Tax Information - Materials and Supplies For Repairs

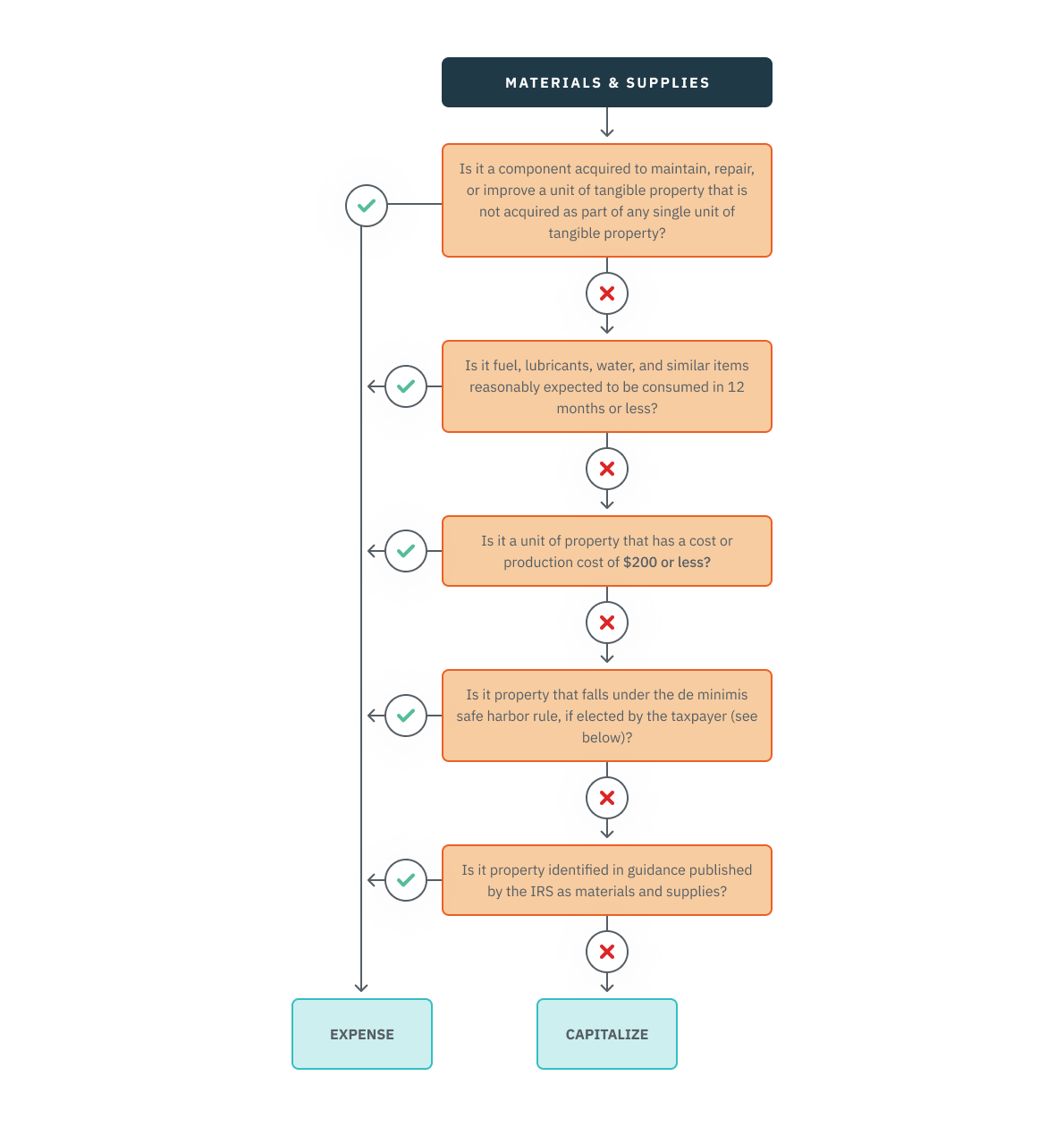

The cost of acquiring or producing materials and supplies is tax deductible in the tax year in which the materials and supplies are used or consumed in the taxpayer’s operations. “Materials and supplies” means tangible property that is used or consumed in the taxpayer’s operations that is not inventory and that:

-

Is a component acquired to maintain, repair, or improve a unit of tangible property owned, leased, or serviced by the taxpayer and that is not acquired as part of any single unit of tangible property (Example: replacing the engine in a fork lift);

-

Consists of fuel, lubricants, water, and similar items that is reasonably expected to be consumed in 12 months or less, beginning when used in the taxpayer's operations (Example: a barrel of grease used to lubricate vehicles);

-

Is a unit of property (UOP) with an economic useful life of 12 months or less, beginning when the property is used or consumed in the taxpayer’s operations;

-

Is a UOP that has a cost or production cost of $200 or less;

-

Is any property that meets the de minimis rule (see below) OR

-

Is identified in guidance published by the IRS as materials and supplies for which treatment is permitted under §1.162-3(d).