IRS Form 1116 Exemption Exception

Find everything you need to know about the IRS Form 116 exemption exception.

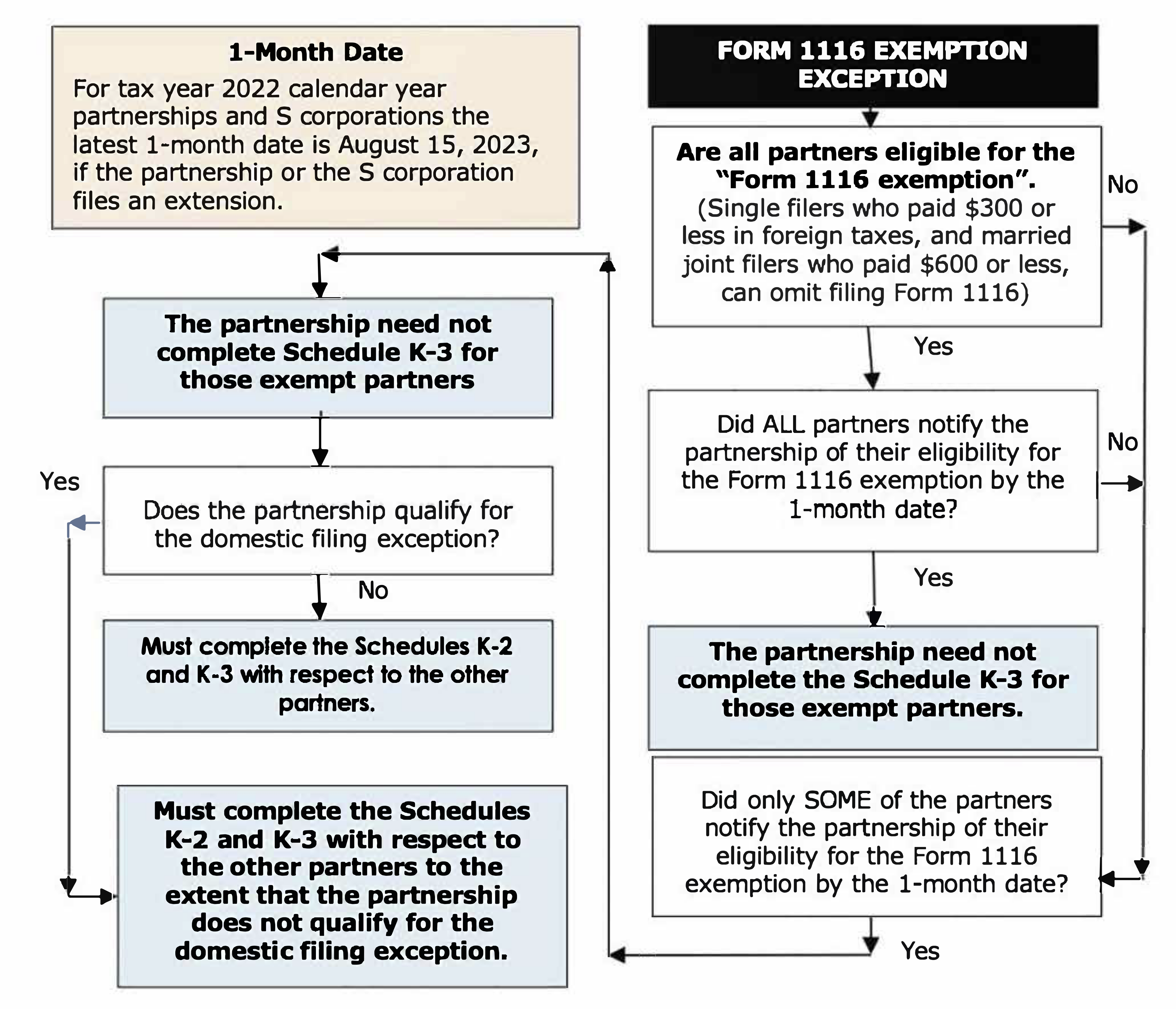

Under section 904(j), certain partners/shareholders are not required to file a Form 1116. This is the Form 1116 exemption, where single filers who paid $300 or less in foreign taxes, and married joint filers who paid $600 or less, can omit filing Form 1116 and still claim a foreign tax credit (see election to claim the foreign tax credit without filing Form 1116 – Page 1 of the 2022 Form 1116 instructions.

A domestic partnership or an S-corporation is not required to complete Schedules K-2 and K-3 if all partners/shareholders are eligible for the Form 1116 exemption and the partnership/ S corporation receives notification of the partners’ eligibility for such exemption by the 1-month date (as defined above).

If a partnership/S corporation receives notification from only some of the partners/shareholders that they are eligible for the Form 1116 exemption, the partnership/S corporation need not complete the Schedule K-3 for those exempt partners/shareholders but must complete the Schedules K-2 and K-3 with respect to the other partners/shareholders to the extent that the partnership/S corporation does not qualify for the domestic filing exception.

Note: Where the following flow chart refers to partners or partnership, you can substitute shareholders and S corporation when applicable.

Example – Husband and wife (H&W), both U.S. citizens, each own a 50% interest in U.S. Partnership (USP), a domestic partnership. H&W and USP each have calendar tax years. USP invests in a RIC. USP receives a Form 1099 from the RIC reporting $400 of creditable foreign taxes paid or accrued on passive category foreign source income. USP’s only foreign activity is that from the RIC. H&W do not pay or accrue any foreign taxes other than their distributive share of USP’s foreign taxes. Husband and wife also do not have any other foreign source income. H&W qualify for the Form 1116 exemption and notify USP by the 1-month date that they do not need the Schedule K-3. Even though USP does not qualify for the domestic filing exception because the creditable foreign taxes treated as paid or accrued by USP are greater than $300, because husband and wife notify USP by the 1-month date that they do not need the Schedule K-3 under the Form 1116 exemption, USP need not complete Schedules K-2 and K-3.