both the space used to operate the day care business and the amount of time that the space is used to provide day care – including preparation and cleaning time – are factors. (Rev. Rul. 92-3; Neilson v. Commissioner, Dec 46,301, 94 TC 1)