Partial Disposition Election

The partial disposition election is a tax option that can be beneficial in certain cases. Find out more about how this election works below.

A taxpayer may make an election under this provision to report the gain or loss on the replacement, retirement, or other disposition of a partial asset. However, if the taxpayer makes this election the taxpayer must:

-

Capitalize the replacement portion under the same asset class as the disposed portion, and

-

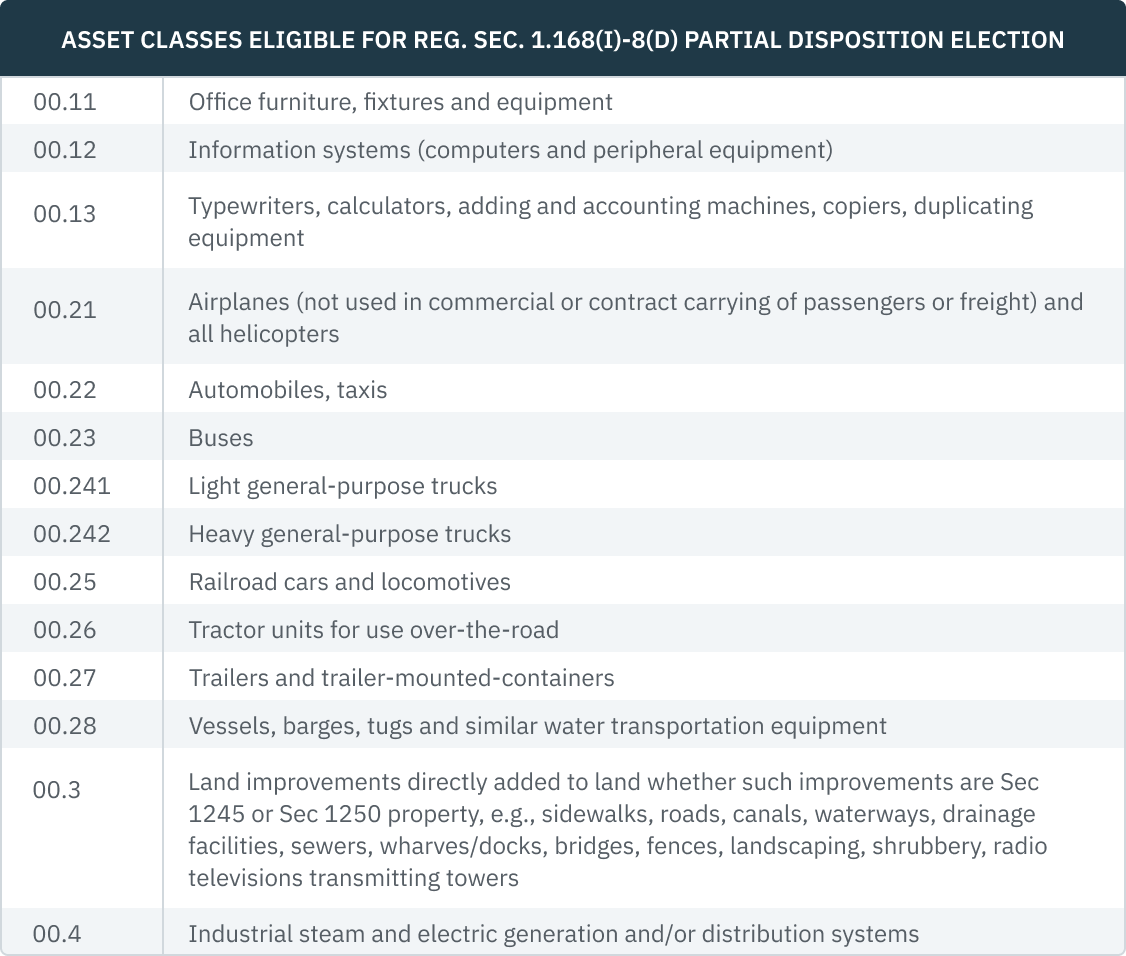

The asset must be within the asset classes 00.11 through 00.4 of Rev. Proc. 87-56 (described below).

This election does not apply to betterments or an adaptation of the asset to a new or different use.

What Does a Partial Disposition Election Accomplish?

