Optional Business Mileage Rate Method

A complete guide to the IRS's optional business mileage rate method for deducting vehicle expenses.

As an alternative to deducting actual operating expenses of an automobile (and depreciation as described later in this chapter), taxpayers can use the “optional standard mileage rate” to compute business auto deductions for owned and leased vehicles.

Motorcycles

The IRS has never established an optional mileage rate for motorcycles; thus, the actual expenses method must be used. In Office of Chief Counsel Info letter (INFO 2009-0255) this subject was addressed and indicated that to date no standard mileage rate is available for motorcycles.

Leased Vehicles

The optional mileage method may be used for a leased as well as a purchased auto used for business provided the mileage method is used for the entire lease period. (Rev Proc. 97-58, 1997-52 IRB 24)

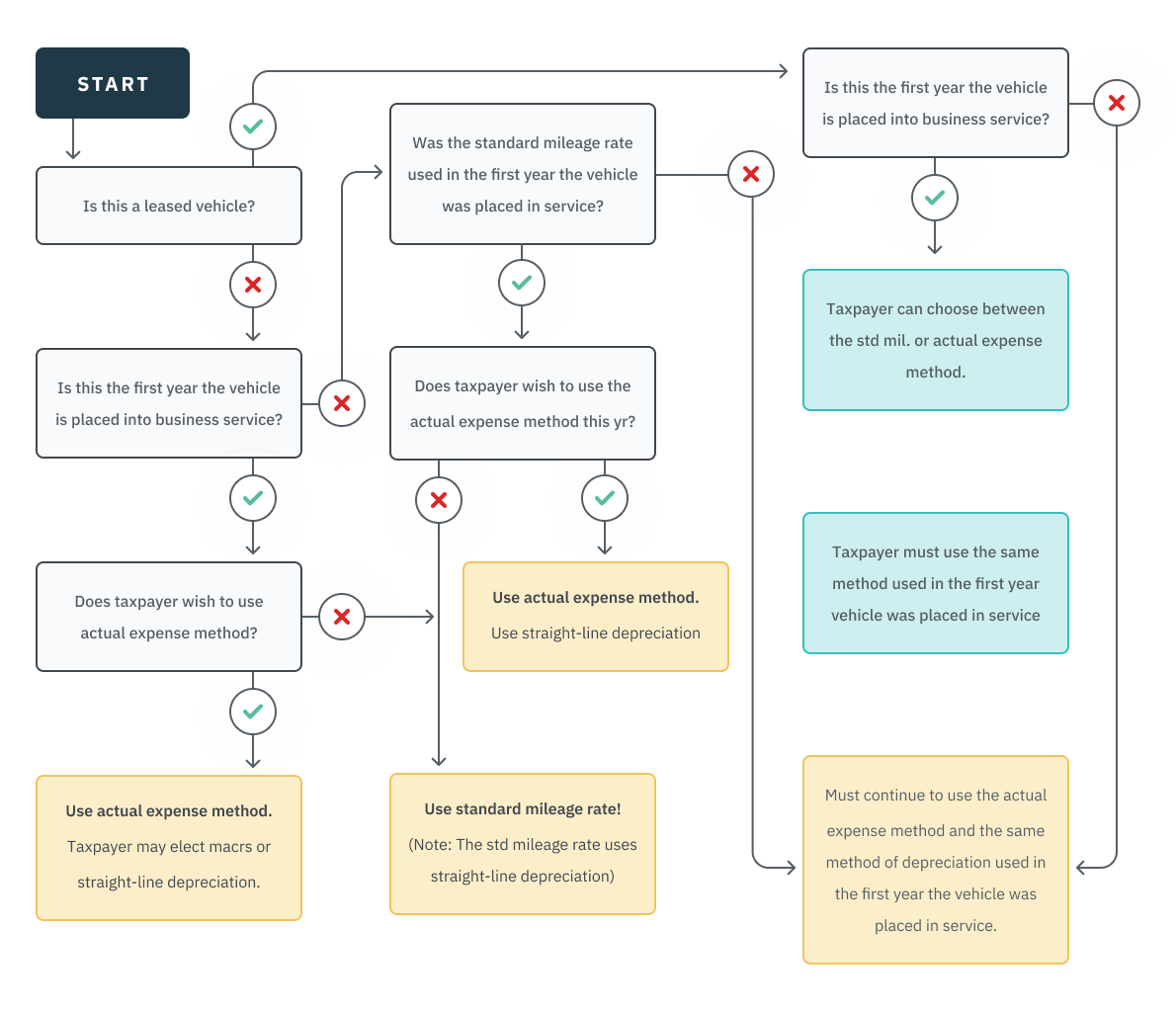

Method Chart for Vehicles

Chart assumes vehicle is not limited by the fleet operation rules

Multiple Vehicles

Whether the taxpayer is an owner or lessee, the mileage allowance method can’t be used to claim business auto deductions for vehicles used for hire or for fleet operations. Fleet operations are defined as 5 or more vehicles used simultaneously. Thus, taxpayers who use no more than four vehicles at the same time for business purposes may use the standard mileage rate.

Expenses Included in the Optional Standard Mileage Rate

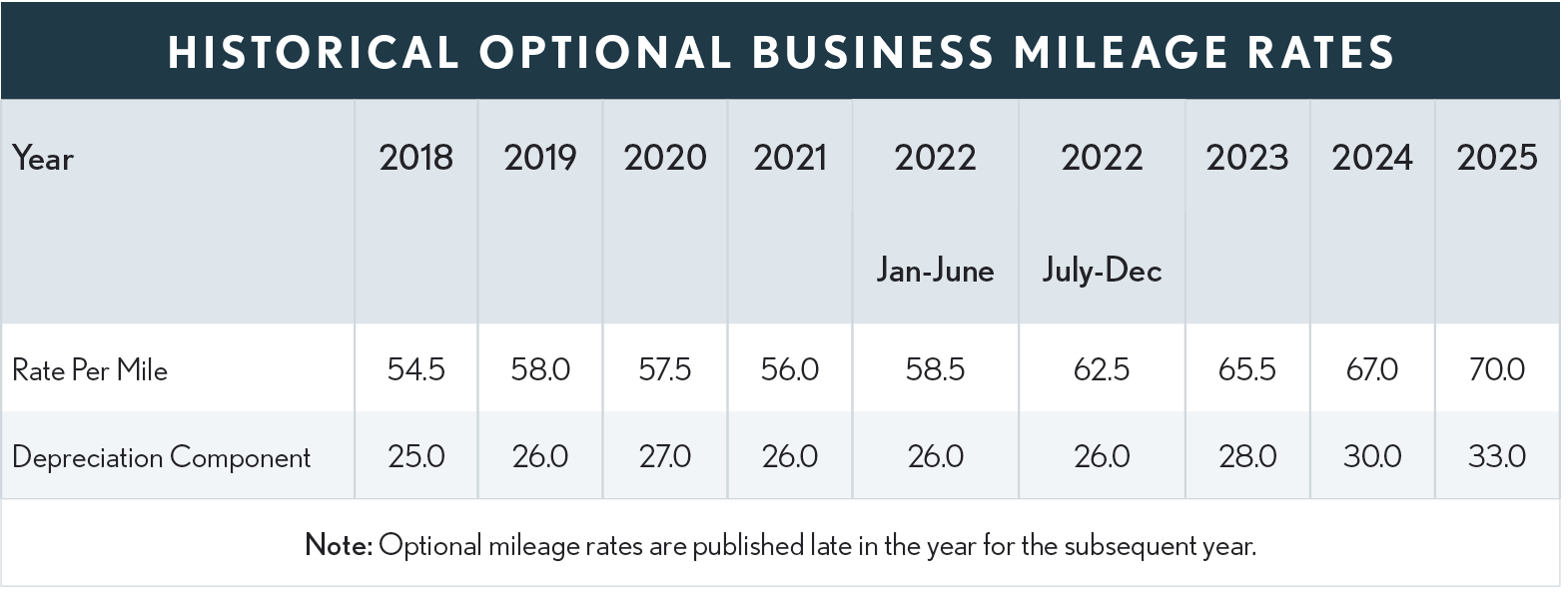

The standard mileage rate is determined annually by the IRS using data from a study conducted by an independent contractor of vehicle-operating expenses based on the prior year’s costs (Rev Proc 2002-61). The rate includes:

-

Gas

-

Oil

-

Lubrication

-

Maintenance and Repairs

-

Vehicle registration fees

-

Insurance, and

-

Straight-line depreciation.

Not included in the standard rate are:

-

Parking

-

Tolls

-

State and local property taxes attributable to business use.

These may be deducted in addition to the optional rate. This does not include sales tax, which must be capitalized into the business basis of the vehicle.

Vehicle Loan Interest

Regardless of whether the standard mileage rate or actual expense method is used, a self-employed taxpayer may also deduct the business-use portion of interest paid on a vehicle loan (claimed as an interest expense on Schedule C). For years 2018 – 2025 employee business expenses aren’t deductible for federal purposes because the Tier 2 miscellaneous deduction is suspended. Employees may not deduct interest paid on a car loan. (Note: in years before 2018 and after 2025, if a home equity loan is used to buy a vehicle, the employee may be able to trace and deduct the interest as home mortgage interest.)

Employers' Reimbursement

Employers may reimburse employees for business-related car expenses using the mileage allowance method for each substantiated employment-connected business mile. The reimbursement is tax-free if the employee substantiates to the employer the time, place, mileage, and purpose of employment-connected business travel.

Employees’ Expenses Exceed Employer’s Mileage Reimbursement

(Years before 2018 and after 2025) – Employees whose actual employment-related business mileage expenses exceed the employer’s reimbursement can deduct the difference as a miscellaneous itemized deduction subject to the 2%-of-AGI floor on their federal returns. However, an employee who leases an auto and is reimbursed using the mileage allowance method can’t claim a deduction based on actual expenses unless he does so consistently beginning with the first business use of the auto.

Rental Cards and the Standard Mileage Rate

Can an individual rent a vehicle for business purposes from a car rental agency such as Hertz or Budget and deduct the standard mileage rate as opposed to deducting the rental fee?

The standard mileage rate is allowed for leased vehicles (including cars, vans, pickups, and panel trucks), provided that the standard mileage rate method is used for the entire term of the lease (Rev. Proc. 2010-51, Sec. 3.01).

The standard mileage rate is not allowed for fleet operations. Fleet operations are defined as using 5 or more vehicles simultaneously. Thus, taxpayers using no more than 4 vehicles at the same time are allowed to use the standard mileage rate (Rev. Proc. 2010-51, Sec. 4.05(1)).

The standard mileage rate includes an allowance for depreciation (26 cents per mile in 2022). As the owner of the vehicles it is renting, the car rental agency will be depreciating the costs of those vehicles.

Although there is no restriction on using the standard mileage rate on leased vehicles, and although a car rented from the likes of Hertz and other car rental agencies is a short-term lease, the fact that the rental agency is depreciating the vehicle prevents a taxpayer who is renting the vehicle from claiming the standard mileage rate, which includes imputed depreciation. Multiple individuals or entities cannot depreciate the asset at the same time.