Gross Income Limits For Business Use of a Home

The IRS dictates specific gross income limits for the business use of a home tax deduction. These are outlined in the paragraphs and table below.

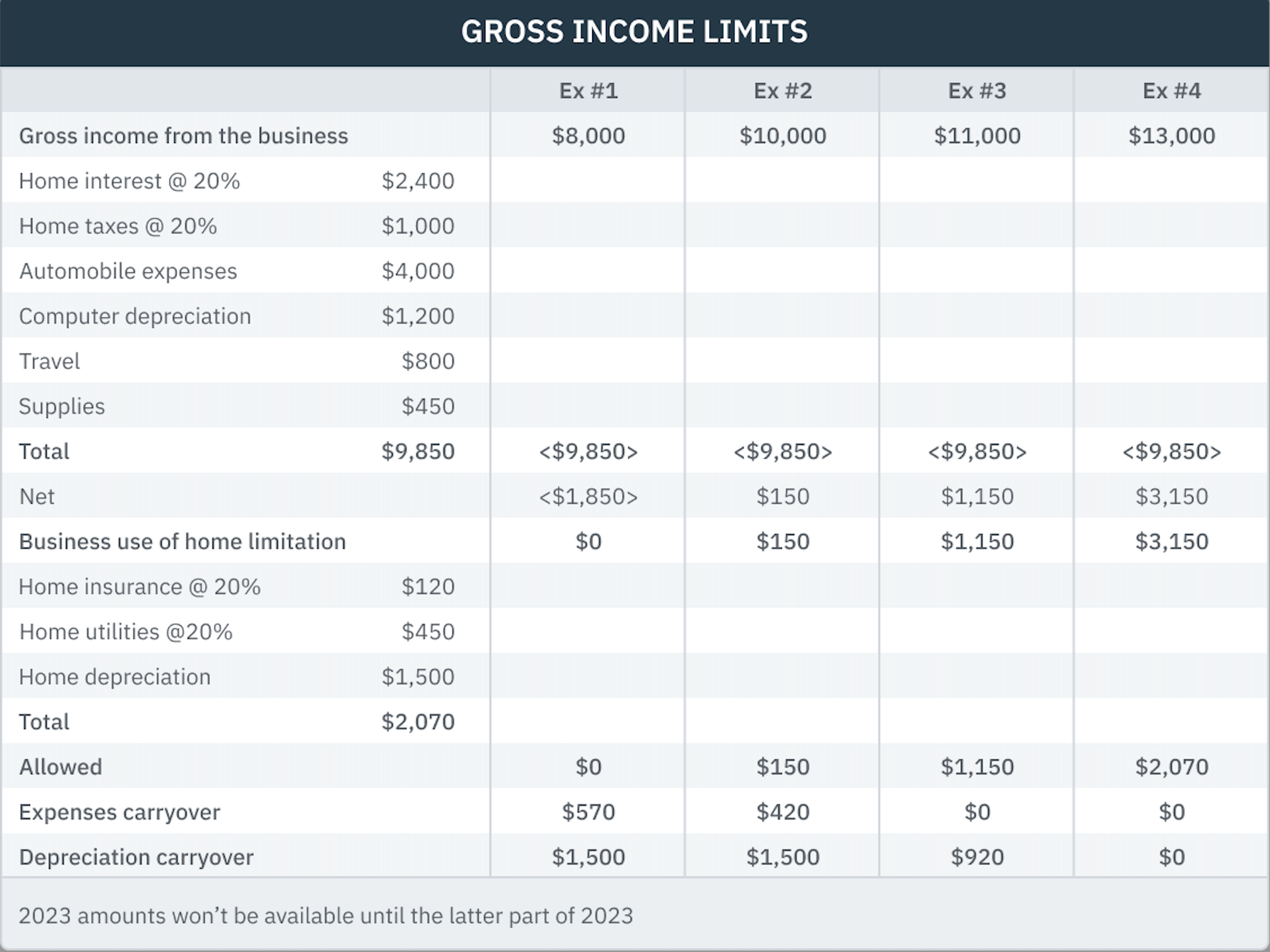

The deduction for the business use of a home is subject to the gross income limit from the business. However, home mortgage interest, property taxes and casualty losses (disaster losses 2018-2025) are always deductible, if the taxpayer itemizes deductions, whether or not the taxpayer claims a deduction for the business use of the home (Sec 280A(b)). Therefore, the prorated deduction for these expenses will always be allowed and is not subject to the gross income test. However, mortgage interest, taxes and casualty (disaster) losses are used in the computation to determine whether the other expenses of the home’s use and depreciation are deductible as illustrated in the four examples that follow.

Assume the taxpayer uses his home 20% for business.

Caution

Under TCJA, all state and local taxes claimed as a Schedule A itemized deduction are limited to $10,000 for the years 2018 through 2025. The portion of the real property taxes used in the computation of the home office is unaffected by that limitation, i.e., the full amount of property taxes paid is used to determine the portion of the property taxes used in the home office deduction. However, the line on Form 8829 where the real property taxes are deducted will vary, thus affecting the gross income limitation computation and carryover of expenses.