It allows taxpayers to elect gain or loss on the replacement, retirement, or other disposition of a partial asset. A good example of that would be replacing the roof on a building that is not completely depreciated. Prior to the release of the new regulations the old roof would have to remain on the books as part of the whole asset and if not already depreciated to zero, continue to be depreciated.

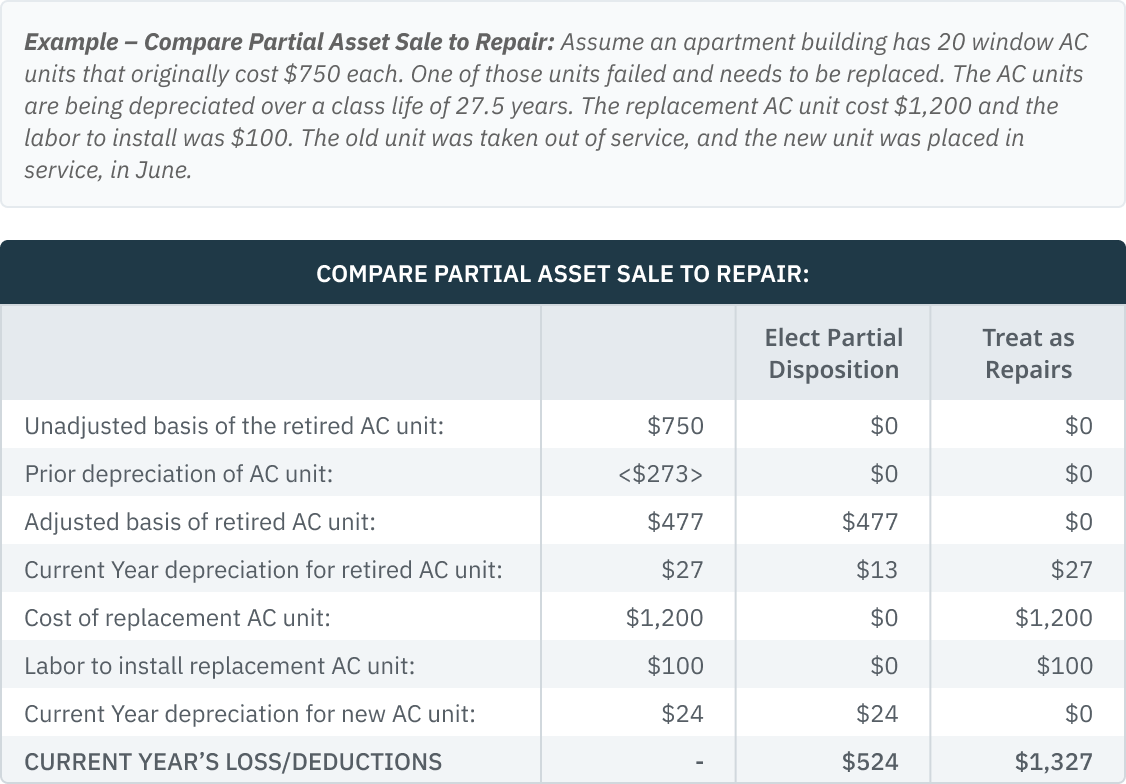

Example – Rental Roof: Mel owns a residential rental property that needs a new roof. Mel determines the retiring roof has an unadjusted basis of $25,000 (27.5-year MACRS life, straight line) on which he has taken $16,817 in depreciation, leaving it with a remaining undepreciated basis of $8,183. If Mel elects a partial disposition for the roof, it will result in an ordinary loss of $8,183. However, he will have to capitalize the replacement roof and depreciate it over 27.5 years and forego any option to expense the roof under any other provision.

-

| Which Part of the Roof? |

| When it comes to the requirement to capitalize or expense a roof one has to consider which part of the roof they are dealing with. For taxes, the roof is generally broken down into two elements, the structural component (for example the underlying plywood) and the membrane (shingles, asphalt covering, tar paper, etc.). Thus, if a taxpayer replaced only the membrane that would be repair, whereas replacing the underlying roof plywood would be a capital betterment. If the underlying roof plywood were replaced then the entire cost of replacing the roof, including the membrane, would have to be capitalized. |

CAUTION

The final regulations allow partial dispositions of assets held in single or multiple asset accounts but dramatically limited the availability of this election for those taxpayers who have the assets in general asset accounts (GAA). GAAs are not covered in this material.

