750 Hours of Participation - Real Estate Qualification

The IRS has a number of specific tax rules that pertain to real estate professionals. The "750-hour rule" is one of these.

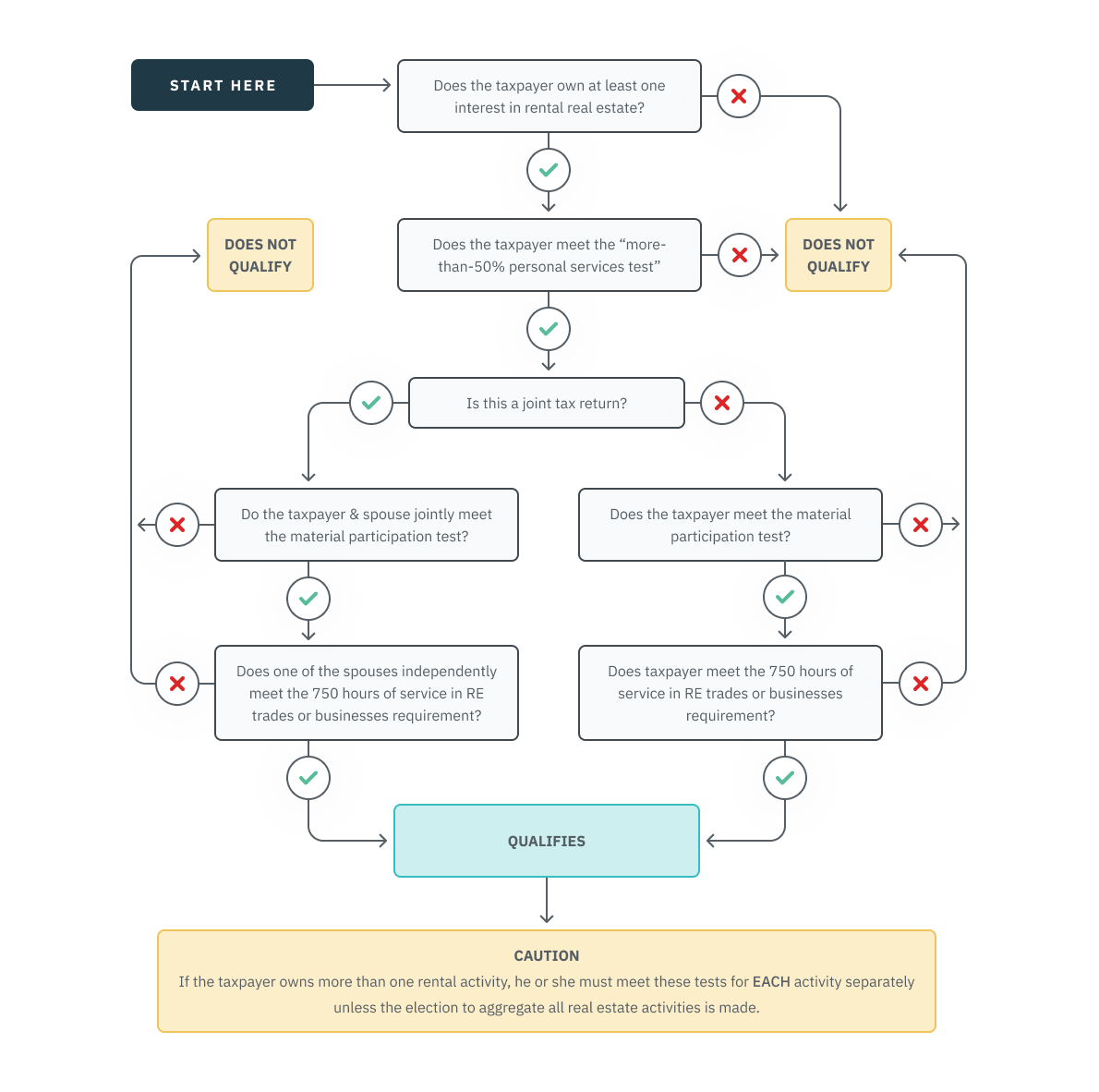

In short, to qualify as a real estate professional a taxpayer must perform more than 750 hours of services during that year in real property trades or businesses in which he materially participates. (Code Sec. 469(c)(7)(B)(ii))

Married Taxpayers

Spouses filing a joint return qualify as real estate professionals only if one spouse separately satisfies the above tests (Code Sec. 469(c)(7)(B), Reg § 1.469-9(c)(4)), without regard to the other spouse's services.

Each Interest Treated as a Separate Activity Unless Aggregation Elected

In determining whether a taxpayer is a real estate professional, each of his interests in rental real estate is treated as a separate activity, unless he elects (by filing a specified statement with his original income tax return) to treat all interests in rental real estate as one activity. (Code Sec. 469(c)(7)(A); Reg § 1.469-9(g)) The election is binding for the tax year it's made and for all future years in which the taxpayer qualifies. Failure to elect in one year doesn't bar the election in a later year. (Reg § 1.469-9(g)(1)). See page 3.26.05 of this chapter for more on this election.

The material participation requirement is most satisfied by participating in the activity for more than 500 hours during the tax year. A real estate professional with multiple rental real estate interests, who wants to treat all these interests as nonpassive but who has not elected to treat all those interests as a single activity, would have to satisfy this test separately for each interest.

Example: Peter owns three rentals but did not file the election to treat all of them as a single activity. If Peter is unable to qualify under one of the other material participation tests, he would need to participate in each rental activity for 500 hours a year. At minimum, that would result in 1,500 hours per year or just over 28 hours a week. If Peter had filed the election to treat all three interests as a single activity, he would only need to participate in the combined rentals 500 hours a year (just under 10 hours a week).

-

Travel Time for the 750-Hour Test

Taxpayer's log originally showed fewer than 750 hours spent on her rental properties, but after it was revised to include travel time from her home to one of her properties, the test was passed. IRS didn't accept the revised log, arguing the travel time was included in the original, but the Tax Court disagreed and held in taxpayer's favor. (Leyh, Richard S., (2015) TC Summary Opinion 201527) This is contradictory to a prior ruling where travel between home and a place of business (cattle breeding activity) did not qualify as work related travel. (Truskowsky, Thomas E., (2003) TC Summary Opinion 2003-130). CAUTION: in the Leyh decision the Tax Court did not consider the commuting issue. Generally, travel between home and the first business location would not be deductible unless the taxpayer’s home qualifies as the site of a business under the home office rules.

On-Call Time Doesn’t Qualify for the 750 Hour Test

An individual who owned four real estate rental properties could not count the hours that he considered himself "on call" to perform services on the properties toward the 750-hour threshold. The Tax Court said the law and regulations refer to “work performed,” so on-call time, un-associated with services actually performed by the taxpayer, did not count toward the 750-hour requirement (Moss v Commissioner, U S Tax Court, CCH Dec 58,336, 135 T.C. No. 18).

Short-Term Rentals Not Included for Purposes of Meeting the 750-Hour Test

The Tax Court, in Bailey, TC Summary Opinion 2011-22, ruled that a taxpayer didn't meet the qualifying real estate professional's exception to the per se passive activity loss (PAL) rule because one of her properties didn't count for purposes of meeting the 750-hour test since it was used for short-term rentals.

Citing Reg. § 1.469-1T(e)(3)(ii), the Tax Court held that when a taxpayer spends time on a real estate property that is rented for periods averaging less than 7 days, that property is no longer a “rental activity.” Therefore, the time spent on the property is not included for purposes of counting hours for the 750-hour test to be a real estate professional.