California Differences - Tax Exempt Entities

The following are some of the differences between federal and California rules for tax-exempt organizations:

Exemption Application

FTB Form 3500, Exemption Application, with all required documentation, is used to apply for exemption from corporate franchise or income tax. However, until the exemption is granted, the organization remains taxable and the requirement to file a state tax return continues. The FTB may require the organization to file exempt returns for the period of time the exemption is requested.

Just because the organization is exempt from federal income tax does not automatically exempt it from California tax. California may require the organization to obtain a federal exemption determination letter that establishes or shows its tax‑exempt status prior to issuing a state exemption determination letter. If the IRS revokes their federal tax‑exempt status, the organization must notify the FTB. The FTB will revoke the tax‑exempt status if the entity fails to meet certain state provisions governing exempt organizations. If an organization’s tax-exempt status is revoked or denied, the organization will need to file form FTB 3500 to reinstate its tax‑exempt status.

There is no filing fee when submitting Form 3500.

FTB Form 199

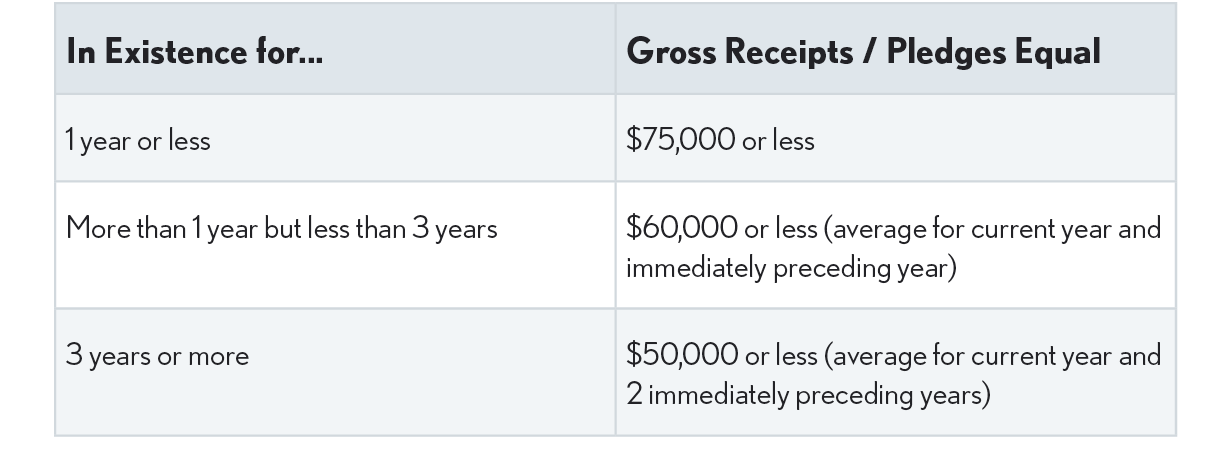

Most tax-exempt organizations are required to file Form FTB 199 or FTB 199N. Form 199 is used by organizations granted tax-exempt status by the FTB and nonexempt charitable trusts as described in IRC Section 4947(a)(1). There is no filing fee. The requirement to file Form 199 applies if the normal amount of total gross receipts and pledges of the organization is more than $50,000, the entity is a private foundation (regardless of gross receipts), or is a non-exempt charitable trust described in IRC Sec 4947(a)(1) regardless of gross receipts. Organizations with gross receipts that are normally $50,000 or less may choose to electronically file FTB 199N.

Normally “less than $50,000” means if the organization has been:

When Form 199 is required, it is due by the 15th day of the 5th month after the accounting period ends (May 15 for calendar year organizations). It can be either e-filed or paper-filed.

The following organizations are not required to file Form 199:

-

Churches, inter-church organizations of local units of a church, conventions or associations of churches, or integrated auxiliaries of churches.

-

Religious orders.

-

Organizations formed to carry out a function of a state, or a public body that is carrying out that function and is controlled by the state, or a public body.

-

Political organizations exempt under R&TC Section 23701r.

-

Qualified state tuition programs exempt under R&TC Section 23711.

-

Coverdell ESA exempt under R&TC Section 23712.

-

Stock bonus, pension, or profit-sharing trusts exempt under R&TC Section 17631.

Extension and Penalties

If Form 199 cannot be filed on time, the exempt organization has an additional six months to file without filing a written request for extension. However, an organization that is not in good standing or suspended on the original due date of the return will not be given an extension of time to file. For more information, see form FTB 3539, Payment for Automatic Extension for Corporations and Exempt Organizations.

If the return is not filed and/or the filing fee is not paid by the extended due date, the following penalties, additional fees, and interest may be imposed.

-

Penalty for Failure to File a Timely Return – If the return is not filed on or before the original due date, or extended due date, the penalty is $5 for each month, or part of the month, the return is late. If the return is not filed by the extended due date, the automatic extension will not apply. The penalty may not exceed $40.

-

Failure to Furnish Information – In the case of a private foundation, the FTB may make a written demand that a delinquent return or foundation report be filed within a reasonable amount of time after mailing a demand notice. The person who fails to file after such demand is subject to a penalty of $5 for each month, or part of the month, (not to exceed $25) after the period expires.

-

Waiver – The FTB has the authority to waive the above penalties and late payment fee if it is shown that the failure was due to reasonable cause and not due to willful neglect.

-

Suspension/Revocation – The corporate rights, powers, and privileges of the organization may be suspended, or the exemption from tax may be revoked, for failure to file a return or pay the filing fee, penalties, or interest.

-

Interest – Interest accrues on the delinquent penalty from the original due date of the return until the penalty is paid.

More Information

See the instructions to Form 199, available on the FTB web site: 2023 Form 199: California Exempt Organization Annual Information Return | California Forms & Instructions | FTB.ca.gov