Example (based on Regulations Example #1) – Partial Disposition NOT elected - Alicia owns an office building with four elevators. She replaces one of the elevators. The elevator is a structural component of the office building. In accordance with Reg. §1.168(i)-8(c)(4)(ii)(A), the office building, including its structural components, is the asset for disposition purposes. Alicia does not make the partial disposition election provided under Reg. §1.168(i)-8(d)(2) for the elevator. Thus, the retirement of the replaced elevator is not a disposition. As a result, depreciation continues for the cost of the building, including the cost of the retired elevator and the building's other structural components, and Alicia does not recognize a loss for this retired elevator. If Alicia must capitalize the amount paid for the replacement elevator pursuant to §1.263(a)-3, the replacement elevator is a separate asset for disposition purposes pursuant to Reg §1.168(i)-8(c)(4)(ii)(D) and for depreciation purposes pursuant to section 168(i)(6).

-

Example (based on Regulations Example #2) – Treated as Separate Asset - The facts are the same as in Example 1, except Alicia accounts for each structural component of the office building as a separate asset in her fixed asset system. Although Alicia treats each structural component as a separate asset in her business’ records, the office building, including its structural components, is the asset for disposition purposes in accordance with Reg §1.168(i)-8(c)(4)(ii)(A). Accordingly, the result is the same as in Example 1.

-

Example (based on Regulations Example #3) – Partial Disposition Election Made - The facts are the same as in Example 1, except Alicia makes the partial disposition election for the elevator. Although the office building, including its structural components, is the asset for disposition purposes, the result of Alicia making the partial disposition election for the elevator is that the retirement of the replaced elevator is a disposition. Thus, depreciation for the retired elevator ceases at the time of its retirement, and Alicia recognizes a loss upon this retirement. Further, Alicia must capitalize the amount paid for the replacement elevator, and the replacement elevator is a separate asset for disposition and depreciation purposes pursuant to section 168(i)(6).

-

Asset

Solely for the purposes of the partial election the term asset or a portion of an asset is limited to an asset in asset classes 00.11 though 00.4 (See previous table).

Determining the Unadjusted Basis of an Asset Included in a Multiple Asset Account

The taxpayer can use any reasonable method to determine what portion of the entire asset basis is assigned to the partial disposition. Although the regulations say “any reasonable method,” they also provide three examples of reasonable methods:

-

Discounting the cost of the replacement asset to its placed-in-service year cost using the Producer Price Index for Finished Goods or its successor, the Producer Price Index for Final Demand, or any other index designated by guidance in the Internal Revenue Bulletin;

-

A pro rata allocation of the unadjusted depreciable basis of the multiple asset account or pool based on the replacement cost of the disposed asset and the replacement cost of all of the assets in the multiple asset account or pool; and

-

A study allocating the cost of the asset to its individual components.

CAUTION

Making this election may not provide the best outcome for the taxpayer since the taxpayer must capitalize rather than expense the replacement asset.

Disposition Election after IRS Disallows Repair Deduction

A taxpayer may make a delayed partial disposition election if the IRS disallows the taxpayer’s repair deduction and requires that amount to be capitalized. The delayed election is made by applying for a change in accounting method, Code 198. However, the asset for which the change is being made must have been owned by the taxpayer at the beginning of the change year.

Making the Election

No formal election is required. The election is made by applying the partial disposition provisions for the taxable year in which the portion of an asset is disposed of by the taxpayer by reporting the gain, loss, or other deduction on the taxpayer's timely filed, including extensions, original Federal tax return for that taxable year. No accounting method change is needed or allowed to make this election.

Revoking the Election

To revoke a partial disposition election, the taxpayer must do so via a request for a letter ruling.

California Differences - Capitalization & Repair Regulations

California follows the federal capitalization and repair regulations except California will follow the de minimis safe harbor increases on a prospective basis only. Thus, for CA purposes the increase from $500 to $2,500 will only apply to years beginning on or after 1/01/16. Because no retroactive increase is allowed for CA, the FTB will not follow the audit protection provisions of IRS Notice 2015-82 in excess of $500 for pre-2016 tax years.