General Business Meal Deduction Requirements

Discover IRS rules for general business meal deduction requirements, including what constitutes a "lavish" lunch or dinner expense.

As with travel expenses, meal expenses must be “ordinary” and “necessary” in carrying on a trade or business. (Code Sec 162) Under the TCJA, no deduction is allowed for the expense of any food or beverages unless the expense “is not lavish or extravagant under the circumstances and the taxpayer (or an employee of the taxpayer) is present at the furnishing of such food or beverages.” (Code Sections 274(k)(1)(A) and (B))

Lavish

Meal expenses are deductible up to an amount not considered “lavish” (i.e., reasonable under the circumstances). The taxpayer (or a representative of the taxpayer) must be present. The representative could be, for example, the taxpayer’s employee, an attorney, or an independent contractor who performs significant services for the taxpayer.

The term lavish or extravagant is frequently used in the tax code. Unfortunately, nowhere in the Code are the terms lavish or extravagant defined in a measurable way. For example, in relation to business meals, Sec 274(k)(1)(A) says “lavish or extravagant under the circumstances.” So, it boils down to a facts and circumstances determination.

Pub 463 says this about “lavish and extravagant” and facts and circumstances: “Meal expenses won't be disallowed merely because they are more than a fixed dollar amount or because the meals take place at deluxe restaurants, hotels, or resorts.”

When discussed with a tax professor, he asked would a $1,000 bottle of wine purchased at a business meal be considered extravagant? Then he came up with this…what if it was a Boeing salesman trying to close a billion dollar aircraft sale? So, the “under the circumstances” makes a big difference. We hope you get the drift.

Away-From-Home Meals

When taxpayers travel away from home on business, they may deduct 50% of the cost of their own meals (100% for restaurant-provided meals in 2021 and 2022). A business traveller who pays for meals consumed with out-of-town clients or associates may deduct the cost of the clients’ or associates’ meals (at 50% or 100% for meals provided by a restaurant in 2021 and 2022).

Example - Away-From-Home Meals - Margaret, who is self-employed, went on a five-day business trip to Minneapolis in 2022 to make sales presentations. Margaret received no reimbursement for her meals during the trip. Margaret ate alone in her hotel on the first three nights away, at a total cost of $200. On the fourth night, she met one of her college friends for dinner. Margaret paid the tab of $180. The next day, she invited Martie, a purchase representative for one of the companies whose business Margaret was soliciting, to dinner. Their dinner followed a full day of discussion on the products Margaret sells. Margaret paid for dinner that night too, a total of $300. All of the meals were at restaurants. Margaret’s deductible meal expense is $590 for the trip ($200, meals alone + $90, her portion of dinner with friend + $300, meal with Martie)). The 50% limit doesn’t apply because the meals were at restaurants. If the business trip took place in 2023, the deductible meal expense would be $295 (50% x ($200+ $90 + $300)).

-

Business Meal Recordkeeping

Meal expenses are deductible only if substantiation requirements are met. Code Section 274(d) requires substantiation of the following:

-

The amount

-

Business purpose

-

Date, time and place

-

Names of guests & business relationship

Reimbursed Expenses

If a taxpayer is reimbursed for business meal costs and makes an adequate accounting, the 50% rule applies to the one who makes the reimbursement, not the taxpayer.

Using Per Diem Rate to Substantiate Employee’s Expenses for Lodging, Meals and Incidentals

(Rev Proc 2011-47, modified by Rev. Proc. 2019-48 to account for TCJA changes and Notice 2011-81) – Rev Proc 2011-47 details the rules, effective October 1, 2011, for using a per diem rate to substantiate the amount of an employee’s expenses for lodging, meals and incidentals that an employer (or third party) reimburses, and explains how an employee or self-employed individual may use the “standard meal allowance.” This revenue procedure will only be updated as necessary in the future.

Rev Proc 2011-47 also clarifies that partners and volunteers who receive reimbursements from payors may use the methods allowed in the procedure to substantiate their expenses.

