Installment Sale of a Business

The installment sale of a business, specifically a sole proprietorship, is governed by specific IRS regulations. Details about business installment sales can be found below.

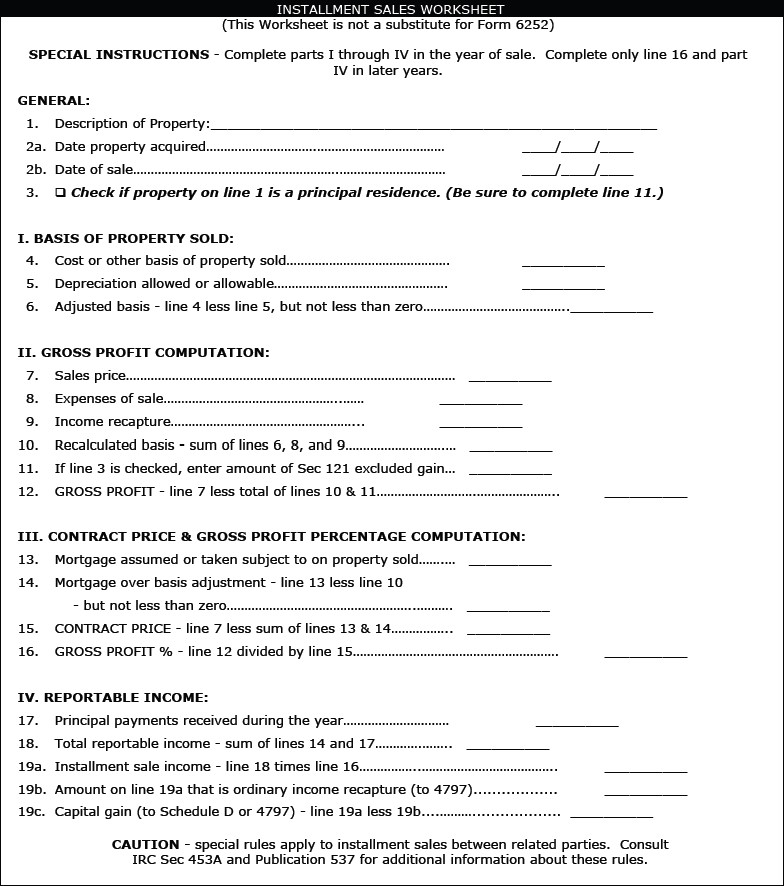

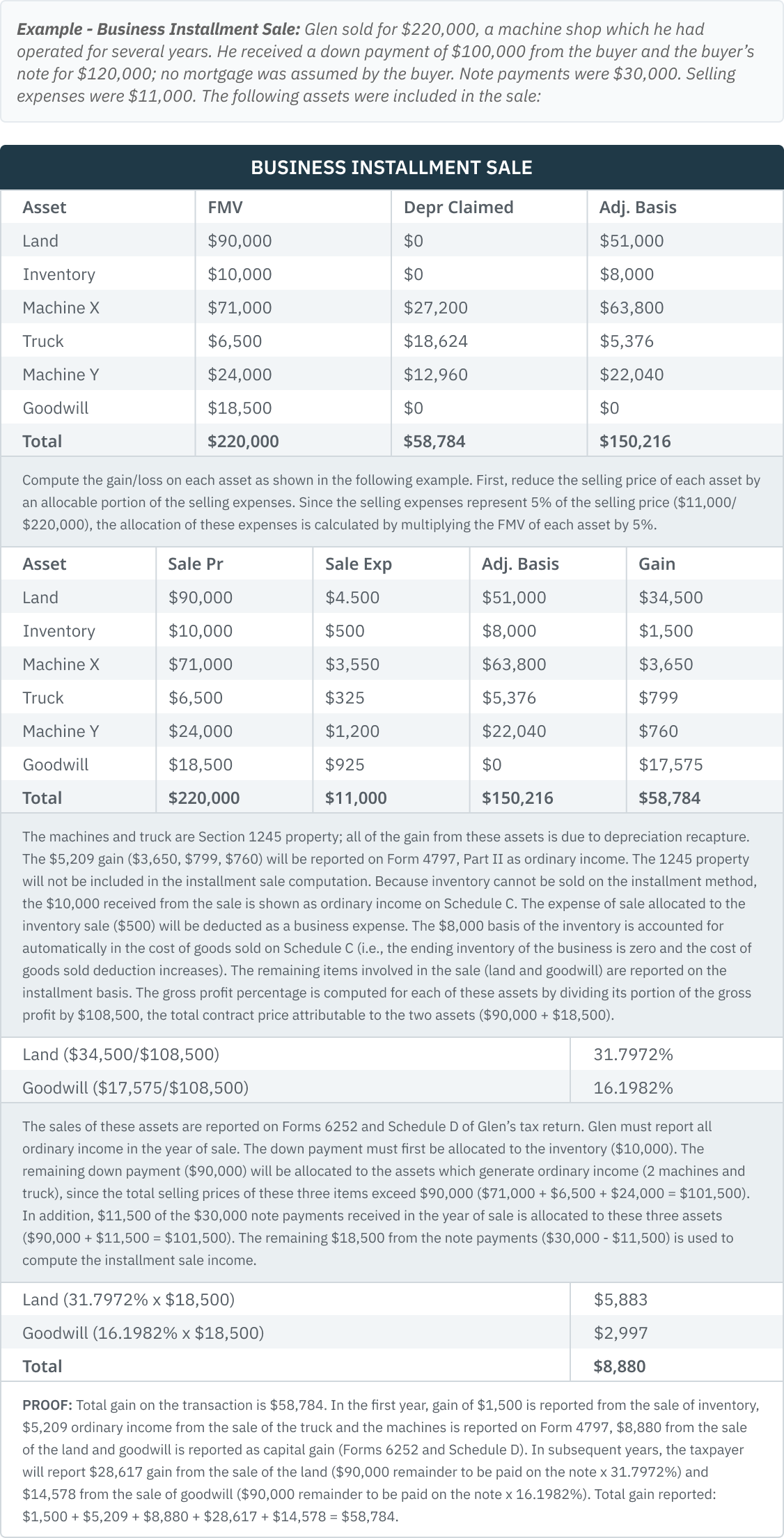

A sale of a sole proprietorship usually involves the sale of several assets. The transaction is not treated the same as the sale of multiple assets using a single contract. The business assets must be categorized by property type--i.e., inventory, Section 1245 property, Section 1250 property, goodwill, etc. Separate calculations may be required to determine the gain or loss for each asset sold. Certain kinds of property, such as inventory, do not qualify for instalment method reporting. Thus, allocations are necessary.

Transfer Due to Death

The transfer of an installment obligation (other than to a buyer) as a result of the death of the seller is not a disposition. Any unreported gain from the installment obligation is not treated as gross income to the decedent. No income is reported on the decedent's return due to the transfer. Whoever receives the installment obligation as a result of the seller's death is taxed on the installment payments the same as the seller would have been had the seller lived to receive the payments. (Reg. Sec. 1.1451-1(b)(2))

California Differences - Installment Sales

Real property sold in California may be subject to income tax withholding. California conforms to the Federal installment sale computation, except that the bases may not be the same, because different depreciation methods were used or because of differences in Federal and California Sec. 179 limitations. In that situation, use two worksheets – one for federal and one for CA.