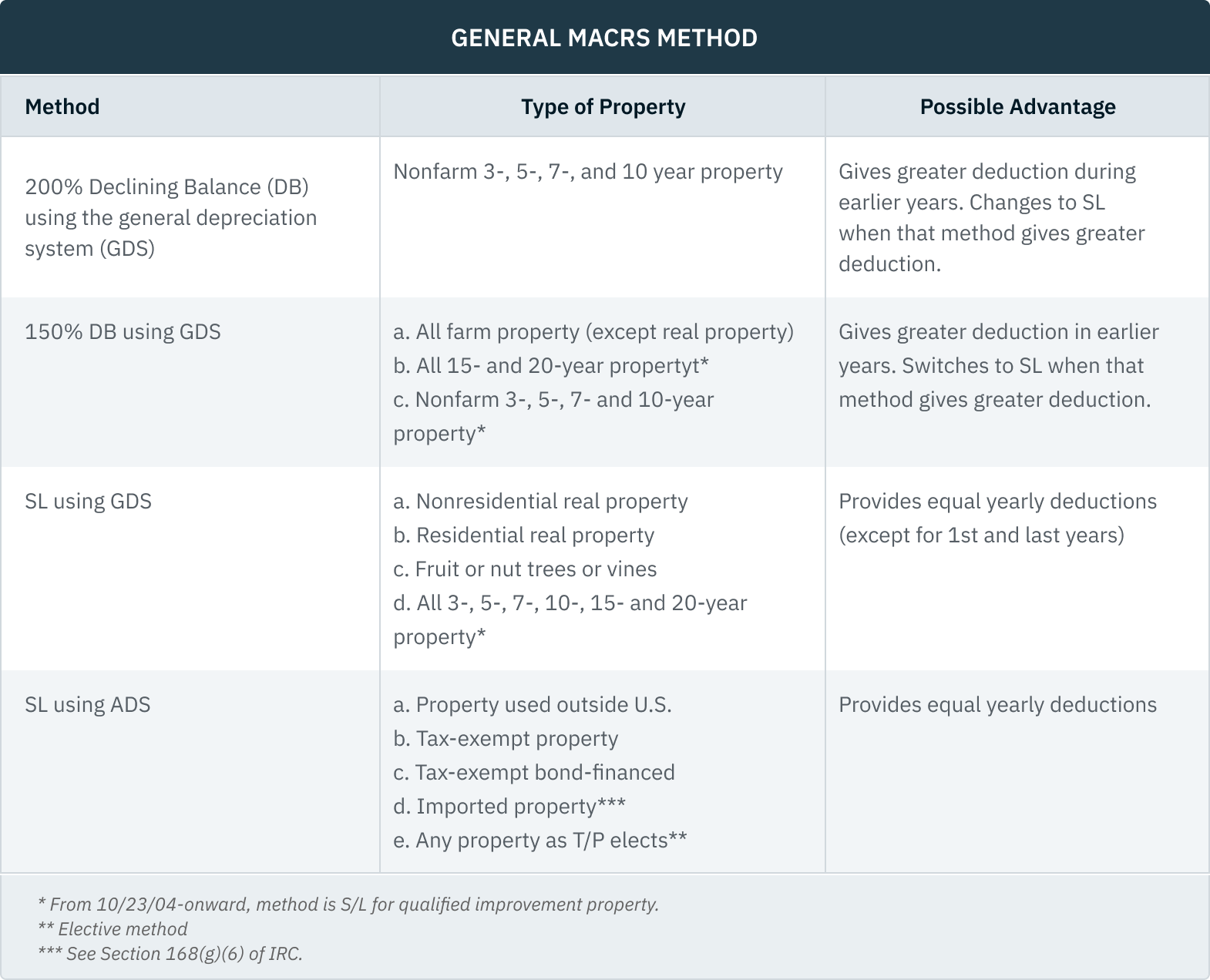

MACRS Class Life Guidelines

The IRS's Modified Accelerated Cost Recovery System (MACRS) outlines class life guidelines that generally apply to different types of property, including farms. The following table is designed to help all taxpayers understand the general MACRS method and the possible tax advantages.

IRS Revenue Procedures give guidelines for class lives - Rev Proc 87-56, Rev Proc 87-57 and Rev Proc 8822. These Rev Procs are generally effective for property placed in service after 12/31/86. To use the tables shown in Rev Proc 87-57, first determine the asset category by looking for its description in the left-hand column. The Class Life and MACRS recovery period are found to the right of the description. A recovery period labelled “ADS” (Alternative Depreciation System) is to be used to determine life for alternative minimum tax purposes or if ADS is elected for regular tax purposes.

From 10/23/04-onward, method is S/L for qualified improvement property.

* Elective method

** See Section 168(g)(6) of IRC.

Mid-Month Convention

(Applies to Non-residential Real and Residential Rental Property) Consider all property placed in service or disposed of during any month as placed in service or disposed of in the middle of that month.

Example - Mid-Month Convention - Bill purchased and placed in service a commercial building in 03/2025, at a cost of $100,000 (excluding land). The building is used by an insurance company. A full year’s cost recovery on the building is $2,564 ($100,000/39). However, using the mid-month convention, Bill is considered to have placed his new property in service in the middle of March. He gets a MACRS deduction for 9.5 months [this is 79.17% (9.5/12) of the year]. Bill’s MACRS deduction is $2,030 ($2,564 x .7917). Note that by using the IRS table for 39-year property, multiplying $100,000 by the percentage for Year 1, Month 3, the result is nearly the same ($100,000 x .02033 = $2,033).