Instead of an annual revenue procedure, the IRS issues a shorter, annual notice providing the special per diem rates effective as of October 1 of the year issued. The 2021-2022 rates are included in Notice 2021-52; 2020-2021 rates are in Notice 2020-71; 2019-2020 rates are in Notice 2019-55; 2018-2019 rates are in Notice 218-77; 2017-2018 rates are in Notice 2017-54; and 2016-2017 rates were published in Notice 2016-58.

Rev Proc 2011-45 was updated by Rev Proc 2019-48 with respect to the TCJA changes mentioned throughout this chapter.

Club Dues Deductions

No deduction is allowed for amounts paid or incurred for membership in any club organized for business, pleasure, recreation or other special purpose. (Code Sec 274(a)(3))

According to IRS Pub 535 (page 47, 2021 edition) the following organizations aren't treated as clubs organized for business, pleasure, recreation, or other social purpose unless one of the main purposes is to conduct entertainment activities for members or their guests or to provide members or their guests with access to entertainment facilities.

-

Boards of trade

-

Professional organizations such as bar

-

Business leagues, associations and medical associations

-

Chambers of commerce

-

Real estate boards

-

Civic or public service organizations

-

Trade associations

Meals and Lodging of Firefighters

They are no longer allowed 2018 through 2025

Optional Method for Deducting Away-From-Home Meals

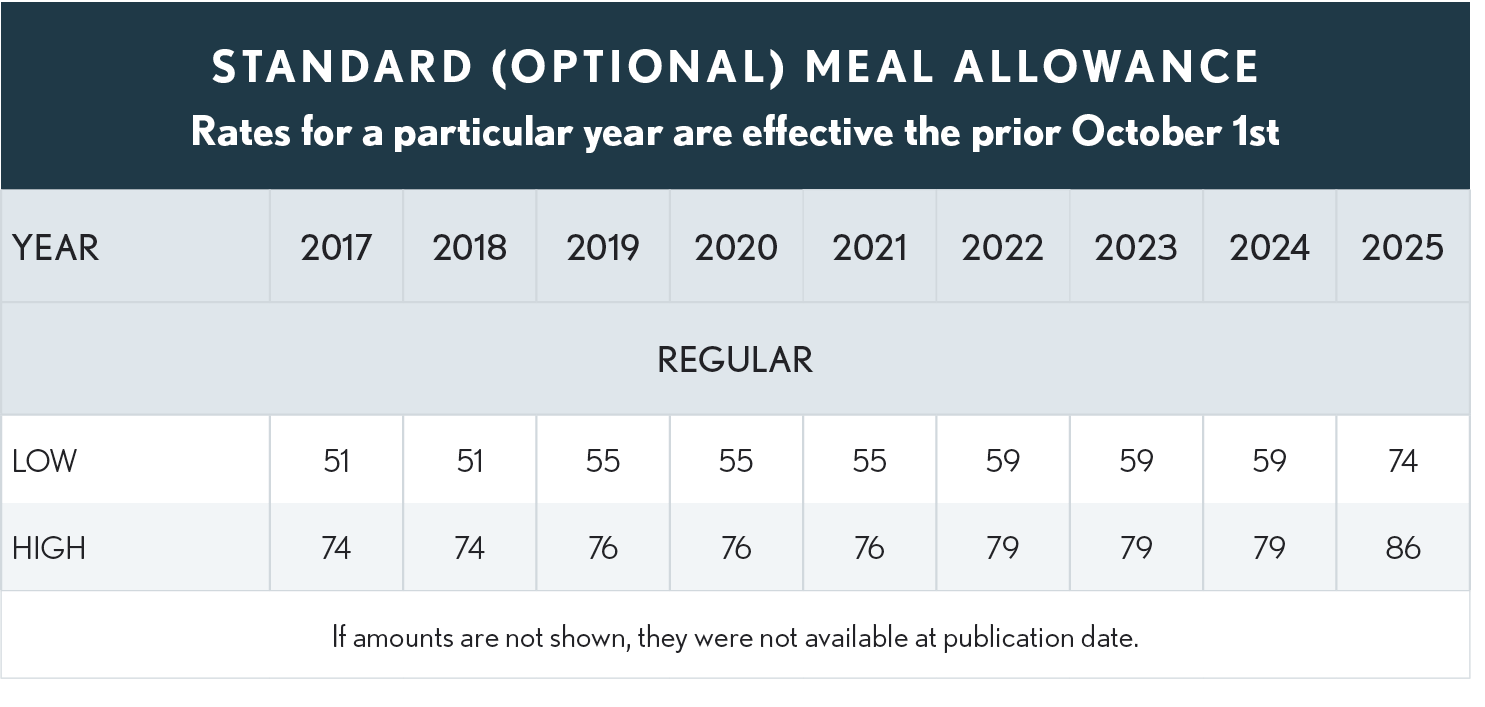

Under several revenue procedures meal deductions are allowed using optional meal rates equal to the federal meal and incidental expenses (M&IE) per diem rate for the location to which the taxpayer is traveling on business (but not for medical or charitable purposes). The optional rate method, also called the standard meal allowance, is elective and can be used by self-employed individuals. The optional meal allowance must be prorated for both the days of departure on and return from the trip (IRS allows either 75% of the daily rate for each of the first and last days of the trip or any consistently applied method that is in accordance with reasonable business practices).

Under the optional rate method, the same rate is used no matter how long the stay away from home, but varies by location. For travel in 2022 the standard meal allowance is $59 for most small localities in the U.S. (for 2019, 2020 and 2021 the standard meal allowance is $55 in low-cost localities). The rate is generally higher for major cities, resort areas and other locations in the U.S., with the highest being $79 in 2022 ($76 for 2019 through 2021). The applicable rate can be found at the following web site: www.gsa.gov/perdiem

The standard meal allowance rates noted above do not apply to travel in Alaska, Hawaii or other locations outside the continental United States (CONUS). The foreign location rates are normally published by the various tax services in conjunction with explanations of Code Section 274. Or they can be found on the Internet at:

Non-foreign areas outside CONUS (e.g., Hawaii, Alaska, Puerto Rico): http://www.defensetravel.dod.mil/site/perdiemCalc.cfm

Foreign per diem rates: https://aoprals.state.gov/web920/per_diem.asp

New federal CONUS rates are published each year, effective from October 1 of that year through September 30 of the following year (coinciding with the federal government’s fiscal year). However, there may be mid-year changes to some of the high-low rates, which will be reflected on the web site referenced above. For 2022, in lieu of the updated rates that will be effective October 1, 2022, a taxpayer claiming the standard meal allowance may continue to use the CONUS rates in effect for the first 9 months of 2022 for all of calendar 2022. However, the taxpayer must consistently use either the rates for the first 9 months of 2022 or the updated rates for the period October 1, 2022, through December 31, 2022.

Substantiation of time, place and business purpose is still required when claiming the standard meal allowance. If a self-employed person uses the standard meal allowance in 2021 or 2022, it is presumed the 50% limitation applies because it’s unknown whether the meals were provided by restaurants.

Caution – Lodging Per Diem

Although per diem rates may be used to substantiate deductions for lodging, meals, and incidental expenses, or for meal expenses and/or incidental expenses only, they may not be used to substantiate deductions for lodging expenses only. Self-employed individuals are not entitled to use the federal per diem rates to substantiate lodging expenses under any circumstances (Starr v. Commissioner, TC Memo. 2000-305). There is no optional standard lodging amount similar to the standard meal allowance. The allowable lodging expense deduction is the taxpayer’s actual cost.

No Double Dipping Allowed

A business traveler who elects to use the standard meal allowance, and who also has a qualified meal expense during the trip, cannot deduct his own meal expense incurred at that event.

Example: Arnold is a self-employed computer software salesperson who travelled away from home in 2020 for several days to meet with potential clients. He opts to use the standard meal allowance method for his meal expense deduction. He meets with two prospective clients for dinner to discuss the benefits of his company’s products and pays for the meals – his guests’ meals cost $70 and his was $30. He can deduct the $70 expense plus the full daily standard meal allowance amount, with both amounts subject to the 50% reduction, but he can’t also include the $30 he spent for his meal.For 2021/2022: if the dinner with clients was at a restaurant, the $70 would be 100% deductible but would the standard meal allowance for that day only be 50% deductible? As noted on page 3.10.02, in Notice 202163 the IRS says that a taxpayer that properly applies the rules of Rev. Proc. 2019-48 may treat the meal portion of a per diem rate or allowance paid in 2021 or 2022, as being attributable to food or beverages provided by a restaurant.

