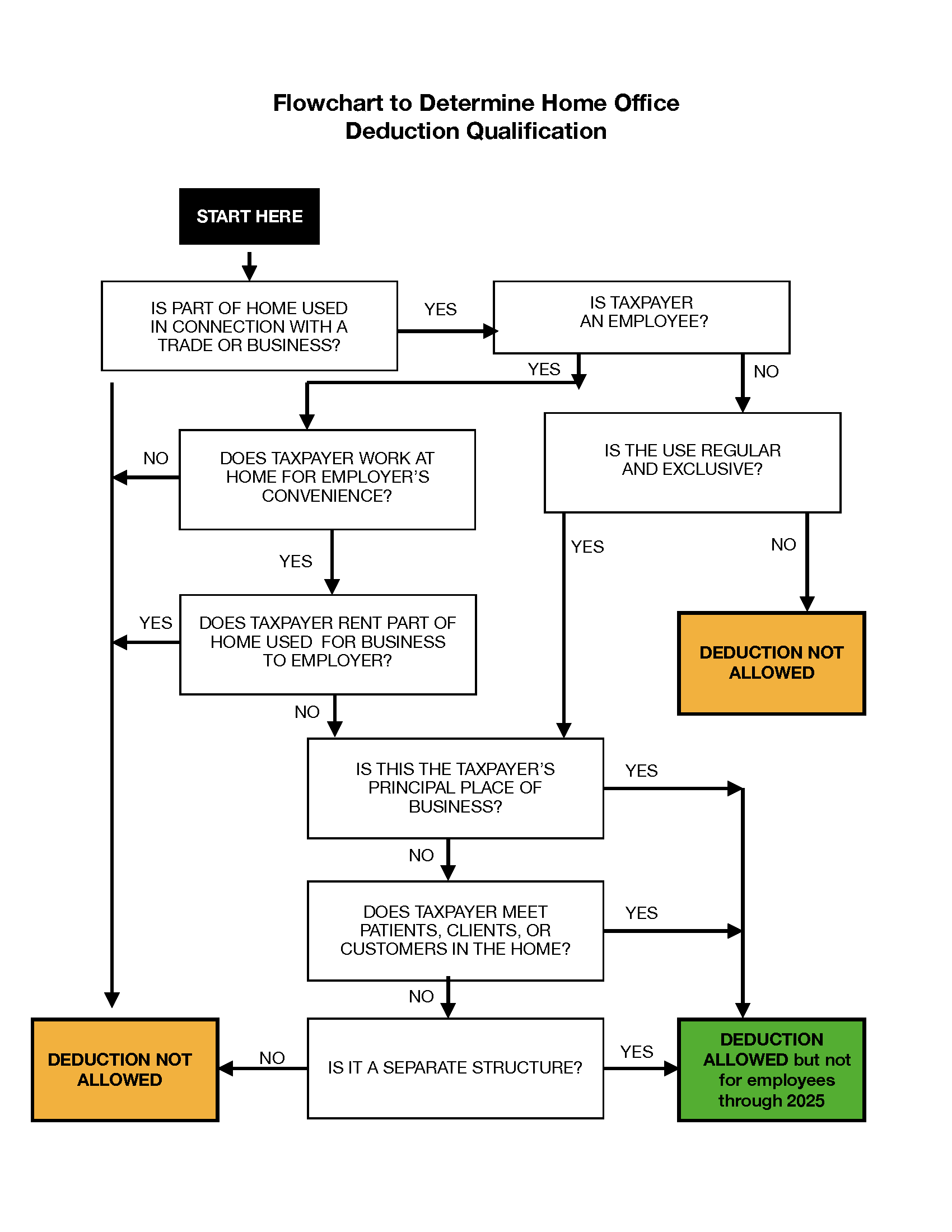

Office-In-Home Tax Deduction Qualification Tests

In order to deduct expenses, remote workers must meet specific office-in-home qualification tests. A complete list of criteria can be found below:

1.The office area must be used exclusively in a taxpayer’s trade or business on a regular, continuing basis. Taxpayer must be able to provide sufficient evidence to show the use is regular. Exclusive use means there can be no personal use (other than de minimis) at any time during the tax year. Use of only a portion of a room is acceptable as long as the taxpayer shows that section is totally for business.

2.One of the following must also apply. The home office must be:

a. Used for storing inventory for a wholesale or retail business for which the taxpayer’s home is the only fixed location of the business. Use of the area need not be exclusive under this test, but it must be regularly used;

i. Since the space is used to store inventory, cost of storage space for books, files or equipment can’t be deducted unless the taxpayer qualifies under one of the other tests.

ii. Storage of “product samples” can also produce a home office deduction.

b. Used as a licensed day care center (another exception to the exclusive-use test);

c. A separate structure not attached to the taxpayer’s home but used for business;

d. A place where the taxpayer meets with customers, patients, or clients (just telephone contact with clients isn’t enough to meet this test); or

e. The principal place of business for any trade or business of the taxpayer (see definition below). Also see following Ninth Circuit ruling:

Musician's long hours of practice yield home office deductions - The Ninth Circuit has reversed the Tax Court and held that a professional musician could claim home office deductions under the Supreme Court's Soliman test.

The determining factor was her long hours of practice at home, because the “relative importance” test yielded no definitive answer to whether she used a room in her home as her principal place of business under Code Sec. 280A. (Popov, (CA9 4/17/2001) 87 AFTR 2d ¶2001-804)

Application to Current Law

A home office is used as a principal place of business under Code Sec. 280A(c)(1) if a portion of the home is used for the administrative or management activities of any trade or business of the taxpayer, but only if there is no other fixed location where the taxpayer conducts substantial administrative or management activities of that trade or business. Examples of administrative or management activities include billing customers, keeping books and records, and setting up appointments.

Under the Ninth Circuit's approach, musicians who may not be able to satisfy the statutory test (e.g., their agent handles all booking and billing details) may be able to use their long hours of practice at home to support a home office deduction under the Soliman principal-place-of-business test.