-

Half-Year Convention

Under the half-year convention, property gets only a half year of cost recovery in the first recovery year, regardless of what month the property is placed in service. The remaining half is deducted in the year following the last year of the recovery period. Thus, a property placed in service in January gets the same MACRS deduction as it would if it had been placed in service in December (assuming the mid-quarter convention doesn’t apply). Property subject to the half-year convention gets half the yearly MACRS deduction in both the year placed in service and the year of disposition.

To use the half-year convention for taxpayers who have a short taxable year, treat an asset as acquired at the midpoint of the short year.

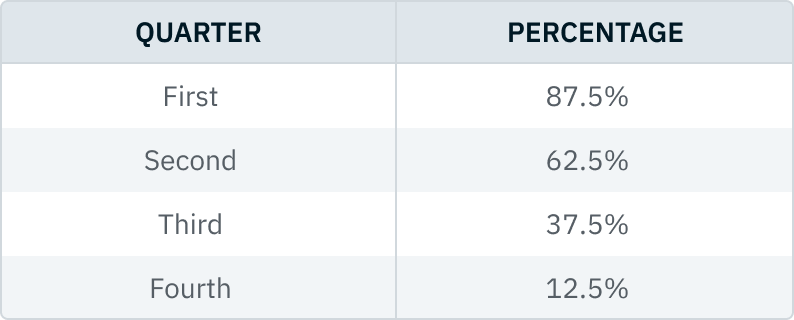

Mid-Quarter Convention

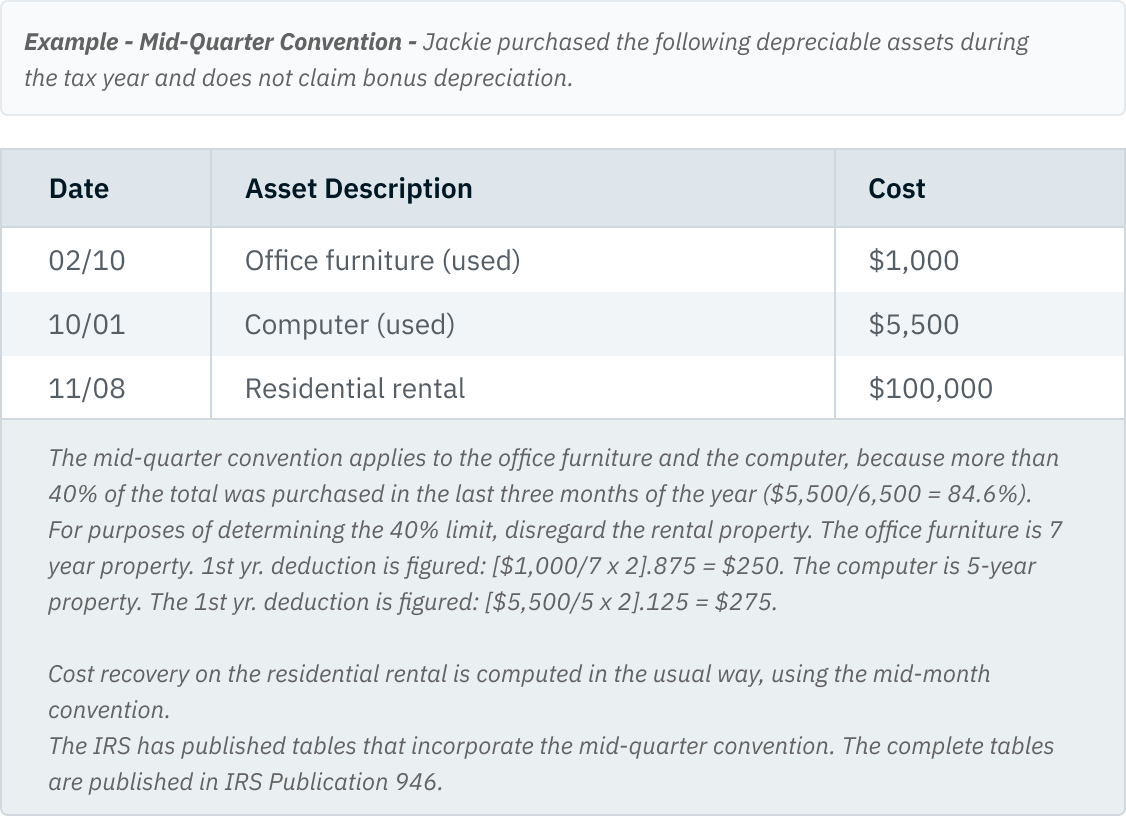

This convention treats property as placed in service (or disposed of) at the midpoint of the quarter in which it is placed in service (or disposed of). It applies when the basis of property placed in service during the last three months of the year is more than 40% of the basis of ALL property placed in service during the year. For assets placed in service when the bonus depreciation allowance applies, do not reduce basis by the bonus allowance for purpose of this test. If the 40% limit is exceeded, then the mid-quarter convention (RATHER THAN THE HALF-YEAR CONVENTION) applies to ALL property placed in service during the year. Disregard the basis of non-residential real property, residential rental property, and Section 179 deductions, as well as the personal-use portion of the basis, when making the computation to determine whether the mid-quarter convention applies. Property placed in service and disposed of during the same tax year is also not included in applying the 40% test.

To compute the deduction using the mid-quarter convention, figure the deduction for the full year, then apply the following percentages, depending on the quarter the property is placed in service: