Excess Business Losses

The Tax Cuts and Jobs Act of 2017 changed the correlation between excess business losses and federal taxes in some ways.

Under pre-TCJA law (IRC Sec 461(j)), if a non-corporate taxpayer in the farming business received an applicable government subsidy, including a Commodity Credit loan, for the tax year, the taxpayer's “excess farm loss” for that year wasn't allowed. The amount of loss that could be claimed was limited to a threshold amount of $300,000 ($150,000 for MFS taxpayers).

Under TCJA the IRC Sec 461(j) limitation on “excess farm loss” for non-corporate taxpayers no longer applies after 2017 and through 2025. Instead, all non-corporate taxpayers’ loss deductions are limited to a threshold amount (IRC Sec. 461(l) as modified by TCJA Sec. 11012(a)).

The non-deductible part of the loss is carried forward as a net operating loss.

Effective Date

This provision was originally effective for tax years beginning in 2018; however, because of the COVID pandemic, the CARES Act extended the effective year to 2021. Plus the ARPA extended the effective date through 2026. Thus the effective years are 2021 through 2026.

Amended Opportunity

The CARES Act retroactively turned off the excess active business loss limitation rule. If a taxpayer’s losses were limited by this provision prior to the retroactive law change, there may be an opportunity for an amended tax return if the refund statute has not expired.

An “excess business loss” is the excess (if any) of the taxpayer's aggregate deductions for the tax year that are attributable to trades or businesses of the taxpayer (determined without regard to whether the deductions are disallowed for that tax year) over the sum of:

-

The taxpayer's aggregate gross income or gain for the tax year, which is attributable to those trades or businesses, plus

-

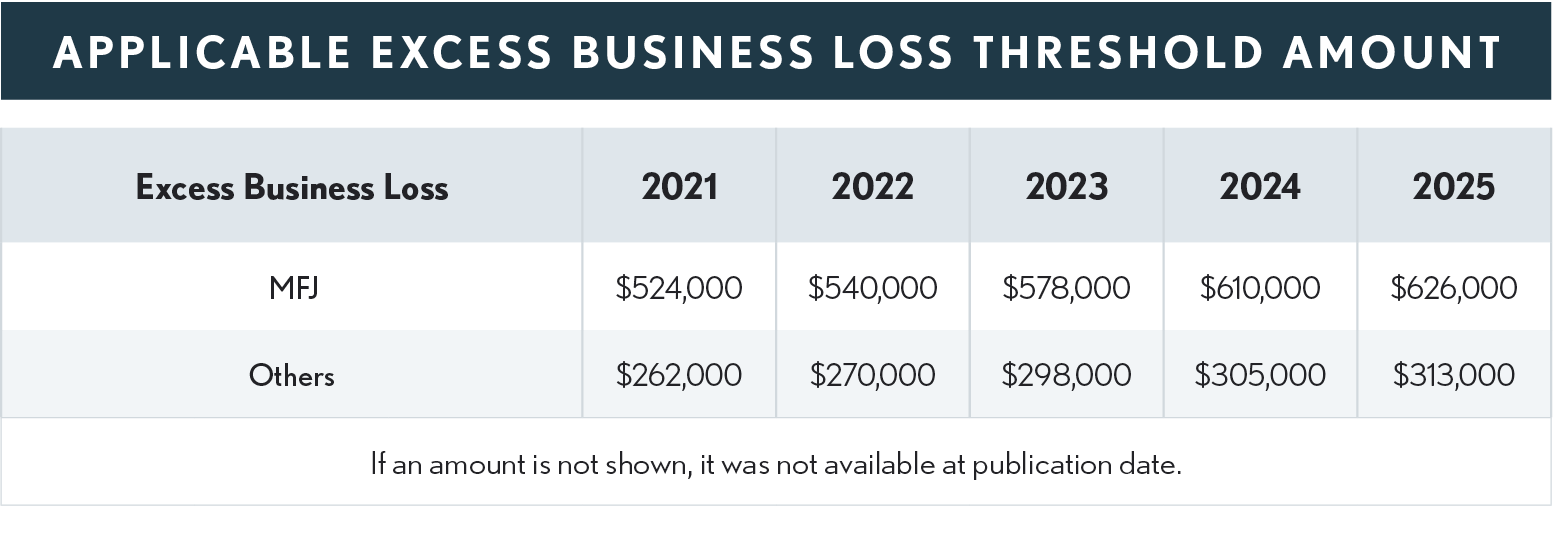

$250,000 (200% of that amount for a joint return (i.e., $500,000)). This amount is adjusted for inflation. The amounts in the table below reflect the CARES Act change that postpones this provision until 2021.

Example: A single taxpayer, in 2024, has deductions of$500,000 from a business. The taxpayer’s gross income from the business is $150,000. The excess business loss is $45,000 ($500,000 – ($150,000 + $305,000)). Thus, the taxpayer’s deductible business loss for 2024 is $305,000 and the excess business loss of $45,000 is treated as an NOL carried forward to the next year.

-

Coordination With Passive Loss Rules

Passive loss limitations apply before the excess business loss rules (Code Sec 461(l)(6)). Presumably, if a loss is disallowed under the passive activity loss rules, any deductions or income from that passive activity would not be considered in the determination of whether a taxpayer has an excess business loss.

Commentary: TCJA modified the NOL deduction for losses incurred after 2017 so there is no carry back and the carry forward is indefinite. But the deduction of post-2017 NOLs can only offset 80% of a taxpayer’s income in any year. The CARES Act reinstated carry backs of NOLs for losses arising in 2018, 2019 and 2020 and postponed the carryover only and 80% of taxable income provisions until 2021 l(See chapter 3.16 – NOLs for more detail.)

-

Coordination With Other Code Sections

Excess Business Losses:

-

Excess business losses do not include any deduction under IRC Sec 172 (NOL) or Sec 199A (qualified business deduction) or any deductions related to performing services as an employee.,

-

Because capital losses cannot offset ordinary income under the NOL rules, capital loss deductions are not considered in computing the Sec 461(l) limitation, and the amount of capital gain taken into account in calculating the Sec 461(l) limitation cannot exceed the lesser of capital gain net income from a trade or business or capital gain net income.

Form 461

If a non-corporate taxpayer has net losses from all of their trades or businesses more than the amount shown in the table above, Form 461 must be completed and included with their income tax return.