-

Incidental Expenses

The optional meal allowance is intended to cover both daily meals and incidental expenses while traveling away from home on business. Incidental expenses are defined the same as the definition of incidental expenses in the Federal Travel Regulations, which the General Services Administration says include only fees and tips to:

-

Porters

-

Hotel staff, and

-

Baggage carriers

-

Staff on ships.

Mailing costs of filing travel vouchers and paying employer-sponsored credit card billings, and transportation between lodging or business sites and places where meals are taken, are not included as incidental expenses. Instead, taxpayers using the per diem rates may separately deduct transportation and mailing expenses. Also not included as incidental expenses, and therefore separately deductible in addition, are the costs for:

-

Laundry

-

Lodging taxes

-

Clothes cleaning and pressing

-

Telephone calls and telegrams

If no meal expenses were paid or incurred, a business traveler may elect to use an optional method for incidental expenses only. The deductible amount for years 2010 through 2023 is $5 per day for incidental expenses paid or incurred during away-from-home business travel. This method cannot be used for any day that the standard meal allowance method is used because the standard meal amount already includes the $5 for incidental expenses.

Note: Unless indicated otherwise, rates for a given calendar year are based on the fiscal year rates effective on October 1 of the prior year.

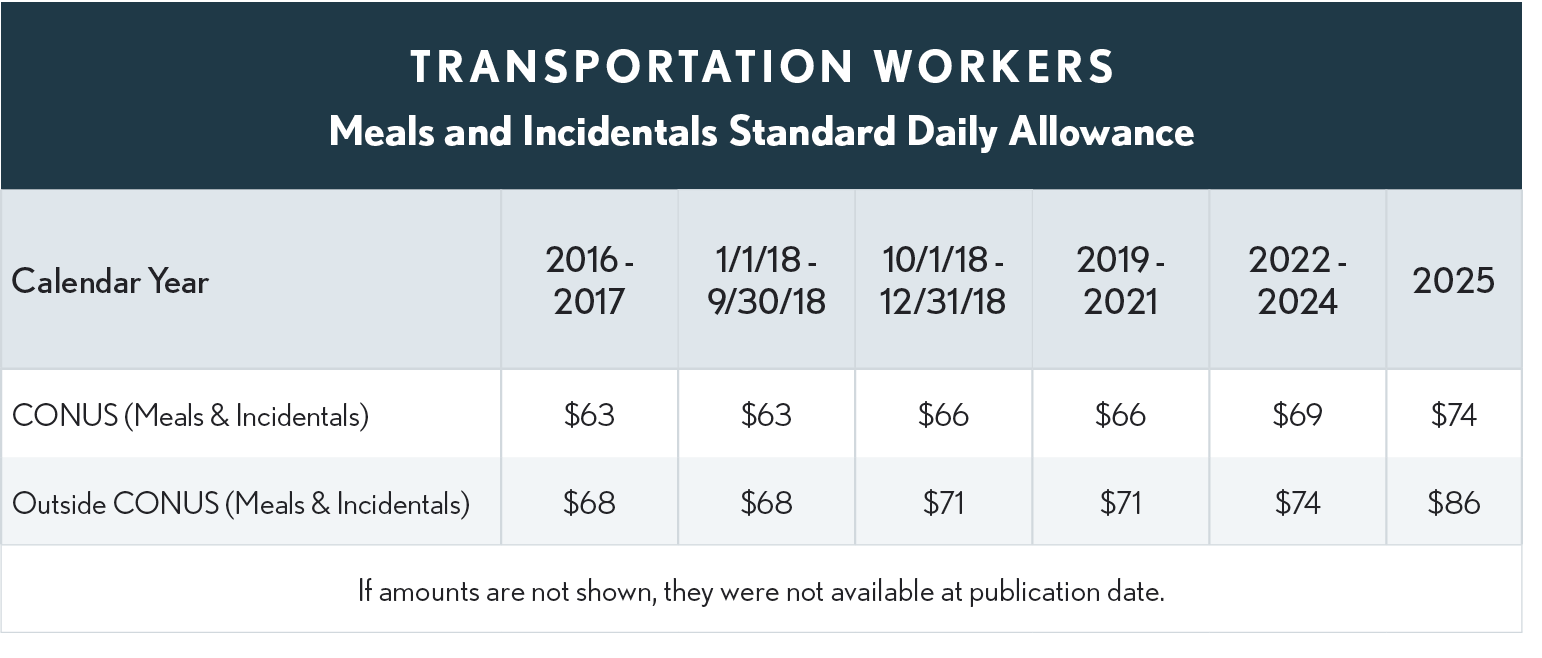

However, for years 2018 through 2025, the TCJA suspends the deduction of miscellaneous itemized deductions that are subject to the 2% of AGI reduction. This category includes employee business expenses, so employees in the transportation industry who would otherwise benefit from deducting the special standard meal allowance (see table above) will get no deduction for meal expenses during the suspension period.

Per Diem Reimbursement

In lieu of an employer reimbursing the actual substantiated expenses incurred while an employee travels on business, the employer may pay a per diem amount to the employee. This concept is unchanged by the TCJA. The per diem amount generally is intended to cover costs of away-from-home lodging, meals and incidental expenses (M&IE). As long as the rate paid is not more than the maximum amount approved by the IRS, and the employee provides appropriate substantiation (time, place and business purpose), the reimbursement is considered made under an accountable plan. Thus, it is not included in the employee’s W-2 wages and is free of income tax and FICA tax withholding.

