Employer Payroll Tax Deferrals (CARES Act Sec. 2302)

Employer payroll tax deferrals were part of the CARES Act, specifically Section 2302. Learn more about the language in the legislation below.

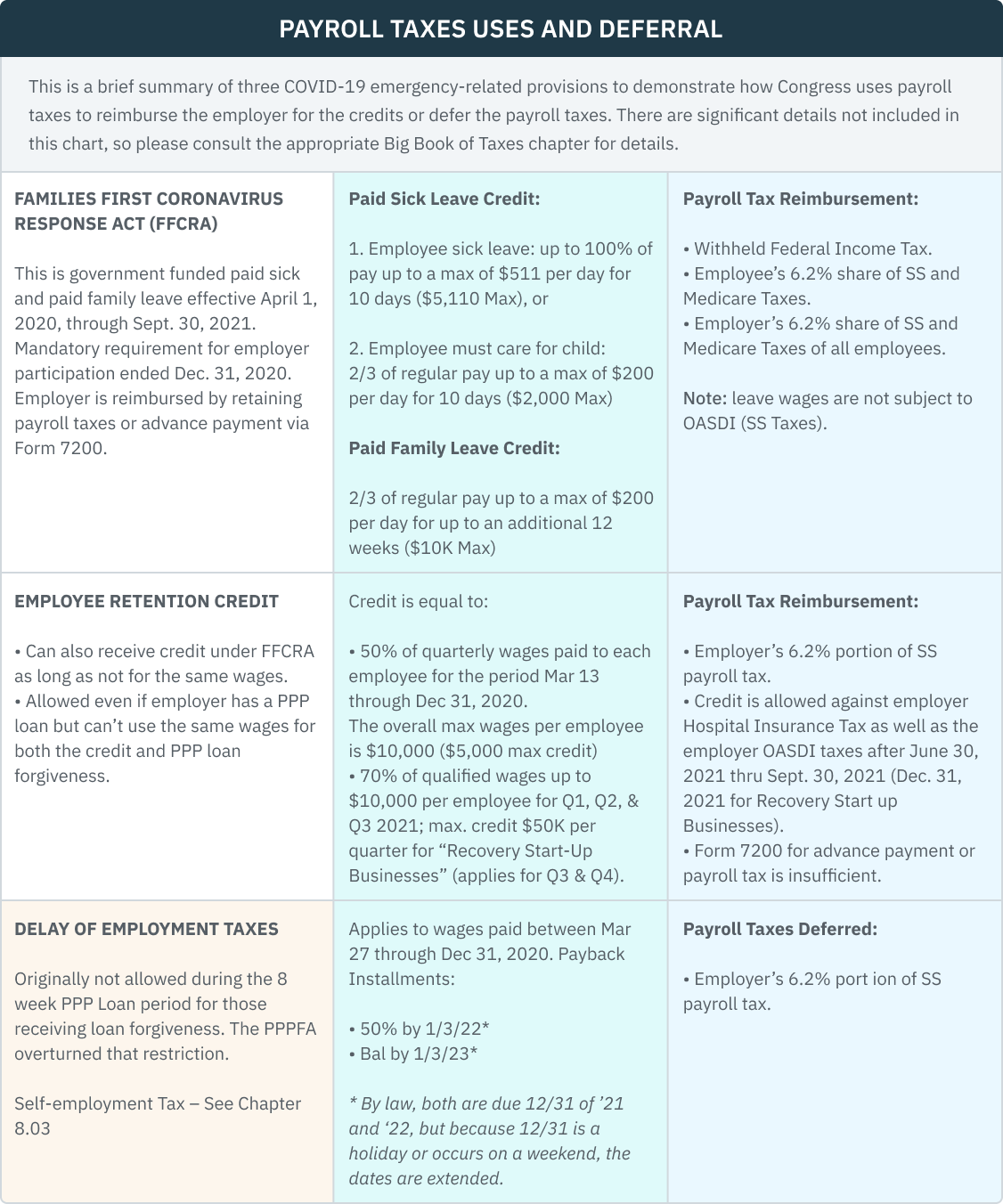

Taxpayers (including those who are self-employed) were able to defer paying the employer portion of certain 2020 payroll taxes. The delay provisions apply to all employers who chose to participate, regardless of size.

Taxes That Could have been Delayed

Taxes that could have been deferred include the 6.2% (IRC Sec 1401) employer portion of the Social Security (OASDI) payroll tax, and the employer and employee representative portion of Railroad Retirement taxes (that are attributable to the employer’s 6.2% Social Security (OASDI) rate) tax.

NOTE: The delay did not apply to the 1.45% (Sec 1401(a)) employer share of the Hospital Tax nor to the employee’s share of the OASDI and Hospital Tax.

Deferral Application Period

Applies to wages paid from March 27, 2020, through December 31, 2020.

Self-Employed

For self-employed individuals, the deferral applies to 50% of the Self-Employment Contributions Act tax liability (including any related estimated tax liability).

Employers who receive SBA loans that are forgiven under the CARES Act were originally not eligible for this payroll tax deferral during the eight-week covered period. However, under the Paycheck Protection Plan Flexibility Act (PPPFA) that restriction has been removed.

Payroll taxes have become the favorite tool of Congress to reimburse employers for paid sick and family leave under the Families First Coronavirus Response Act and for the Employee Retention Credit. The following table summarizes the various applications of payroll taxes.