Generally, the per diem maximum allowed by the IRS is equal to the highest per diem rate paid by the federal government to its employees on travel status. This rate varies from locality to locality, sometimes changes seasonally, and is updated periodically (see the web sites noted above). The standard meal allowance is derived from the M&IE component of these government per diem rates. The rates generally are updated as of October 1 each year (to match the federal government’s fiscal year). The rates in effect for the first nine months of the year may continue to be used for the balance of the calendar year provided it is done consistently for all travel.

Employers may choose instead to use a simplified per diem method – referred to as the high-low per diem – rather than using actual per diems. Under this method there is one rate for designated high-cost areas within the continental United States (CONUS) and another per diem rate for all other areas within CONUS. For example, effective October 1, 2021 (apply to 2022 calendar year taxpayers), the optional high-low per diem for high-cost areas is $296; it is $202 for other areas. These rates have two components, lodging (set at $222 in high-cost areas, $138 for other localities) and meals and incidental expenses ($74 in high-cost areas and $64 elsewhere).

Consistency Required

An employer who used the actual per-diem method for an employee for the first nine months of 2022 can't switch to the high-low per-diem method for that employee until Jan. 1, 2023. If the high-low substantiation method was used for an employee during the first 9 months of calendar year 2022, the employer must continue to use the high-low method for the rest of 2022 for that employee, although for travel on or after October 1, 2022, and before January 1, 2023, the employer may continue to use the rates and high-cost localities as of 10/1/21 in lieu of the updated rates and high-cost localities effective 10/1/22, if those rates and localities are used consistently during the last 3 months of the calendar year for all employees reimbursed under the high-low method.

Caution

There is no optional standard lodging amount similar to the standard meal allowance. IRS allows the per diem rates for lodging to be used as a way to satisfy adequate accounting and substantiation requirements. They are for the purpose of reimbursing employees who travel away from home for their employers, not for use by the employee or a selfemployed person to claim a tax deduction. The allowable lodging expense deduction is the actual cost and must be substantiated by receipts. The standard meal allowance amount is determined from the meals and incidental expenses component of the federal government’s per diem allowance for its workers on travel status, based on location of the travel, not from the meals and incidentals portion of the per diem rates for the high-low method.